Any news regarding last result, why suddenly drop in price, result not that bad

Posts tagged Value Pickr

Sumitomo Chemicals ~ After Excel Crop Care Acquisition (10-11-2023)

El Nino, Chinese dumping and channel destocking especially in the international markets badly impacted the Q2 FY24 performance, according to the management. But I will take this with a pinch of salt. For Sumitomo, 75 % of the revenues are from India and things were not all that bad in the domestic market. Dhanuka Agritech whose business is largely domestic reported revenue growth of 14 % (which means volume growth should be even higher). Even Rallis reported marginal volume growth. Sumitomo on the other hand reported 3 % de-growth in domestic volumes. Meanwhile, there seems no sign of company utilizing the huge cash pile it is sitting on, as there is neither any large capex nor big bang acquisition on the cards. No plans to returns cash to the shareholders either, at least there was no mention of that. Everything seems to be move very slowly in this company. Perhaps that is the Japanese style of working.

Anyway, some highlights from the concall:

-

Revenues were down 20 % YoY for the quarter overall.

-

Exports dropped almost 50 % in the first half, about 25 – 30 % in volumes and 25 – 30 % in price. Exports were contributing 19 % of revenues in H1 FY23 and now down to 11 % in H1 FY24. LATAM demand has been hit.

-

Domestic business showed 15 % total fall of which 3 % is volume and 12 % is price drop.

-

Company was able to consume all the high-cost inventory that it was carrying as of 31 March 2023 by the month of July

-

Two projects for 5 new products: The first project at Bhavnagar facility has commenced production for a global proprietary product. The second project at Tarapur facility involving multiple EHD products has started commercial production recently. Both these projects are expected to generate some revenue in FY24 but major ramp up only in FY25

-

In domestic business, we launched three herbicides, one insecticide and two fungicides in the first half of this financial year

-

One analyst said in the last 3 – 4 years, we have launched 25 to 30 products but they have not scaled up

-

Glyphosate volume increased 5 % during the year but prices dropped 23 %. Domestically in Glyphosate, there are hardly 2, 3 major players. Exports happen in H2 but they are not very big. The ban proposal will die its own death, most likely.

-

Animal Nutrition business volume increased 31 % in H1 current year

-

One analyst noted that the Environment Health business (EHD) has not grown much last one or two years. Management blamed it on destocking by clients like Godrej, J & J etc. and said things will improve in the coming months.

-

Barrix acquisition – one analyst noted that while the technology is not that new, the acceptance in the Indian market is also not that much. So it will have to be sold globally only. Management said in India this is approximately INR 400 crores to INR 500 crores market today, which is spread across several unorganized players and there is no single large player who is having a very good national level presence, having very good technology.

-

Normalized capex for the business is around 15 % of EBIDTA. Project specific capex if any will be over and above this.

-

One plant which manufactures Quinalphos and Tebuconazole was non-operative from the month of April to almost August end.

-

One example of destocking – We sell a huge quantity of Profenophos to Syngenta for global market. And what we were told that there is a full stop, to not increasing even 1 kilo of inventory till 31st December (Just a thought – what if Kumiai does this to PI)

-

One analyst said based on recent commentary or guidance downgrade by a couple of the global agrochemical majors, it appears that at least even in the near term the situation does not seem to be abating.

-

Cash in hand is Rs.1400 crores but no big bang acquisitions. May go for smaller niche companies rather.

-

Dahej land is very big and the capex will be around Rs.300 crores – spread across 2 – 3 years

-

Promalin – launched in March this year. Lot of hopes on it. It should transform how the apple farming happens in India.

-

The normal industry average growth in a normal year historically is somewhere between 8% to 10%

(Disc.: Holding)

AVT Natural Ltd (10-11-2023)

Posted QOQ better but YoY poor result

Indo Borax and Chemicals (10-11-2023)

result are not good

Saregama India Ltd: India’s premier music publishing label (10-11-2023)

Yes. It is demerged but yet to be listed.

Saregama India Ltd: India’s premier music publishing label (10-11-2023)

It has been demerged, it will list in a few weeks as per the updates on the concall.

HDFC Bank- we understand your world (10-11-2023)

I agree with your concern and had similar thoughts about HDFC Bank. Citi and BoFA both are most likely to outperform HDFC Bank shares going forward especially when returns are measured in dollars.

Banks in US such as Citi, BoFA and bunch of others are trading at very low valuation due to recession fears and other factors but once these clouds clear they can deliver 30-50% return in short time.

Premium valuations for HDFC and other Indian banks will be in question as economy opens up more leading to more competition and these big banks get compared to global peers. HDFC bank’s return for last 5 years haven’t been that great especially when compared in the terms of dollar.

High multiple stocks in India will be in question once compared to similar global companies. Investor can make good money when multiple expansions is combined with rising profits but stagnating profits or even slowly increasing profits can lead to multiple compression.

Goldiam International : A rare shareholder friendly and debt free Jewelry company (10-11-2023)

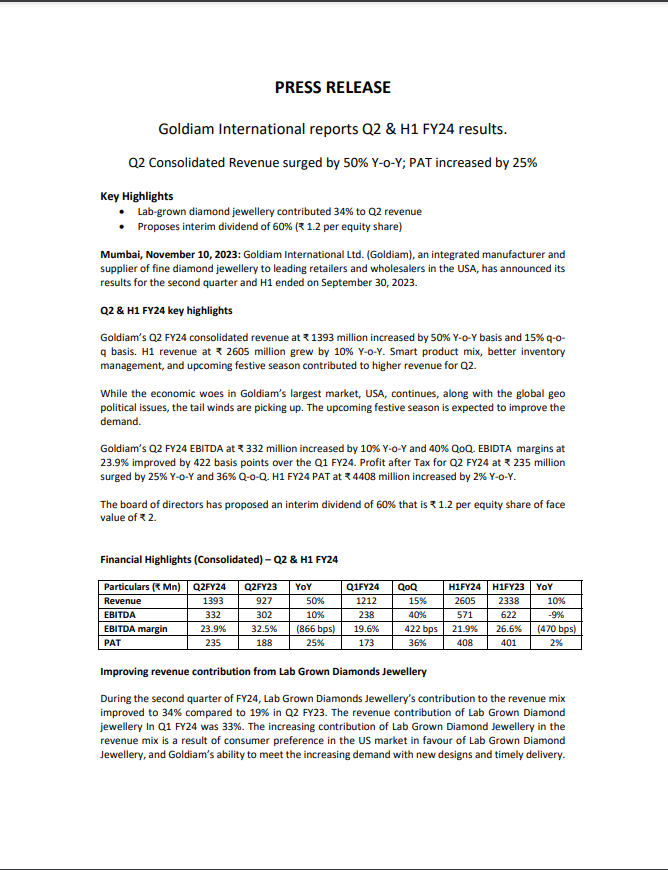

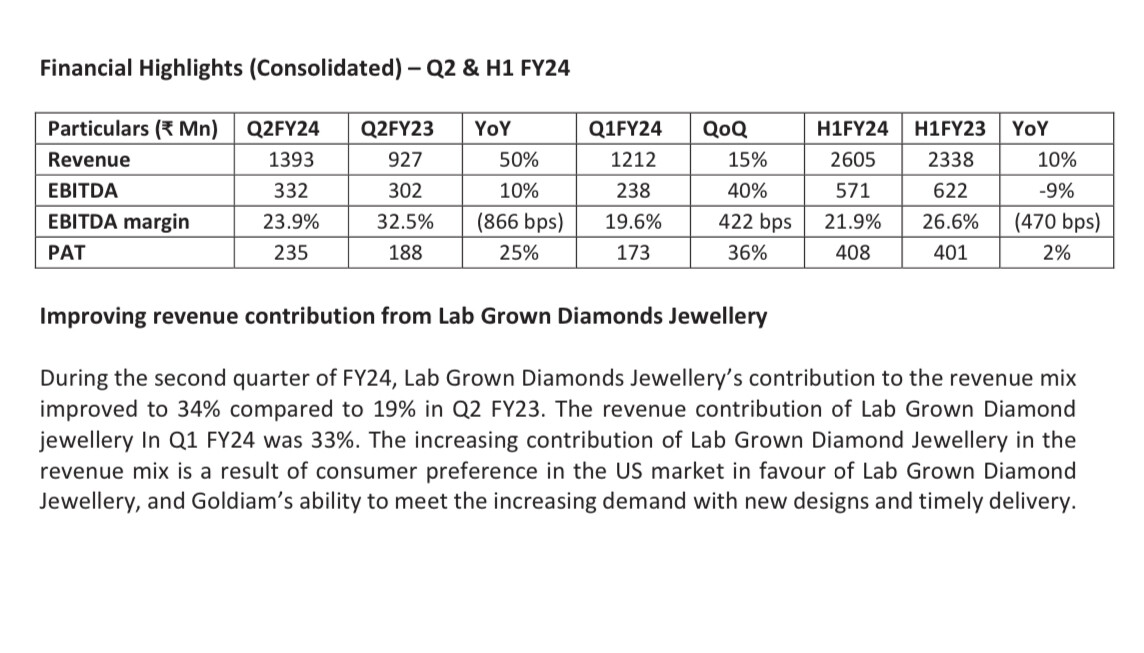

Goldiam has reported its financial results for the second quarter and the first half of fiscal year 2024. Here are the key highlights:

Q2 & H1 FY24 Financial Highlights:

- Q2 FY24 Consolidated Revenue: Goldiam’s revenue in Q2 FY24 reached ₹1,393 million, marking an impressive 50% year-on-year (YoY) growth and a 15% quarter-on-quarter (QoQ) increase.

- H1 FY24 Revenue: For the first half of FY24, the total revenue amounted to ₹2,605 million, showing a solid 10% YoY growth. This growth was attributed to a smart product mix, improved inventory management, and the upcoming festive season.

- EBITDA and Profit: In Q2 FY24, the EBITDA increased by 10% YoY to ₹332 million, with a substantial 40% QoQ growth. The EBITDA margin for the quarter improved by 422 basis points over Q1 FY24. Additionally, the Profit After Tax (PAT) for Q2 FY24 surged by 25% YoY and 36% QoQ, reaching ₹235 million. The H1 FY24 PAT increased by 2% YoY to ₹440.8 million.

Key Highlights:

-

Lab-Grown Diamond Jewelry: Lab-grown diamond jewelry contributed significantly to the revenue mix, accounting for 34% in Q2 FY24, up from 19% in Q2 FY23 and 33% in Q1 FY24. This shift is driven by the growing preference for lab-grown diamond jewelry among consumers in the US market.

-

Online Sales: The revenue from online sales increased to 24% in Q2 FY24, compared to 22% in Q2 FY23 and 18% in Q1 FY24. Lab-grown diamonds, in particular, witnessed robust traction, with the share of online sales for lab-grown diamonds increasing from 3.5% in Q2 FY23 to 12% in Q2 FY24.

-

Inventory Management: Approximately 75% of the inventory (jewelry) as of September 30, 2023, is held by customers as finished stock to be sold in subsequent months.

-

Expanding Geographies: While the USA remains the primary market for Goldiam, the company is actively exploring new geographies, including the Middle East, Europe, Australia, and India for both natural and lab-grown diamond jewelry. The order book as of September 30, 2023, stands at ₹1,650 million.

-

Shareholder Rewards: Goldiam has a consistent track record of rewarding shareholders through dividends and share buybacks. They recently completed a buyback of equity shares, and their consolidated cash and cash equivalents (including investments) stood at ₹2,776.4 million as of September 30, 2023.

Goldiam International : A rare shareholder friendly and debt free Jewelry company (10-11-2023)

Finally an improved set of results. Revenue grew 50% YOY and PAT grew 25% YOY

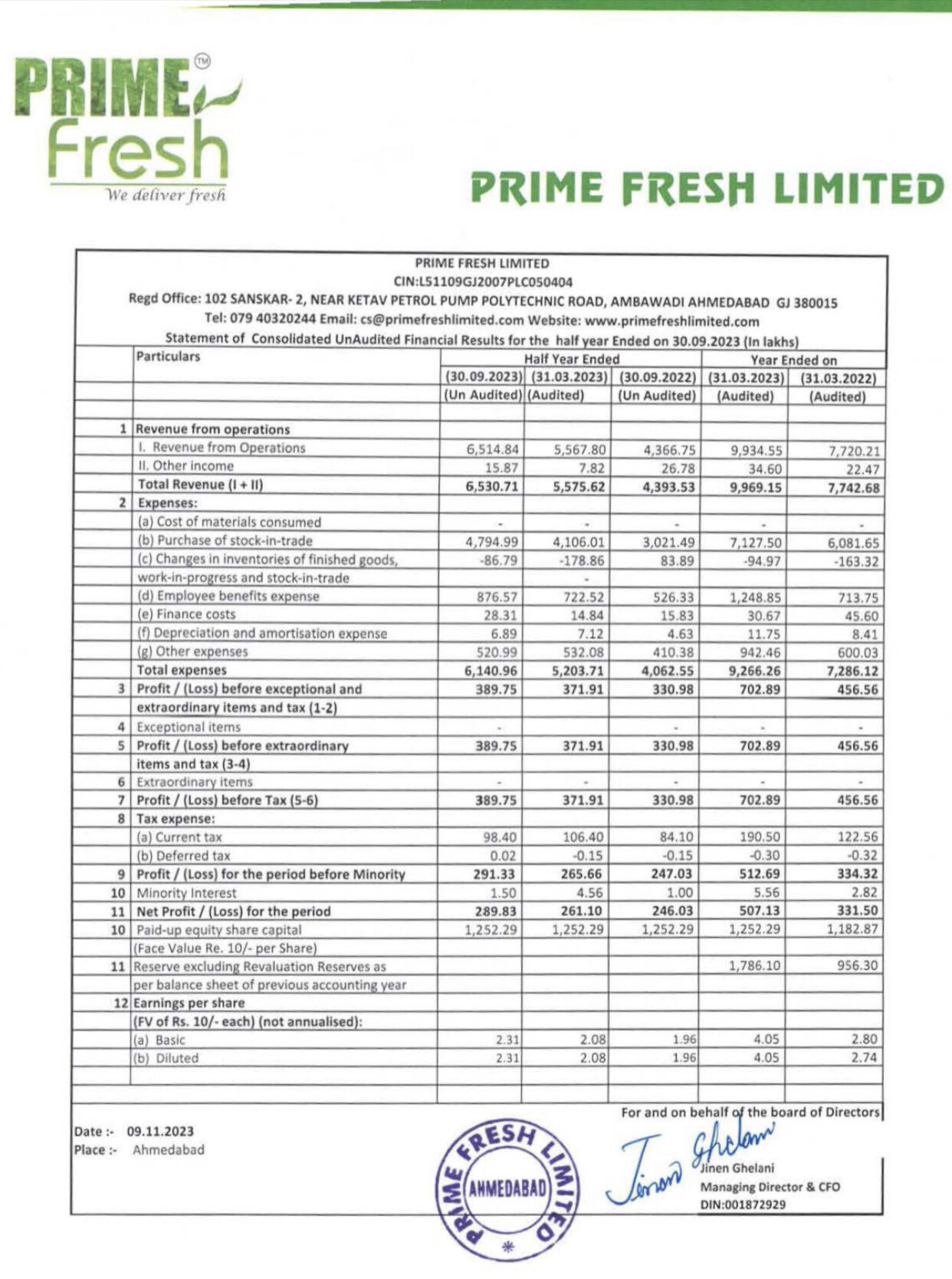

Prime Fresh Limited – Organized Player In F&V Industry (10-11-2023)

Decent results. Revenue grew 32% YOY and net profit 15% YOY