Any update on Q2 FY24 result and business outlook

Posts tagged Value Pickr

Phantom Digital Effects Limited (10-11-2023)

What is short term borrowing? From some bank? NBFC? If so, why are they reporting it under operating activities instead of financing activities?

When you put this together with their recent efforts to raise further money; I suspect they are facing a reasonable cash flow issue.

Basilic Fly Studio Ltd (10-11-2023)

Thanks for this new page. Have you done any comparison with Phantom digital who is in the same domain? How does 2 companies stands in terms of their value proposition, future growth prospects, financial track record, valuation and management quality?

Phantom Digital Effects Limited (10-11-2023)

During last year’s Q2 results also, they have compared H1 vs H1. Infact, reporting and disclosures have improved this year with 1) more comparison vs prior like for like periods. 2) good to see balance sheet comparison now with fiscal end.

Anyone has an idea if they are hosting analyst/investor meeting?

Permanent Magnets – Business under transformation? (10-11-2023)

Attended the concall and got the opportunity to ask few questions that were troubling me.

-

Regarding Neodymium supply – since China has restricted exports of critical minerals, the company doesn’t have any supply concerns as we have tie up with ARCI for supplies and even the govt wants pvt companies to participate in utilisation of these.

-

On Tesla entry into India, the management is positive on getting share of business. Didn’t quantify, nor did I ask.

-

Due to aerospace and drone boom the company is positive on demand scenario and they mentioned that their components were onboard Chandrayan and Aditya L1.

-

E-waste Recycling doesn’t pose any threat to their revenue potential and would in turn improve the availability of supplies to the company.

Other point of interest –

The new business investment is 4 Cr and revenue forecast in FY 25 is 7lin the range of 7 to 15 Cr.

Since the metals involved are in the range of Rs 5000/Kg, once the business takes off, the revenue potential can be huge.

Missed parts of the concall so others can contribute.

Aavas Financiers :: Banking on the unbanked (10-11-2023)

From the conf call, I got the impression that they are not making loans fast enough.

On other players esp big ones, i doubt that. They are mainly focused on mainly high ticket size borrowers with credit history in Top tier cities.

Aavas, home first etc. focus on rural loan demand and their process might be completely different.

Basilic Fly Studio Ltd (10-11-2023)

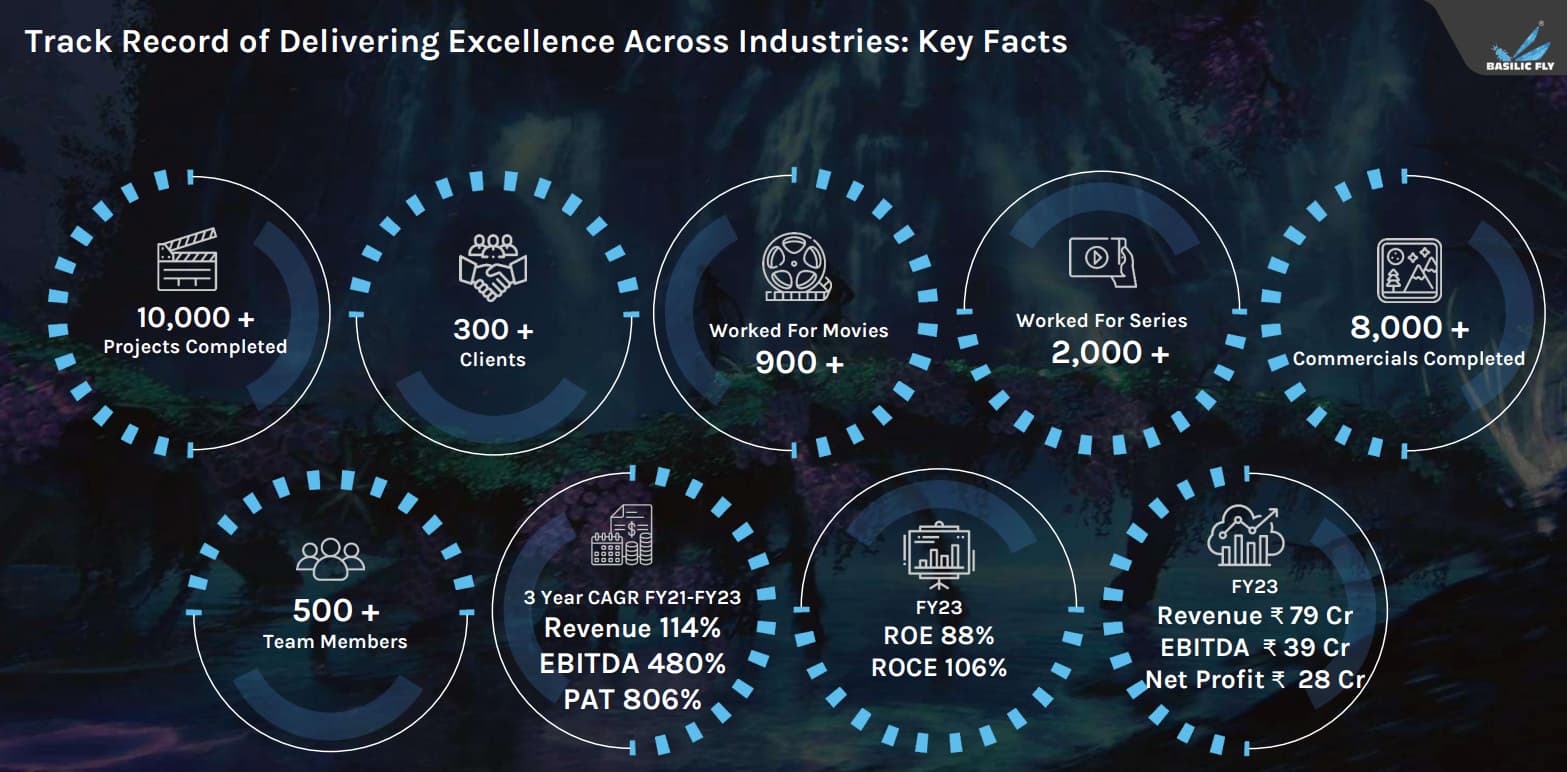

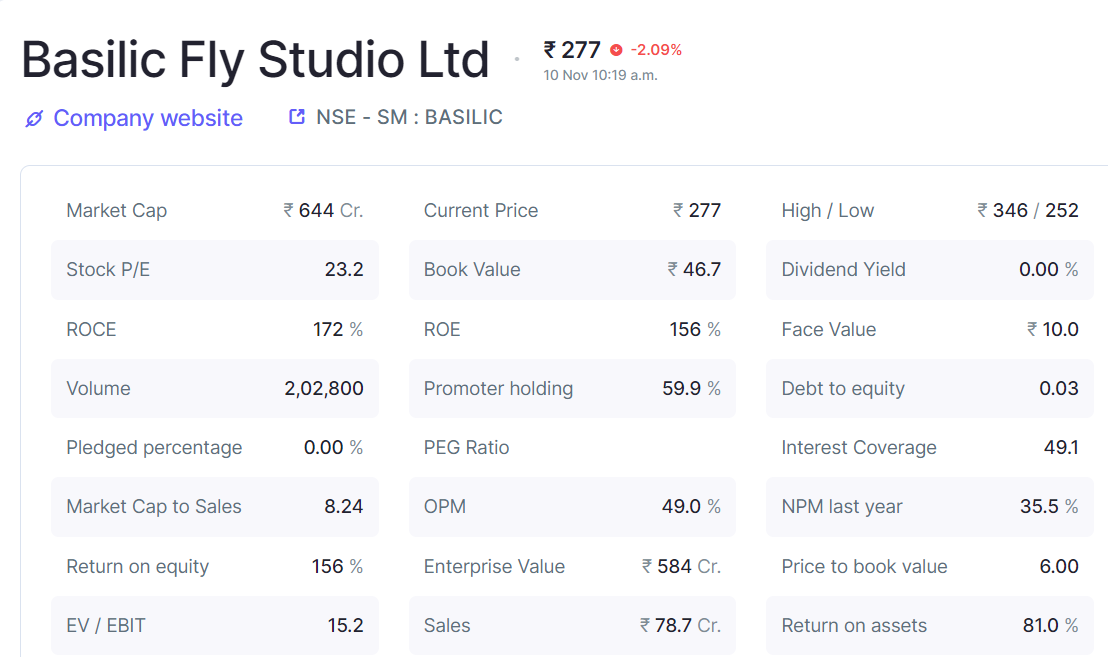

Basilic Fly Studio Ltd. Market cap: 644cr

Business overview:

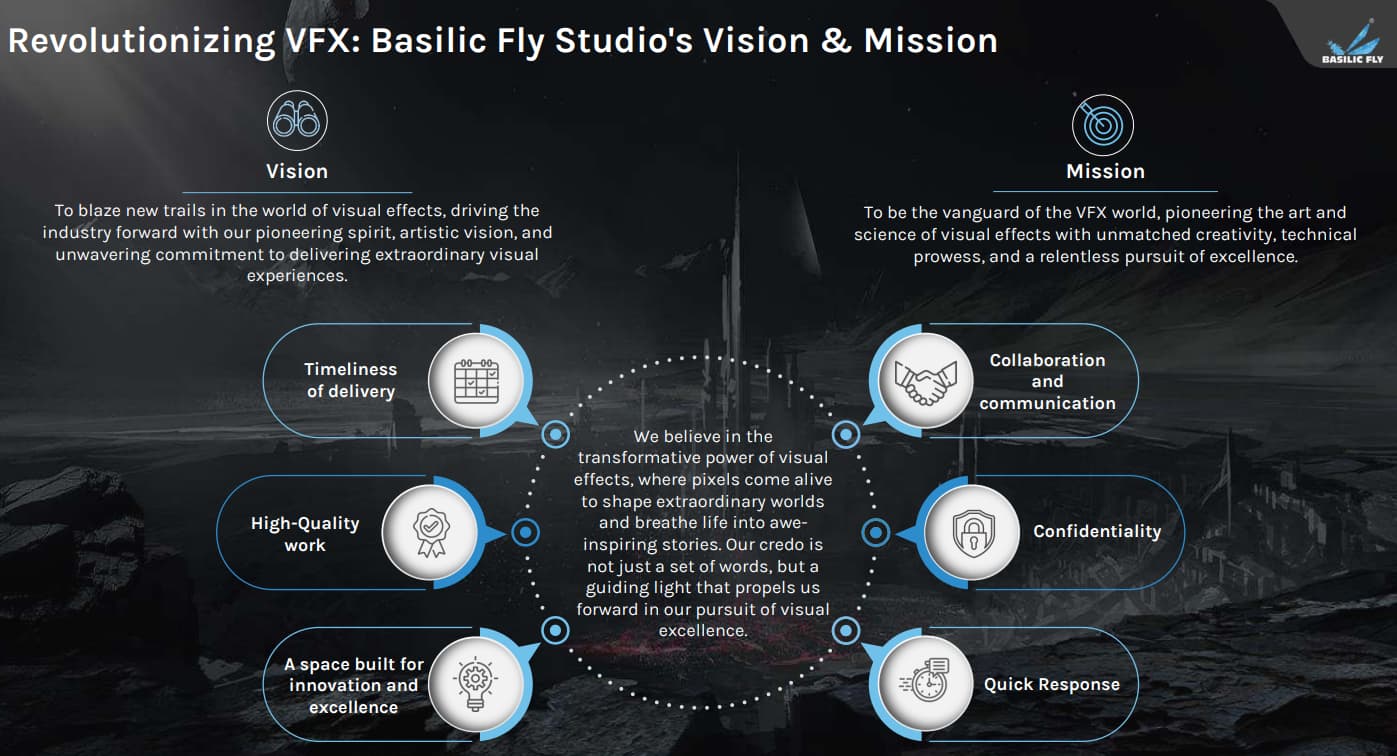

Established in 2016, Basilic Fly Studio (BFS), is a leading visual effects (VFX) studio headquartered in Chennai, India with subsidiaries operating in Canada and UK.

BFS specializes in creating captivating visual experiences and has gained rich experience in pushing the boundaries of creativity and technology to deliver exceptional VFX solutions for movies, TV shows, web series, and commercials.

Renowned for its high-quality output and commitment to investing in the latest technology, BFS has become a top name in the VFX industry. Its team of skilled artists has earned a reputation for excellence, serving clients from diverse sectors and countries. The company’s work spans across various platforms and end-uses, ensuring that every detail is meticulously crafted.

Vision and Mission:

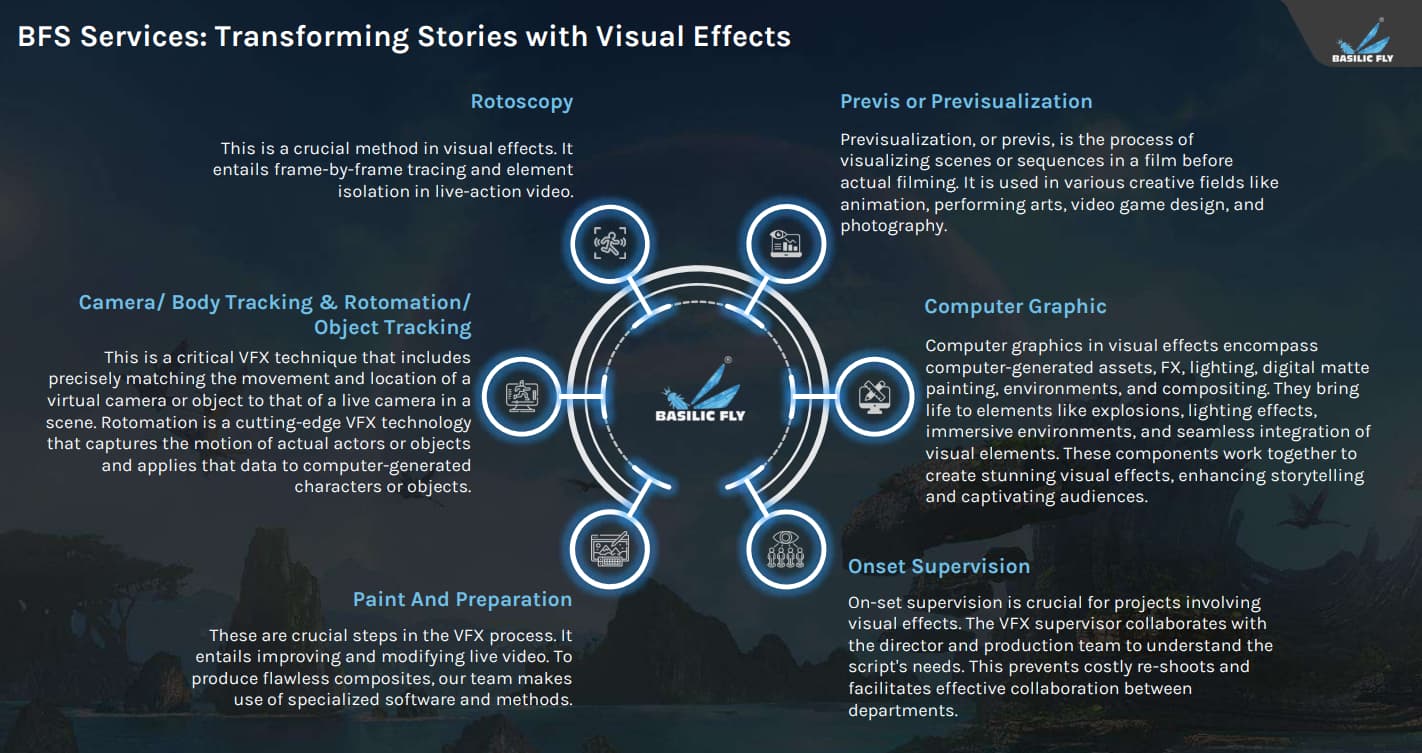

Services:

Growth Strategy:

Total Addressable Market:

According to Boston Consulting Group (BCG) and the Confederation of Indian Industries (CII) research, the Indian animation and visual effects industry has the potential to grab 20 to 25% of the worldwide AVGC market ,it is estimated to generate 75,000-120,000 jobs by that year.

In India, the animation sector alone was valued at INR 2,450 crore ($330 Mn) in 2020. A significant proportion of revenues (70-75%) for this sector in India came from international clients, further demonstrating the growth potential of the global VFX industry.

The Animation and VFX industry in India has the potential for further expansion, as these technologies have gained prominence in various fields, including gaming, education, branding, and marketing. The use of animation and VFX in these sectors has contributed significantly to the growth of the industry in India.

Financial and ratios:

Investment Rationale:

- Sunrise industry with huge TAM compared to company revenue/market cap.

- Top notch clients like, apple, netflix, sony, fox, warner brothers etc.

- Considering to start work for Indian films, OTT, Commercials etc.

- High ROE and ROCE.

- Revenue guidance of 60% with margin of 45%.

- Long runway of growth.

- Company working on Kids entertainment, which can have long episodes of 40/45, which provide stability to earnings.

- Work on entire value chain. Company can provide services for gaming, education videos, Anime ( my son mostly watch Anime) it is a cult in young people.

- I see this company similar to KDDL, RACL gear tech which are in precision work and supply to top notch clients in world.

Catalyst:

- Plan to increase manpower from current 500 to 800/1000 in next year.

- Two new facility in India and two new in Europe+ south korea planned.

- Strike in US for writers have been ended will resume movie/OTT which are halt or due.

- Expansion from IPO money, no need debt as of now.

- Training people to be Generalist who can do many task.

- Automation/copy cat tool to reduce man hours.

- added VFX supervisor/manager in team.

Technical:

- Company listed recently and is under consolidation, stage 1.

- Pivot point at 345 rs.

- For this IPO to get 66cr, 14,000 + Cr subscription was seen with more then 7 lakh application. It was gung ho.

Risk:

- High Growers, can become slow grower without notice.

- Execution risk.

- Inherent risks related to entertainment industry.

- Competition.

- Micro cap.

- Top 5 customers are 59% revenue in FY23, which is reduced from previous years.

Presentation: https://nsearchives.nseindia.com/corporate/BASILIC_09112023183725_IntimationunderRegulation30InvestorPresentation.pdf

Conference call:

https://www.basilicflystudio.com/investor-corner/#bfs-h1-fy24-investors-analysts-concall-audio-recording

I request here members to bring industry specific and company specific insights to understand company/industry better.

Disclosure: Invested and looking to add based on opportunity.

BMW Industries Ltd (Steel Service center) (10-11-2023)

BMW INDUSTRIES Q2 ![]() :(First ever concall)

:(First ever concall)

Bmw industries limited specializes in adding value to semi finished steel products a strategic approach that ensures they’re ability to maintain stable profit margins and offers a safe guard against the volatility against steel market.

This approach allows them to sustain a reliable cash flow by mitigating the impacts of demand and pricing fluctuations

They have an enduring association of over 30 years with tata steel limited.

THEIR USP derives from providing comprehensive suite of services to their customers covering every aspect of the value chain from manufacturing to logistic support a key driver of their success is their advantageous geographical proximity to their clients

In addition company has strategically assembled a fleet of long haul trailers further Enhancing their capability to deliver end to end solutions to their customers

Qoq margins are down due to product mix change however Gross margins remains same

For future growth:

1.planned an expansion in pipes and tubes over the next two years due to the high demand potential in the sector in the phase one which is already under one they will be Operationalized by march 2024 increasing capacity from the existing 204000 metric tonns to close to 53400 metric tons

While in the 2nd phase it should get Operationali by end of fy25 this capacity will be little over One million metric tonnes per annum

The agreement of Gpgc Sheets through the CRM complex is due for renewal by April 2024

This renewal is anticipated to yield about 2000 crs in rev over a span of the following 5 years with annual revenue projection atleast 350cr per year

An agreement of the production of TNT rebars scheduled to continue untill November 2025 is anticipated to generate revenues close to 250crs over the contract period

Their strategy of establishing their own brand involves several key steps including adopting an asset light model developing a robust distribution network expanding their presence in under serviced areas building in-house logistics capabilities and actively working on strengthening our brand value

For reducing carbon emissions company is setting up roof top expansions

The first project is already awarded and should be commercialized in the next three qtrs (cost 21cr)

They’re dedicated to improve their conversion biz by tapping into potential of their existing facility where available and setting up new plant if needed

Looking for brownfield expansions in response to the changing market dynamics.

They want to capitalize their brand value for the upcoming opportunities in B2C sector .

50-50%

50% from internal accruals

50%debt for the expansions

Have already spent 50cr out of the 70cr for the first phse 21crs being sourced from debt and remaining from internal accruals

2nd phase will require approximately 100crs

With rs 50cr funded through debt and balance from internal accruals

The entire capacity is exclusively for tata steel

They’ve already been doing this from past 10years

They are looking at renewing it again by April 2024

Other than gpcp their into conversion of TMT bars as well as pipes and tubes galvanizing for tata steel and

Generally in these types of ebita per tonne?

Their numbers are pretty sustainable numbers as volumes increase and as you know they get the advantage of scale these are very very sustainable numbers.

What competitive advantages do wee have against the fully integrated players?

They’re nothing but a convertor player they take the steel and convert it into billets, and they’re converting into finished steel or pipes or tubes so generally in this

They can only to them based how many billets they give to me as they don’t make billets

The whole capex is exclusive with tata steel

Their USP is their plant is in 5km radius away from the Customer

Lot looking at burning cash.

They’re serving a completely different set of market than tata steel they’re actually In rural undeserved areas that’s a part of their strategy they are supplying a lot of the smaller order lots etc which is completely different from tata tiscon that is s high end branded product. Our product Bansal super is s much more market based standard market product

They try to cover very very sensitive factors that affect their cost

Despite the expansion their net debt will keep going down bcz they’re getting that debt on a fine rate

ON IRR basis their margins will be 17-18%

They’ll be OPERATING LEVERAGE

There is no non compete between them and tata steel

How to plan to grow their own brand?

They’re working with rural part under served areas. It’s a n asset light model they’re getting the production outsourced and not using their facilites to do this and so they basically depending on the monhtly demand they outsource then they brand it and distribute

That helps them to keep asset allocation om this particular vertical very low

Campus Activewear – betting on the India Consumption Theme (10-11-2023)

management rescheduled concall to 8:00-9:00am pre market opening. Looks like it helped to sustain stock price. yet to go through concall.