who is the innovator? or market size for the same?

Posts tagged Value Pickr

Kovai Medical Center and Hospital – Health and Wealth (16-11-2023)

Its finally great to see long term debt coming down. On top of that I was really surprised by the 12 % revenue growth in the Health care segment. I was expecting to see contribution from the 5th year of admissions in this quarter. Hope to see that next quarter. With the final year in, hope to see leverage kicking in and better margins

Ranvir’s Portfolio (16-11-2023)

Akzo Nobel Q2 concall highlights –

Sales – 956 vs 926 cr

Gross Margins @ 44.7 vs 38.4 pc

EBITDA – 142 vs 106 cr ( margins @ 14.8 vs 11.5 pc )

PAT – 94 vs 65 cr

Double digit growth in automotive coatings business led by OEM demand. Marine coatings also grew strongly on the back of strong orders from Defence. Protective coatings also grew well driven by oil and gas and power segments

Paints business impacted by subdued demand, erratic rains. Tier -2,3 towns showing good sales pick up. Premium end of the Mkt doing better than mass mkt

Company’s paints business is now on negative working Capital !!!

Cash on Books – aprox 670 cr

Company’s good performance in smaller towns, rural areas led by distribution led gains and lower base vs larger competitors

Q3 likely to see festive tailwinds

Revenue contribution from new products launched in last 2-3 yrs currently at 10 odd pc

Company intends to jack up advertising and sales promotion expenses from 3.5 pc of revenues currently to 5 pc of revenues. Company – advertising heavily during Cricket World Cup

B2B – business has been surprising positively. B2C – remains challenging

Company’s current Mkt share in paints business is around 4.5 pc. Intend to take it beyond 6 pc in about 2 yrs by focussing more on the mass mkt where the company is still on a weaker footing

Velvet touch – premium brand continues to do well

Disc: hold a tracking position. Not SEBI registered. Biased

Himatsingka Seide (16-11-2023)

I found the management quite bullish on this concall, which is different from the usual very conservative style. They maintained their stance of ‘stable demand outlook with an upward bias’ whilst answering all questions.

- In further questioning, they sounded more bullish when guiding that capacity utilisation should reach in high 90’s before 3 years from high 60s currently. When I asked them about triggers for this on the call (below), their reasons were pretty well outlined, though obviously it still has to play out.

-

On debt, they are happy to work on it to reduce it year by year, rather than doing something like raising capital at these valuations.

-

IMO, valuations are very attractive versus peers still for the kind of business/management this is purely because of above debt. Versus the likes of Welspun/ICIL, I think Himatseide can do some good catching up on P/B P/S in case they are able to pare down this debt (even if in a longer timeframe/maybe dilution at better than current valuations over time in a favourable business environment)

-

There is significant capacity headroom here without needing Capex in case a bull cycle is coming with all the triggers in the sector (coming out of destocking, issues with Chinese cotton ban, Pakistan industry issues, potential FTAs, new products/divisions, domestic product launch). Currently capacity utilisation for them is in the high 60s.

Essentially, I invested as I thought in the next few years the R/R was favourable and there is a chance of the dual engines of earnings growth + multiples expanding in case the situation plays out for the company.

Disclosure : Invested as core PF position in self and family accounts and hence I am biased. I am not a registered SEBI advisor and this is not investment advice. I have made transactions in the last 30 days at lower levels.

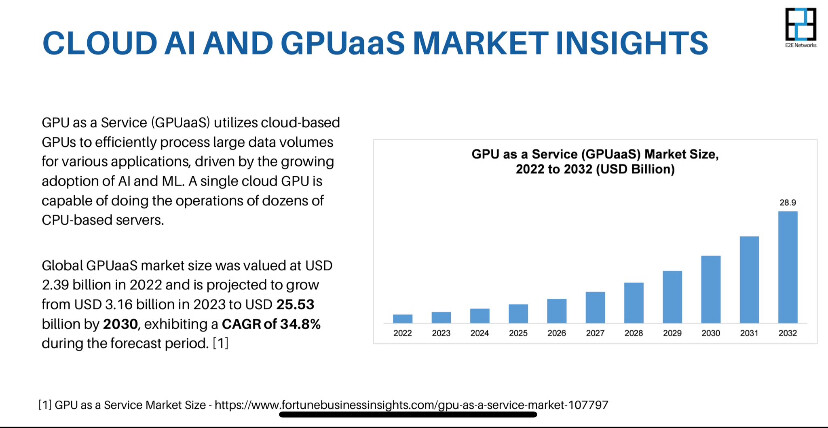

E2E Networks Ltd – Listed small Cloud computing player (16-11-2023)

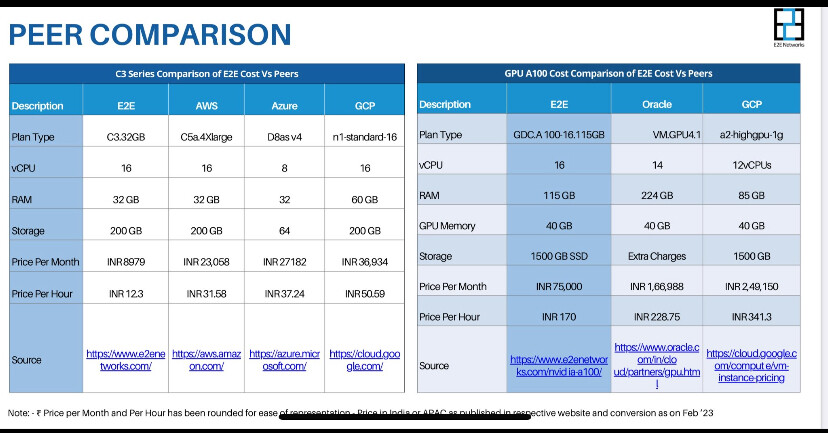

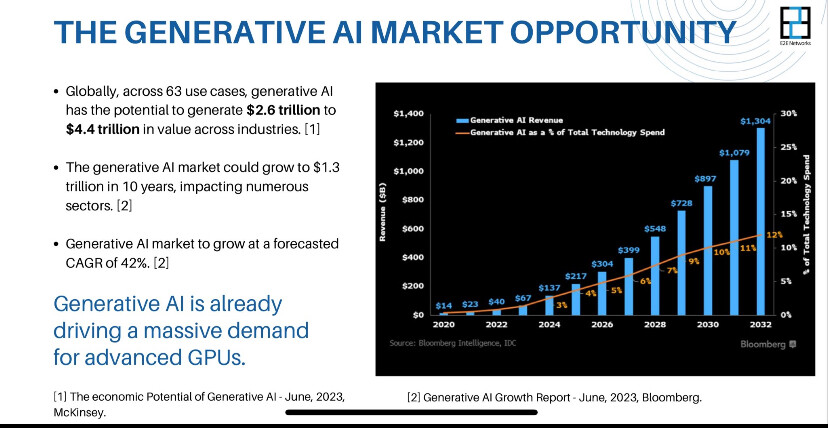

This is the only Indian listed company in GPU cloud segment. Screenshots from company website is here oliw :

Please see the companies website where one can see the competitive edge what this company offer

JK Paper – Best Bet in Paper Sector? (16-11-2023)

Long term debt reduced by around 200 odd crores in the HY. Interest outgo has reduced proportionally. Crisil ratings is a good read about the capex and assets.

The company is expected to undertake yearly maintenance capex of Rs. 100-150 crore and a partially debt funded capex of Rs. ~650 crore during FY 24-26 to set up a BCTMP pulp mill, which will help in backward integration and will substitute imported pulp at Unit CPM. Despite the said capex and acquisition of Manipal Utility Packaging Solutions Pvt Ltd for a consideration of Rs. ~90 crore, expected to be funded out of cash accrual.

The company’s liquidity position remains strong, characterized by healthy unencumbered cash and bank balances of Rs. 1225 Cr (Rs. 900 Cr in Mutual Fund and Rs. 325 Cr in Bonds) as on September 2023 and average unutilized fund based limits of around Rs 163 crores (~65% of total limits of Rs 250 crores).

source: crisil ratings

Swiss Military Consumer Goods (16-11-2023)

I had invested earlier in it, but exited due to trademark litigations issue. Company should perform good but there will always be a regulatory issue with the trademark.

Rajshree Polypack – The food packaging specialist (16-11-2023)

Q2FY24:

• Volume growth 17% yoy.

• Injection Moulding: In process of machine upgradation to enhance installed capacity.

• Developed 6 new products

15 new customers onboarded including 4 overseas customers.

Strong Customer retention with ~97% of revenue from repeat customers.

• Appointed Chief Marketing Officer.

• Company’s export revenue tripled on Y-o-Y basis to ₹15.32 Crores for H1FY24.

• Around 55-60% of the business is coming from dairy and beverages.

• Injection molding capacity expansion: It is in discussion phase as such. As and when it materializes, will let you know the exact numbers.

• Patents: One is a process patent which we have done for making the tube laminates, that’s a process patent which we are holding. The other is product packaging design patent which we are holding.

• Tube laminates: We are constantly evaluating this particular market so as and when we feel that the situation is correct to have a dedicated line for this particular segment, we will take a call for investing for a dedicated line for the tube lamination. At the moment, it is on halt.

• Over the period of 2-3 years, we expect it to at least go to 12 crores to 15 crores per quarter or at least Rs. 50crores- Rs. 60crores coming from export.

• In-Mold Label: In-Mold Label, we have commercially established the product and we have started manufacturing. We have received the initial trial orders from the customers and we will ramp up the production of IML products in coming quarters. So, that is the six products of what we have added in which that one of the products is Injection Molded product, Label products.

• Olive Ecopack: Rs. 100 crores- Rs. 110 crores revenue we can definitely look for next year. that number will be a break-even number.

• So, for next quarter, definitely, we’ll see the reduction in the Finance Cost.

• Customer advance for capex: It will be difficult to reveal the name of the customer but, yes, as I mentioned that few of the customers where we have almost monopolistic supply and as the customer is expanding their business, they wanted us also to increase the capacities and it helped us in increasing the capacities as we were doing a lot of investment and we needed that support and they accepted our request. That’s the only thing, I would say.

• In food packaging, since sustainable packaging still are not able to meet the functional requirement, we don’t see much entry of sustainable products entering into Food Packaging but there the more focus will be on to recyclability and using recycled materials. And in Food Service, the focus will be more on using sustainable products. And we would say, as a company we are well placed in both the sectors and so that will help us to achieve the growth in the next five years

• Capacity increase: we are working on increasing the capacities on the existing machines by doing some modifications and we have got very good results and probably in the next one month or so we should be able to announce that the increment in the installed capacity on these processes around 10%-15%.

The Anti-Portfolio (16-11-2023)

Hi Sandy, thanks! I don’t have much of an opinion, there are 2-3 business areas they operate in, remember having invested before (for hardly one quarter). Results are on very good uptrend so you can maybe keep holding. I didn’t find conviction to make big enough holding, since it was also highly valued then.

Disclaimer : Am not an sebi analyst/advisor, this is not a stock recommendation