RBI releases cards related data every month.

https://m.rbi.org.in//Scripts/ATMView.aspx

Posts tagged Value Pickr

IDFC First Bank Limited (11-11-2023)

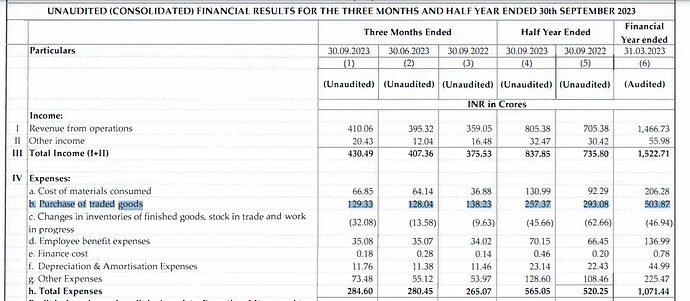

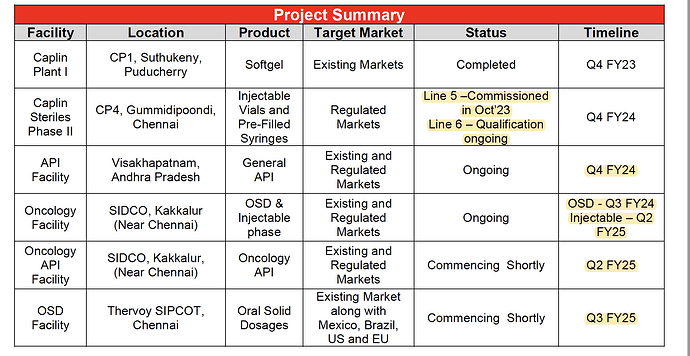

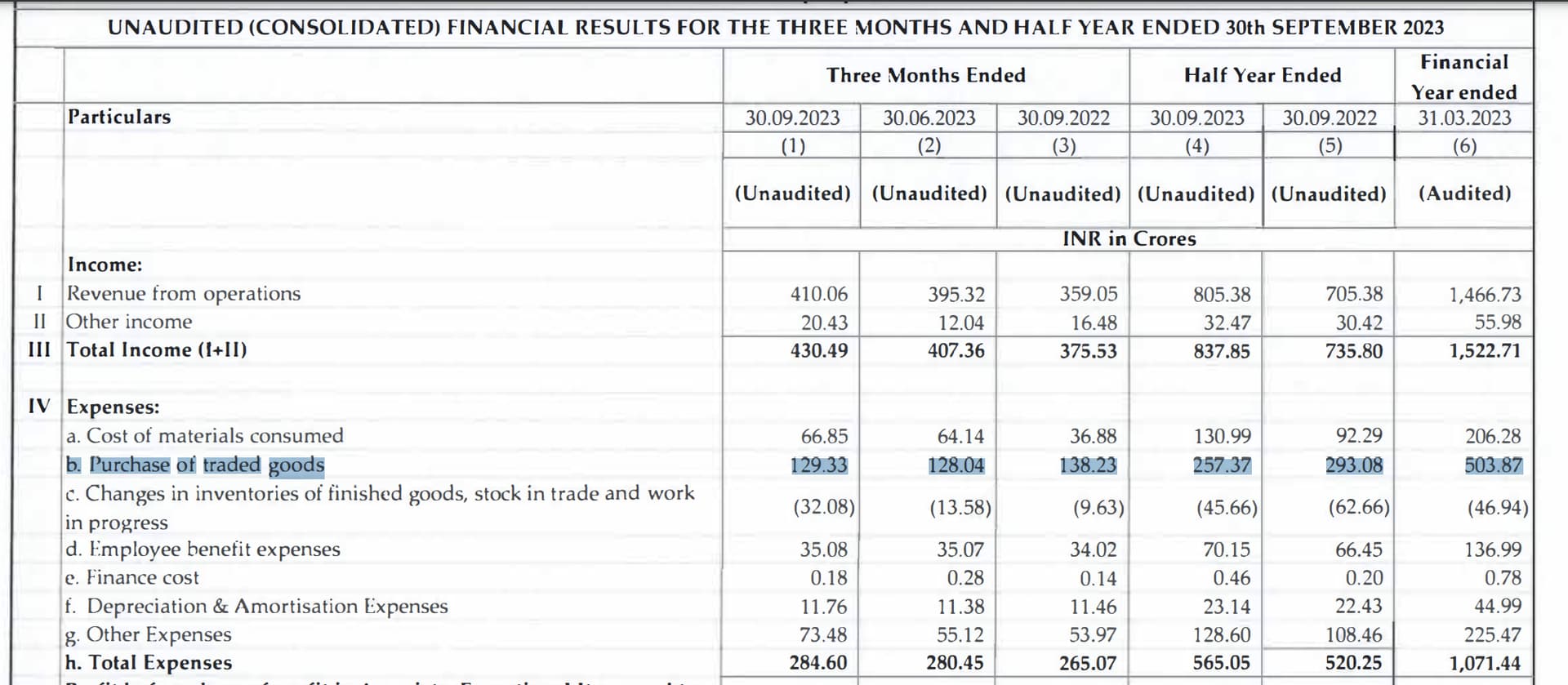

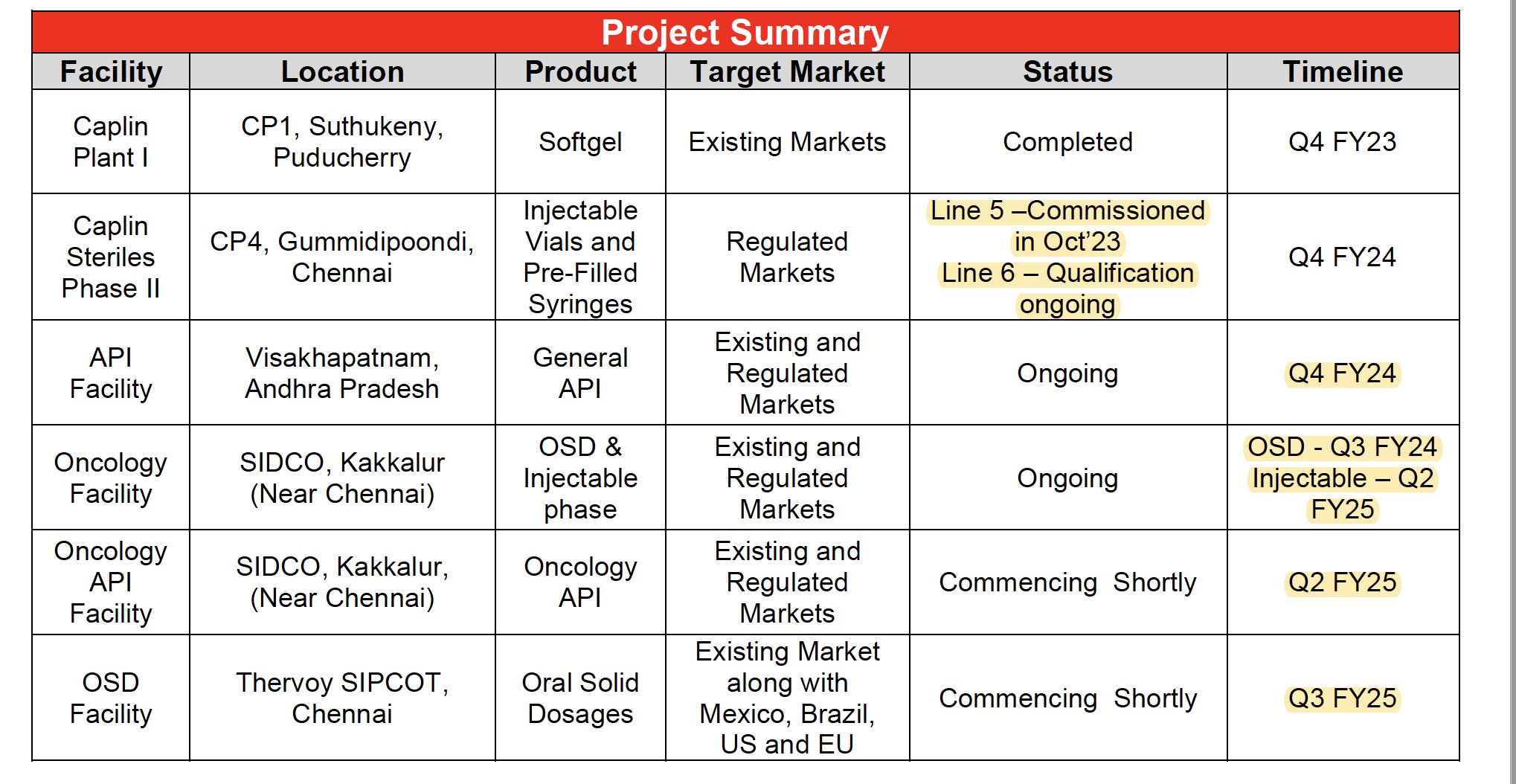

Caplin Point Laboratories (11-11-2023)

Another good quarter from the co, sales grew by 14% and EPS by 25%. They are in heavy investment mode, which will continue for the next few quarters. Concall notes below.

FY24Q2

- Large reduction in purchase of traded goods leading to better gross margins. However, guides for lower gross margins going forward

- Profit share for Caplin Steriles: 30% with 70% coming from product supplies. Made 12.5 cr. EBITDA in H1 as they are expensing out all R&D and filing expenses. Core business has same margins as standalone (if R&D/filing expenses are removed)

- LATAM revenue breakup: Wholesalers 55%, Direct to Retail 25%, Institutional 20%

- Mexico expansion: want to replicate LATAM model where they sell via smaller distributors. Meaningful scaleup will require atleast 2 years and 100 products

- Tied up with third party manufacturers (2 Indian + 1 Chinese) for supplying penicillin and cephalosporin range of products in Mexico

- Plan to launch 15 own-label products in US in next 1 year

- Niche products in USA: filed 3 Ready-To-Use Bag products, filing Suspension Injectables, Emulsion Injectables, Emulsion Ophthalmic and Plastic Vial injections

- Injectable facility will cater to non-US market as well, filing completed for multiple products

- Planned capex: 600-650 cr. (more than half has already been spent)

- High speed vial filling line commercialized (will be replacing other line as the new Bosch line is 2-2.5x faster)

Disclosure: Invested (position size here, no transactions in last-30 days)

Optiemus Infracom – How much business Blackberry is going to bring for it? (11-11-2023)

I had done initial due diligence on this company and checked their AR…since they have a holding company structure, very little worthwhile information is available in AR to evaluate the EMS side of business and make a view on the future of the company. Management keeps giving interviews and paints rosy future, thought nothing much has materalized as yet…latest deal on manufacturing mobile phone screens (in partnership with corning) also will take time to show impact.

Considering all these factors, i exited the company in a matter of weeks.

Kanchi Karpooram Ltd (11-11-2023)

The management writes off the “Excess remuneration” to the directors, while the company is posting huge losses.

Simple strategy with back-test results (11-11-2023)

Hello!

Thanks for sharing Acquirer’s Multiple results. I tried to replicated these with the following:

Market Capitalization in Cr > 1000 AND

AcquirersMultiple < 5 AND

AcquirersMultiple > 0 AND

Long Term Debt To Equity Annual < 30 AND

Promoter holding latest % > 40 AND

ROCE Annual 5Yr Avg % > 20

And the best I’m able to do seems to be about 30%? I’m definitely doing something wrong. Here is what I’ve tried to fix:

Acquirer’s Multiple Definition: EnterpriseValue Annual Cr / Operating Profit Annual in Cr

Duration: I’ve matched the Sep 15 Date from the screenshot you had shared!

I bought Trendlyne specifically after seeing your post, and would really appreciate any assistance in spotting the error ![]()

Campus Activewear – betting on the India Consumption Theme (11-11-2023)

Hi! I’m a beginner as well.

Just wanted to understand your thought process, if you have conviction in the company, why not downward average after it gets correction instead of selling at a loss (if it’s still under the max % allocation of the portfolio). Previously you mentioned, that the next quarters will be likely better and then the stock is likely to bounce at that point.

Another question, how long had you been holding the stock for.

Disc: Not invested

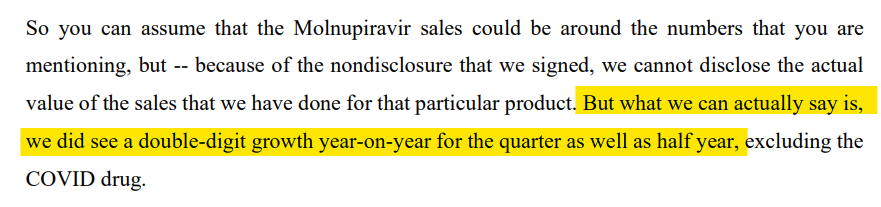

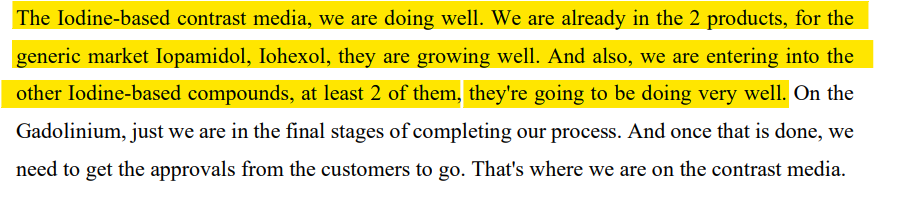

Divi’s Laboratories (11-11-2023)

-

They see a double-digit growth YOY

-

Entering into the Iodine based compound

-

See excellent opportunity in peptides

Pricol limited – OEM automotive (11-11-2023)

Will it be taken by minda? In that case that willl happen to the minority shareholders

Caplin Point Laboratories (11-11-2023)

Capex budget: 600 cr

To be completed by Q4 FY 25. That is March 25.

By Jan 2026 everything is operationalized.

Total net block = 300 (before) + 600 = 900 Cr

Latest net fixed asset turns = 5.25

Total revenue generated by Jan 2026= 900*5.25= 4725 cr ( current 1500 cr).( 3.15x~3x)

Net margin latest = 25%

Net profit Jan 2026= 1181 Cr. (Current= 400 Cr)( 2.9x~3x)

CAGR for 4 (conservative estimate) yrs after tripled profits= 114/4 = 28.5 % CAGR approx

Is this a fair way to estimate future revenue & earnings potential? If it does work out then, would it be fair to also estimate that the share price will at least triple if things go as planned and PE remains stable or improves?

Time technoplast (11-11-2023)

My impressions from Q2 FY24 results & ppt:

Company had given a deadline of end-Sep 2023 to complete the whole overseas sale for the last 8-9 months atleast, and clarified that 2/3 (US, SE Asia, SW Asia/Middle East) were in advanced discussions in last conference call. Looks like they need more time to close this. US business is going through headwinds, so one can speculate if selling US business is problematic.

-

CNG Cascades – 225 crores order book for next 6-8 months – ~170+ crores revenue possible in next 2 quarters for FY24. No other competition, but noises from BHEL-Indraprasta Gas MoU to develop CNG Cascades esp for hydrogen applications. Indraprasta Gas is a Time Techno customer.

-

LPG – going on BAU mode with IOC repeat order (~7.6L) utilizing most realizable capacity of 1M. They made ~231 cr in FY22, ~190 cr in FY23 and may be clock ~200+ cr in FY24. Looks like IOC order is high volume but less profitable as company hasn’t increased LPG capacity in last few years. Supreme Industries has got similar order from IOC, but not sure if Supreme competes with Time Techno by supplying to other PSU/private LPG companies

-

IBC – Expanding big time – company has IBC capacity directly and through subsidiaries both in India and all over the world (Type-4 LPG and CNG Cascade capacities are only in India as far as I know). Pyramid Technoplast which recently IPOd is a direct competitor here, and also expanding capacity judiciously.

-

FY24 remaining order book of 200 cr for pipes – these are good top line numbers, but this is less profitable and probably more working capital intensive too… cash flow might also take longer if this is related to govt contracts.

Overall a lot better than expected Q2 results, hopefully will lead to 650-675 crores FY24 EBITDA.

Management is clearly executing well on value-added products revenue/profitability… fingers crossed on their 17% EBITDA goal within 3 years… the goal was for 17% including overseas business, but will be easier to achieve with just India business.

Discl: Invested since 2018, added more till 2022, big part of portfolio.