Is the group created or still in process

Posts tagged Value Pickr

Saregama India Ltd: India’s premier music publishing label (13-11-2023)

Hi @Worldlywiseinvestors Ishmohit, has your thesis changed on Saregama after the acquisition of Pocket Aces and demerger? Do you see better capital allocation from the firm going forward since they have demerged the loss making segment? And also, what’s your take on TIPS growing much better than Saregama in terms of revenue?

I would like to thank you for the content which you post on social media, it is a great time always to learn something new instead of receiving calls and tips! ![]()

The Anti-Portfolio (13-11-2023)

Yes valuation is expensive and time is stretched hence some change in views. Still planning on holding but have been reducing allocation by selective selling for occasional liquidity needs.

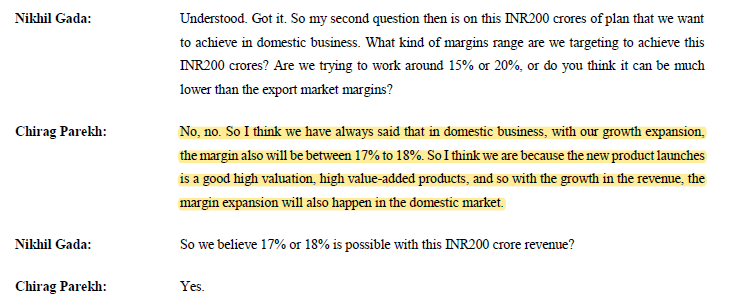

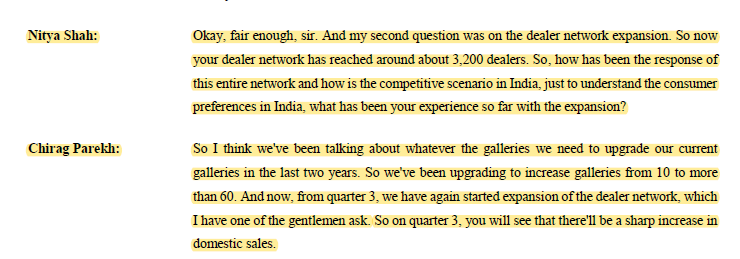

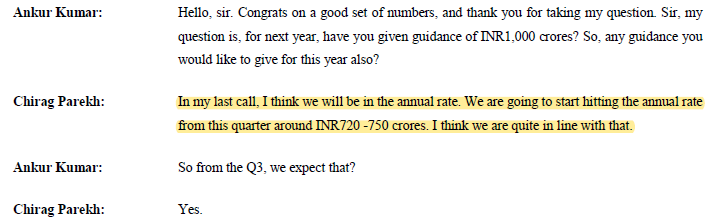

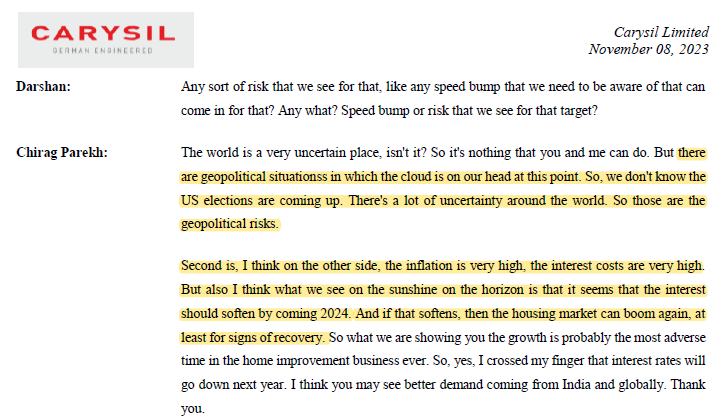

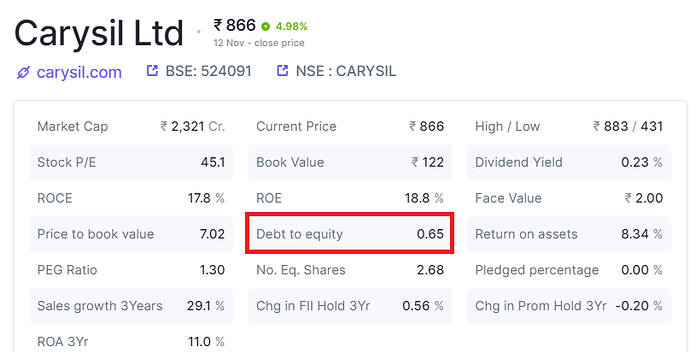

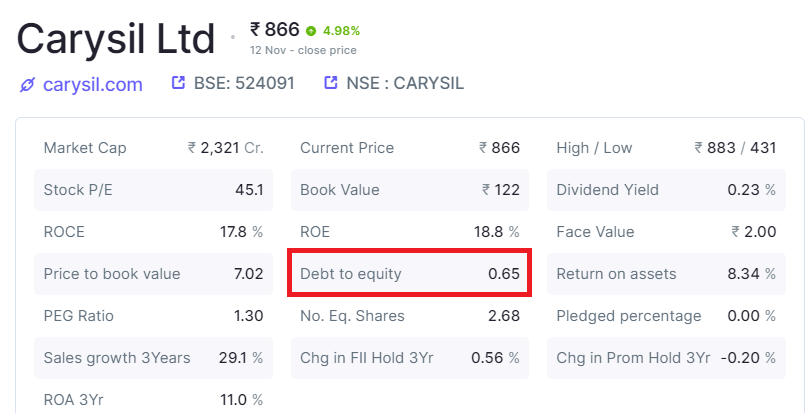

Carysil (earlier Acrysil) – Kitchen sinks (13-11-2023)

The management has provided a very bullish view on the growth targets.

The overall tone of the concall was extremely positive

Guidance:-

Target of 1000 Crore revenue by FY25

EBIDTA margins of 20%

Positives

-

Increasing SOM in International/Domestic geographies

-

Destocking issues over with rising volumes

-

Strong Order Book for Q3 and Q4

-

Upbeat on Domestic Market w/ strong Dealer N/w

-

Strong FY23 guidance w/ performance in H2

Negatives

-

Geopolitical and Macro issues continue to be a risk

-

Rising Debt due to multiple acquisitions

Summary

- The management is extremely bullish on the growth propspects

- One of the few cos. to acknowledge destocking issues are over

- Better cost management gives it and edge over the competitors in EU

- Valuations a tad expensive but can be justified with expected growth in next 2 years with increasing SoM and Operating Leverage

- Rising debt is something to keep a watch on. US acquisition will reflect in B/S only from Q3.

Disc: Invested and holding

Mann’s Portfolio (13-11-2023)

Hello,

In My limited Understanding

Needle Rollers are typically very customized as per the different application, which causes SKP to spend very high amount of time just to onboard the different clients.

Ball Bearings though can be customized the customization is very limited (hardly 4-5 Types as per management)

Ball bearings is very Volume related game

And Just so you know that the margins at 45% utilization is near to 20%, Better cost utilization imo can take the same to 25%, as better absorption of fixed cost will happen

and also the Needle rollers are used at large in ICE Vehicles’ engine, where as Ball rollers are used at large in EV since the main characteristic of Ball rollers is that it Suppresses the Noise caused due to working of the machinery which is the main reason why Balls are used in it since EV are silent

Of-course the Blended margin will come down the same is acknowledged by management too in recent Call

And For capacity Utilization the ball Volume for H1 is up 80% odd the same isn’t Updated here, the revenue is flattish in light of ongoing downside in Textile sector and hence the new capex is stopped, halting the revenue from Other Sectors

The Anti-Portfolio (13-11-2023)

Hi Vikas, any changes in your views on Gujarat Themis Biosyn & Shivalik Bimetal after their not so good quarterly results…

AA – Abhishek’s Attic (place to store stuff to clear my head)! (13-11-2023)

Is this net inflows? I assume so, but wanted to confirm.

Genus Power – Smart Metering (13-11-2023)

Q2’FY24 conference call notes summary –

Orderbook Position

- Current order book ~19,500 Cr; Out of that ~70% is available to Genus. Execution period – 27 months; The order book can be further broken into – Production, Installation and Maintenance (6-7 yrs.)

Revenue Guidance

- 1,200 Cr. confident guidance for FY24, Aasam and Bihar orders to contribute for FY24 revenue;

- For H1, it has been Rs. 520 Cr. Remaining revenue 680 Cr. is expected in H2’24. That will be more than 50% growth in revenue against H2’23.

- Revenue for FY25 & FY26 will be multi-fold

Margins

- Current subdued margins are due to increased expenses for preparation of delivering the huge order book e.g. employee cost, finance cost etc.

- Once the revenue from newer order comes in the management expect to 15-16% margins

Future Outlook

- Ability to take orderbook to about 30,000 Cr. That was a target for 3 yrs. orderbook. 2/3rd of that already achieved.

- Current capacity 10 Million orders. Can increase capacity if the orderbook continue to scale up

I have initiated a position during last week considering the tailwinds for the smart meter adoption. The thing that I am particularly cautious about is – these orders largely being from state electricity utilities, shall we be aware of some challenges about the receivables. Has company management ever clarified about their strategy about saving themselves from receivable related challenges from state electricity boards.

Dreamfolks services limited( DFS) (13-11-2023)

I am quite surprised that Dreamfolks has not yet suggested a Rs 50 convenience fee in the structure. Since the differential of Rs 2 and Rs 300-500 for food is huge, people will still pay. Banks can still call it free. This will address the margin which Dreamfolks has lost.

Disclosure – Invested and optimistic of growth since the potential due to new lounges, new airport, stations is huge.

Will this Bull Market last forever? (13-11-2023)

this is my source for FII investment: https://www.fpi.nsdl.co.in/web/Reports/Yearwise.aspx?RptType=6