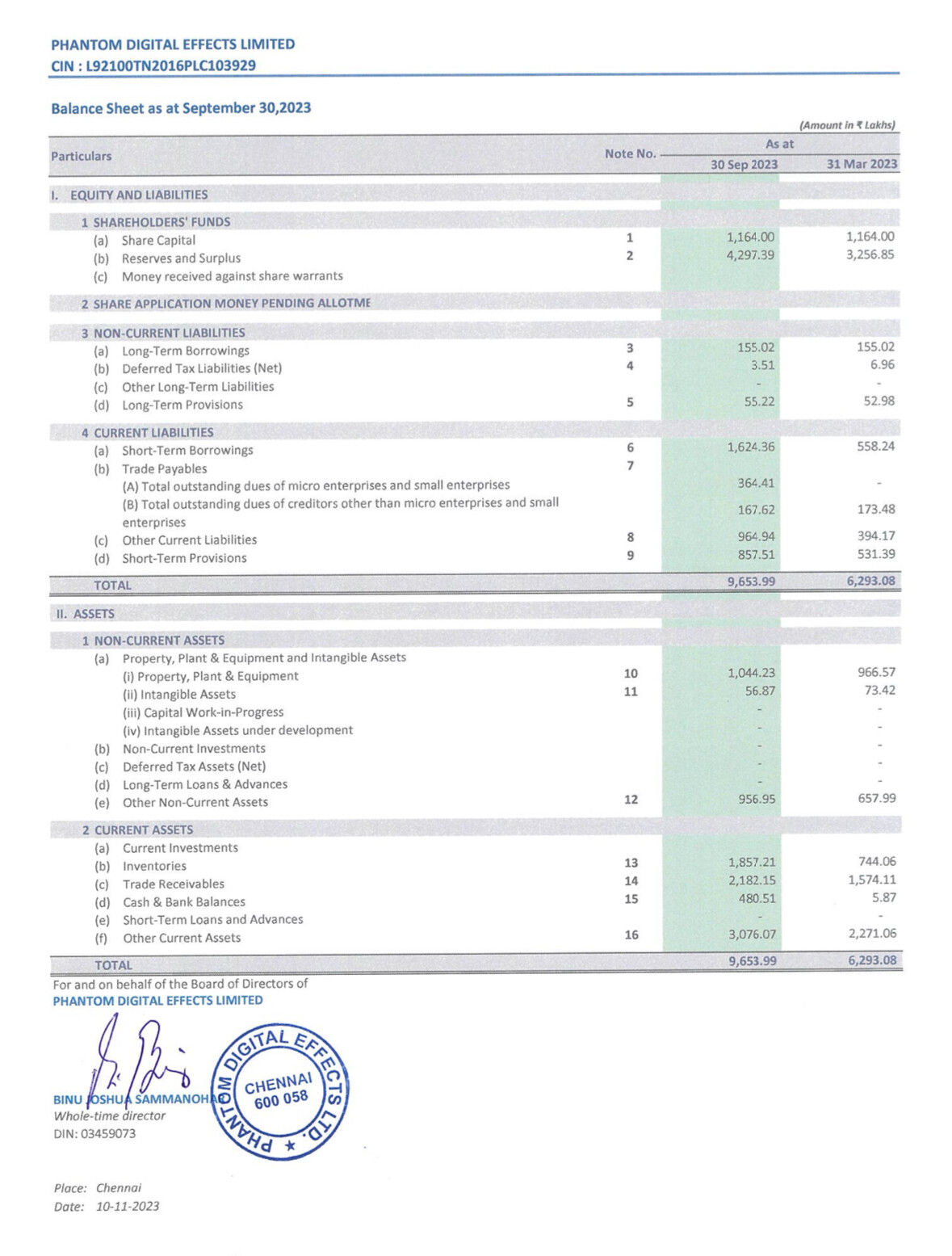

Yes, thats correct

There is however healthy cash generation during the period despite increase in working capital

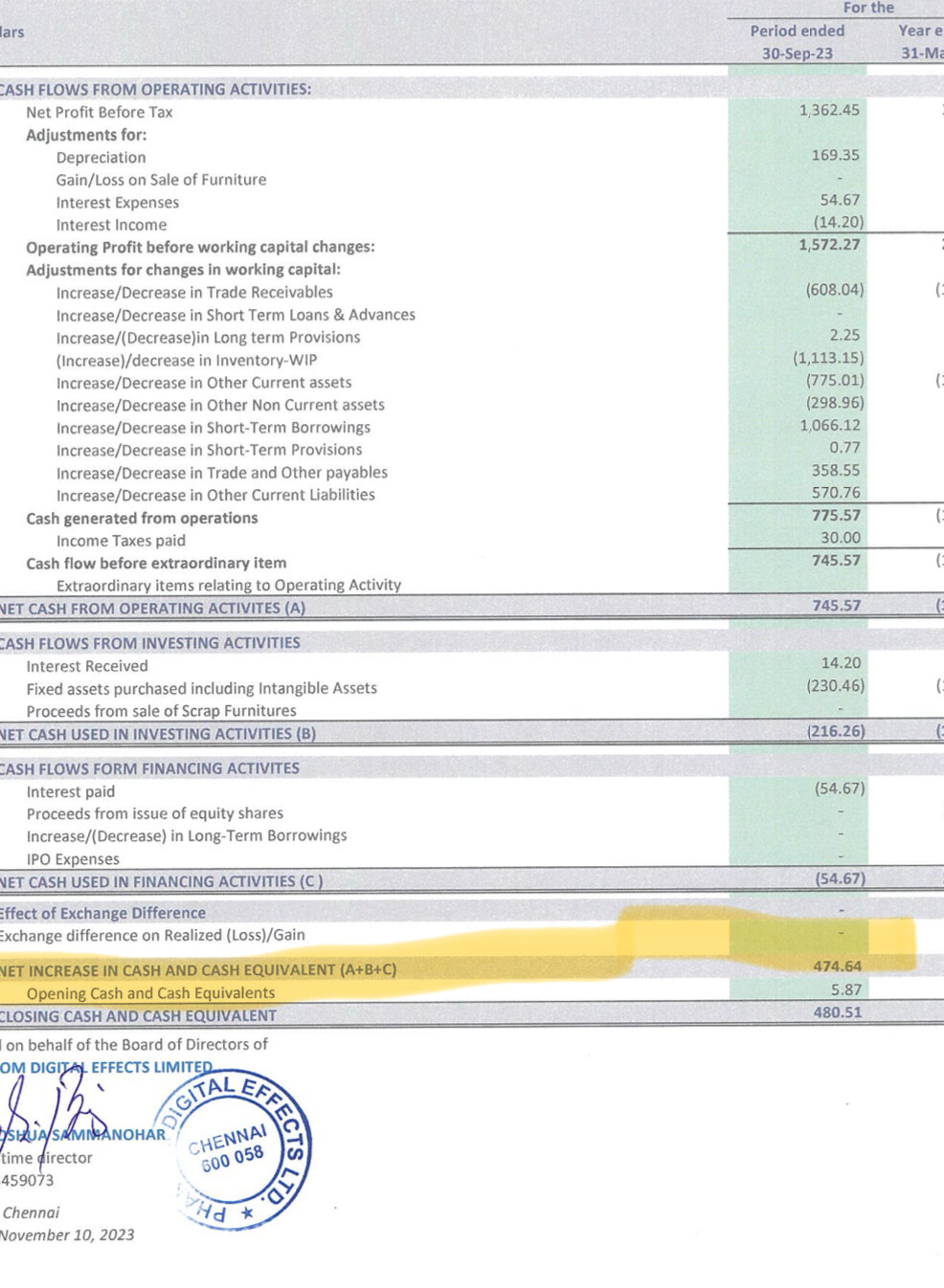

Yes, thats correct

There is however healthy cash generation during the period despite increase in working capital

As you said it is losing market share, do you think it’s due to Lending becoming popular and new players entry?

Reliance with no business in lending entered via Jio Financial

Pidilite which is an Adhesive company also recently announced to setup a lending business.

I see this business as highly competitive and only players with well established disbursement network like Bajaj Finance and Jio Financial can survive in case of any headwinds.

Growth points:

Operators at work.

I have not seen the promised execution in this company and as mentioned by Ravi, the Corporate governance is loose.

This is an example of a company with Sector tailwinds but poor management.

It’s not telecom industry. There are tonnes of home finance companies. AAVAS focuses on folks who may not have credit history and low ticket loans. But with stringent checks.

Based on the conference calls, looks like it’s losing market share. That’s why it went down. They have sales force of 3500 and doing two loans in a month of avg 12 lac loans. You can guess where the growth will be. Also their sanction to disbursement went down to 80%.

I’m not sure why that is significant.

The real question is the management claims they are a conservative lender. Is that a real reason or ploy to hide their inefficiencies, only time will tell.

Ascendant

Main item we need to track is new order. Orders in hand will be executed sooner or later.

Company do not do conference calls or investor interactions, so difficult to find what is going on inside.

Disclosure: Invested.

Also short term borrowings and receivables have gone up sharply. Will the be a concall?

Thank you @vikas_sinha

Thank you @vikas_sinha

Company has generated free cash flow of around Rs 120 Cr and has now announced a CAPEX of Rs 128 Cr.

Reason

To maintain and cater to the growing demand of our customers.

Capex will be completed in next 24 -36 Months.

Exisitng capacity is 305 KL.

Proposed capacity 207 KL.

Current Capacity utilisation 62%.

Take away points:

Free cash flows generated is being utilised for CAPEX. Company is presently debt free and future CAPEX will also not require any debt as frees cash flow will be sufficient to take care of expansion.

Current capcity utilisation will further increase from 62 % to 90% there by operational leverage will start playing to further improve margins.

Company is having visibility of future growth.

Efficient captial utilisation.

CAPEX investment seems to be chanelised in higher margin products.

Management walks the talk so we can easily infer that Company is having visibility of future orders and therefore increasing capacities. It also ratifies the point that vendors have trust in Neuland.

I look forward for above criterion in compounding stocks.

Disclosure: Invested and will further build position through SIP.

Q2FY2022-23 Quarterly Results

Financial