Did anyone attend the call. Any takeaways?

Posts tagged Value Pickr

Wockhardt – A story with twist and turn (13-11-2023)

Results are tomorrow and price has gone up considerably today….One always has to be cautious with Wockhardt because it is a serial disappointer but do people think that this new antibiotic that is going through testing could be a game changer ?

Amrita’s portfolio (13-11-2023)

Current portfolio:Nov 2023

Suggestion wanted.

Age of portfolio 3.5 years

1.Caplin Point :Good fundamentals at decent valuation.Holding since 2020

Av Price: Current Price

Will add more in future

2.Titan Biotech: Good fundamentals at decent valuation.Unfortunately the stock is not moving much.Will hold on and see what happens.Hokding since 2020

3.Ngl fine Chem: Running at a loss.Poor results and overvalued.Recent quarter has given better results.Will hold on for some recovery

4.Ganesh benzoplast: Decent stock.Holding now to see how the stocks moves.May add in the future if good fundamentals persist

5.Chemcon:Running at a loss.Poor results and overvalued.Recent quarter has given better results.Will hold on for some recovery

6.Saksoft: Multibagger stock.Currently overvalued.So not making any fresh addition May add at lower levels during market correction

7.Infobeans Tech: Average returns.Holding to see if results improves in the next few quarters

8.Polycab : Great fundamentals and overvalued.So no fresh addition except at lower levels during market correction.Holding since last 3 years

9.Kei Industries :Same as above.Holding since last 3 years

10.Lincoln Pharma:I love this stock.Decent fundamentals and good valuation.Holding since last 3 years

11.Deepak nitrite:Holding since last 3 years.

12.Jk paper:Holding since last 3 years

13.Sonata software: Good fundamentals at decent valuation.Holding since last 3 years

Recent buys

1.Expleo solutions

2.Mk exim

3.E cleryx

52 week highs and all time highs strategy (13-11-2023)

HCC cmp 30 . Fundamentally the company claims to be on a deleveraging path. If is one of the turnaround candidates. If it is successful, the pattern shown below can play out, but one has to closely monitor this kind of company on a regular basis to check how the story is playing out in terms of turnaround, or failure thereof.

According to their latest presentation, • Investor acquired 51% shares in Prolific Resolution Private Limited (PRPL). With this, PRPL has ceased to be a subsidiary of HCC, with effect from 30 Sept 2023.

Consequently, ₹3,301.2 crore of debt has reduced on a consolidated basis.

Above is one of their latest exercises to reduce debt at consolidated level.

Company mainly operates in hydro, water, nuclear and transportation segments of infrastructure and power. Order backlog 12300 crores. Quarterly revenues as of last two quarters at 1800-1900 crores. Company does presentations, concalls etc which one can utilise for detailed research.

Technically, the stock price broke out of a 5 year high above 21 and the whole consolidation below it was an early rounding bottom formation. Since 12 weeks it was consolidating within a weekly triangular formation ( on weekly line charts) and now has broken out of this consolidation. The latest upmove also resembles a flag pattern with flagpole extending from 19 to 29, and breakout happening at 28.5.

disc: invested with a small allocation as a techno funda bet. ( not a recommendation, anyone considering investing should do their own diligence. )

MOLD TEK PACKAGING—dividend plus growth (13-11-2023)

Hi all,

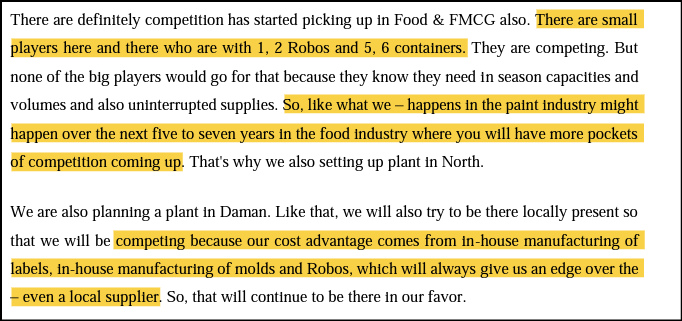

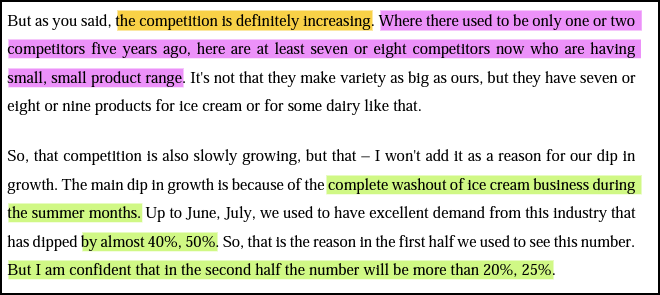

Look to these Snippets from the company con call, The Company is taking the competition seriously and clearly sharing why they have subdued growth and all. At the end of the end transparency of management and taking every small competition seriously help in the long term to protect market share and all.

Deepak Fertilizers and Petrochemicals (13-11-2023)

Hi,

Can you plot Q1 and Q2 number on excel and share the calculation?

Investing Basics – Feel free to ask the most basic questions (13-11-2023)

Thanks for your valuable response.

Narayana Hrudayalaya Ltd (13-11-2023)

Great numbers. Last 5 years growth from 51 Cr. PAT to 680 Cr. PAT on a TTM basis.

Seems like the highest-ever EBITDA, PAT, and Revenue in any quarter in NH.

Shivalik Bimetal Controls Ltd (SBCL) (13-11-2023)

Thanks for the reply. I guess there is some confusion and that’s primarily because of its name ![]() . Let me clarify further. I am not taking competitive advantage period as an assumption in the above modelling works. This is a calculated field. First of all, there are many names of this period. MM calls it as competitive advantage period but more often refers it as market implied forecast period. His basic premise is that expectations investing starts with what we know, the stock price, and asks whether the expectations for the company’s financial performance implied by the stock price are justified.

. Let me clarify further. I am not taking competitive advantage period as an assumption in the above modelling works. This is a calculated field. First of all, there are many names of this period. MM calls it as competitive advantage period but more often refers it as market implied forecast period. His basic premise is that expectations investing starts with what we know, the stock price, and asks whether the expectations for the company’s financial performance implied by the stock price are justified.

Before we discuss it further, let me put here his response to an interview question by Motely Fool:

Q: The book also says, “Analysts typically choose a forecast period that is too short when they perform a discounted cash flow valuation.” Most forecast periods I’ve seen are five to 10 years before they calculate the terminal value. Can you explain how analysts should determine how long the forecast period should be?

A: This is interesting. Most DCF models use an explicit forecast horizon of five years. Some go out 10 years or more, but they tend to be rare. I think the five-year horizon is an outgrowth of the leveraged buyout models used in private equity. Five years may make sense for a private equity firm that has an explicit objective of exiting an investment in about five years. But just because we have five fingers on a hand, or because private equity firms hold investments for five years on average, does not have any relevance for properly modeling the economics of a public company.

The result is that investors have to allocate value in the continuing value estimate, often through using an unrealistic calculation of growth in perpetuity or multiples of earnings before taxes, depreciation, and amortization. The goal of a model is to represent reality, and this approach fails in that objective.

You determine the market-implied forecast period by using consensus estimates for free cash flow growth plus an appropriate continuing value, an estimate of the cost of capital, and seeing how many years are necessary to solve for today’s stock price. For example, in the case study we did on Domino’s Pizza we found that the market-implied forecast period was eight years.

Now if you read above answer by MM, it becomes clearer. In nutshell, this is not the period in which they will lose or maintain its competitive advantage, rather this is the number of years which the current stock price assumes that the company will have ROIC higher than WACC i.e. will have a period with competitive advantage. This is the period which an investor should project in future to do DCF calculations and beyond that period, terminal value calculations. Hope it’s clear.

Now, coming to your statement that if this period is 25 years or more, every company will be undervalued. Here is the proof why this isn’t the case.

Let’s take the example of Asian Paints. No one can argue that this company shouldn’t have competitive advantage for many years to come. However, the current stock price already has assumed this or rather it’s already factored in the price.

Below are the details of Asian Paints:

- Steady state value = 36, 275 Crs

- ROIC in 2023 = 31%

- Future state value = 380, 619 Crs

- Total value = 416, 894 Crs

- Competitive advantage period or market implied forecast period = 25+ years

- Value per share with margin of safety = 2173 which is lower than current price. That means its overvalued.

For more details, I would highly suggest you read his book, watch his YT videos and / or read his interviews. It will be super clear.

Mann’s Portfolio (13-11-2023)

What is top line growth guidance in next 2-3 years for creative newtech ltd by promoter.