Posts tagged Value Pickr

KPI Green- Turning Sunshine Into Cashflows (10-11-2023)

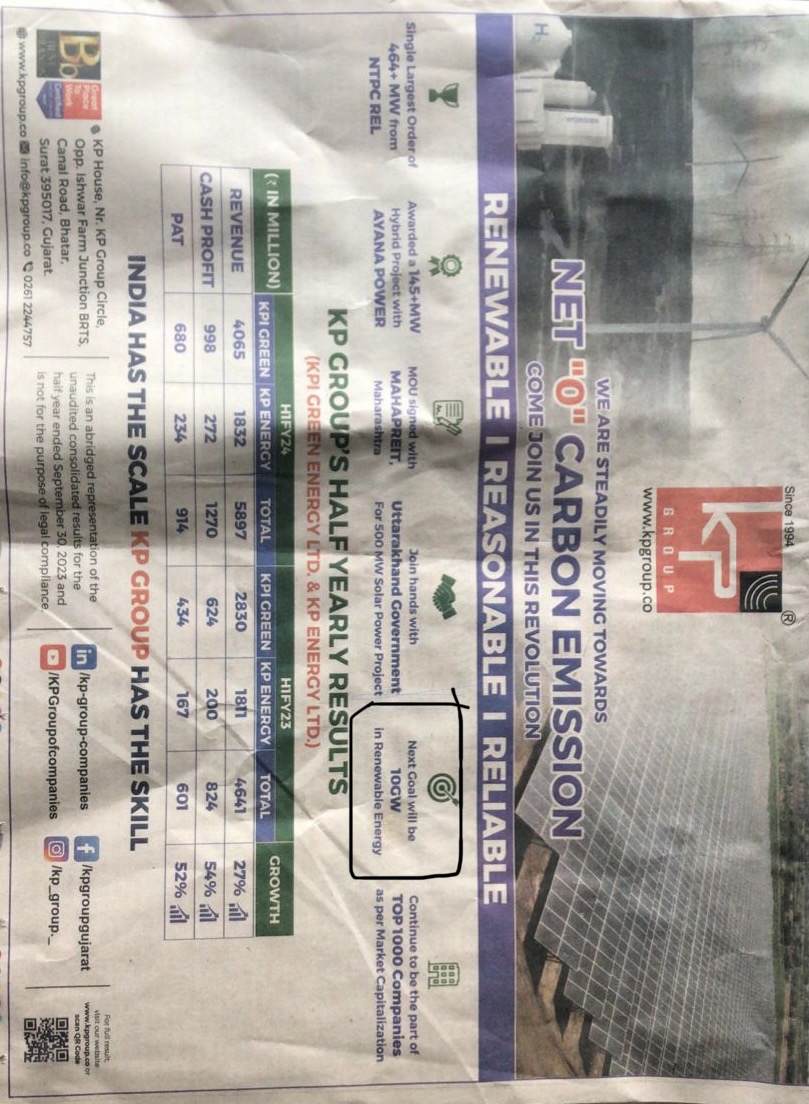

They had a half page advert on Business Standard Front Page yesterday where there was an indication of next target of 10GW (timeline unknown) for KP group vs. 1GW target for 2025. I thought it was interesting. I will go back to find the newspaper and upload the picture here when time permits.

52 week highs and all time highs strategy (10-11-2023)

GREENPLY INDUSTRIES – Monthly Chart: (CMP 186; Currently trading at Nov2014 levels)

- A smaller slant breakout can be seen, volumes have risen in weekly chart, with increasing deliveries.

- A Multi year channel being respected

- RSI heading towards a breakout

- Previous Slant breakout in 2012 led to a bull run in the stock.

- Similarity in setups from 2007-12 and currently from 2018 Jan top to 2023

Safe to assume bullish bias ahead, with bigger slant breakout leading to large up moves.

Companies with 20%+ growth guidance for next few years (10-11-2023)

They have grown 6% this Q and profit is down 6%. Needs 25% CAGR to for 2x-3y

Morepen Labs – a believable turnaround story (10-11-2023)

Latest numbers show two years of negative cash flows from ops. 60 and 90 crores negative in march 22 and march 23 respectively. These are mostly on account of a spurt in receivables and inventory. Of-course these are expected to rise when sales go up. Now my problem is this – from march 2022 and march 2023 sales falls about 100 crores but receivables still keeps rising. If I am not selling the same amount should’nt my inventory and receivables get moderated? I’m seeing inventory has come down but receivables does the opposite. Why? Are they having some disputed collections issues? Can someone throw some light on this?

Thanks.

Hero Motor – Leader in two wheeler (10-11-2023)

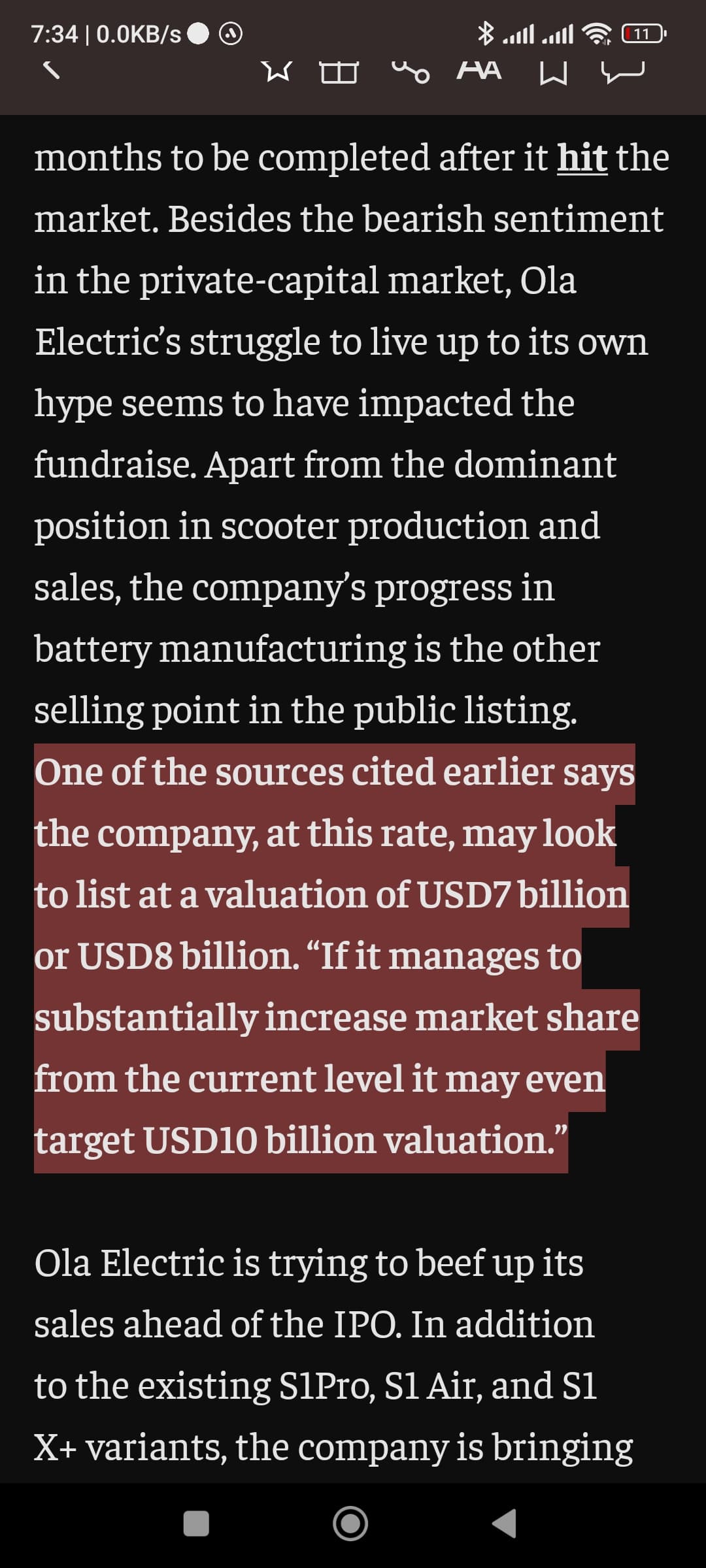

Ola targeting valuation of 7bn USD makes heromotocorp very attractive at this price.

Clean Science and Technology Limited (CSTL) – A clean and green future ahead (10-11-2023)

In my personal opinion, the Management had a cautious tone in the recent Concall w/ some positives and negatives going forward.

Some notes from the Q2’FY2024 Concall by Management:-

Positives

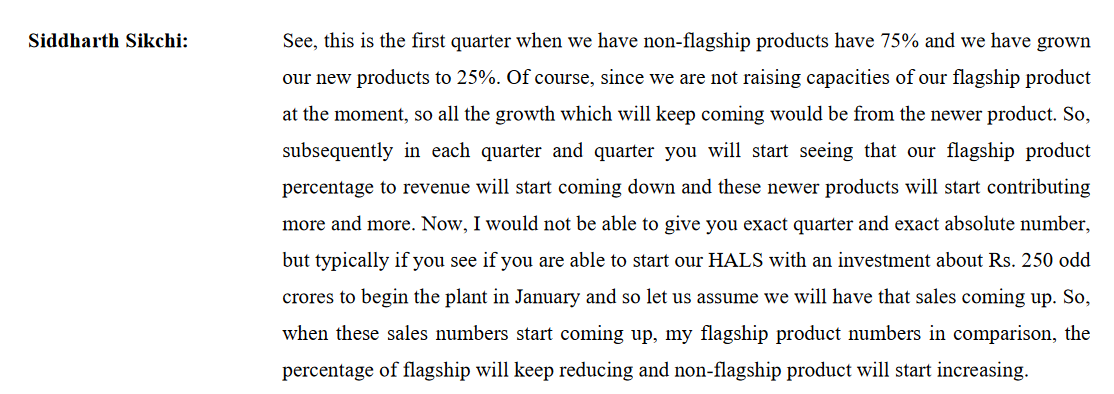

Product Mix Change:-

This is reflected in improved margins this quarter and will help in product diversification going forward.

New Customer Acquisition for HALS:-

This volume should be reflected in the upcoming quarters for Clean Science

Potential Mean Reversion Play:-

Strategic Capex(30Cr) with Large Revenue(100Cr):-

Negatives

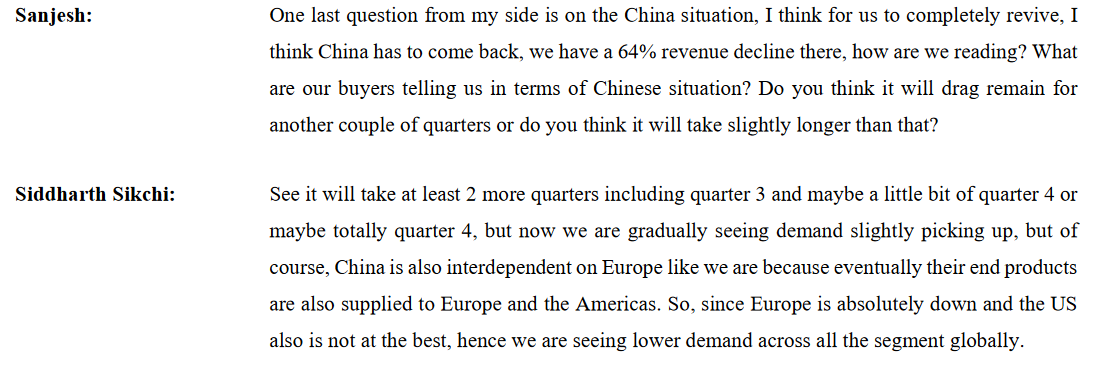

Destocking Pressure to continue:-

This should continue for a couple of quarters

Demand Environment continues to be weak:-

Under performance of Performance Chemical Segment:-

Summary:-

- The valuations of the company continue to be a bit elevated.

- It is a debt free organization with all the planned CAPEX to be funded from internal accruals.

- The overhang of management bringing the stake <75% is done and FII have increased the stake over last 2 quarters in the company.

- Demand environment and destocking situation will potentially result in some headwinds in coming couple of quarters.

Innovators Facade Systems Ltd (10-11-2023)

Exceptional Half yearly result, Company is on the right track. Long way to go…

Disc . Invested

Ambika Cotton Mills (10-11-2023)

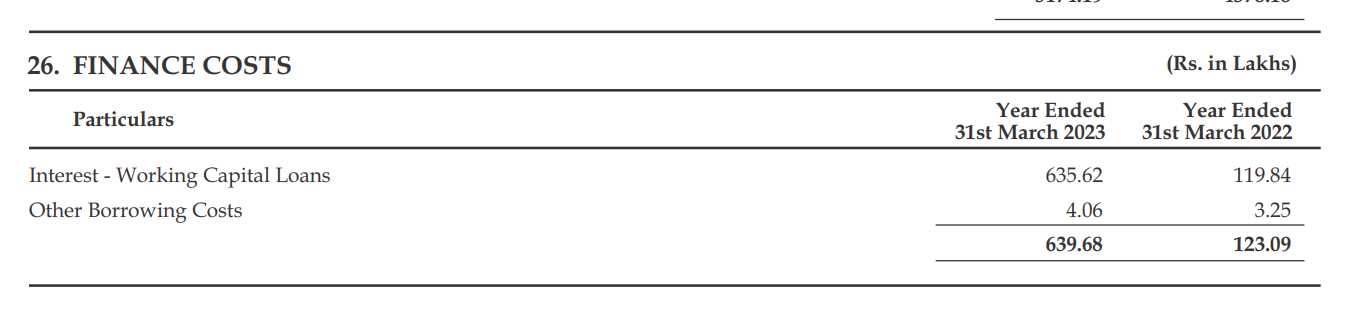

I believe the reference was to Working Capital Loans. See Note 26 in the latest Annual Report as an example.

The short version of my answer is – without any disrespect to the Chairman, I think interest costs have risen simply because interest rates have gone up worldwide – and most definitely in the U.S. I don’t think it mattered whether the reference rate was LIBOR or SOFR. For detailed response, read on.

The interest on most Corporate Loans are charged as Reference + Spread. Earlier, this reference rate was LIBOR. So if LIBOR was 0.5% and the bank decides a spread of 1%, the loan would be quoted at a floating rate of 1.5% (LIBOR being the floating component). Recently, LIBOR has been abandoned and has been replaced by the Secured Overnight Funding Rate (SOFR). More on why LIBOR was abandoned here: What Is Libor And Why Is It Being Abandoned

You can check out recent history of SOFR rates here: Secured Overnight Financing Rate Data – FEDERAL RESERVE BANK of NEW YORK

This clearly show that SOFR rates have moved up from around 0.5% in early 2022 to 6% today. My point is that even if LIBOR was somehow retained in wide global use, interest cost would have gone up because LIBOR will have also risen with the general interest rate increases around the world. Anyway, if it’s any consolation, SOFR forward rates indicates a softnening towards 4% (Source), although it might take a while.

To summarize my personal understanding – any sort of leverage or working capital loan has become quite costly. Energy costs are another reason quoted. All of this aligns with the information from the Management that many of their Competitors aborad had to shut down.

Overall, what is the impact on Ambika?

-

Increase in Interest Costs from 2-5 Crores to 10-12 Crores. Although that’s a sizeable increase, not much can be done by the company. All the firms in the industry will be suffering from the same issue.

-

Increase in Energy costs. According to logic provided in this Hindu BusinessLine article, the increase in Energy costs for Ambika could be as much as Rs. 5 Crores. Again, similarly all players in the industry would be facing the same issue. You can find many articles, including this one, where Indian Yarn Manufacturers are protesting the increase in unit prices and even stopping production.

What can/will Ambika do?

-

The increase in Working Capital cost can be partially or fully offset by passing it on to the customers. I don’t think it’s easy to do that when demand scenario is stagnant. I expect it would be possible once demand picks up, whenever that happens.

-

Ambika is installing Solar Panels to mitigate the rise in energy costs. According to the Chairman, the company has spent 40 Crs. to install Solar Panels that produce 8.33 MW of power and this will provide them with an IRR of around 10 Crs. per year. In gross for the coming year, 63 Million units out of 78 Million units required for production will be via internal energy generation (Wind and Solar power). The future plan is to take care of the entire energy requirement for production through internal energy generation. (See Chairman’s speech from the 40:23 mark)

Ultimately, in my mind, these minor cost increases are short term pains and not long term detriments. Ignore and move on.

Kolte Patil Developers (09-11-2023)

Company maintains their presales runrate, however they weren’t able to launch any new project in Q2 as a result of which most sales came from Life Republic. On reported numbers, they are guiding for 1500 cr. revenues in FY24 and 2000 cr. in FY25. Concall notes below

FY24Q2

- No new launches in Q2, as a result sales only came from sustenance inventory (462 cr. from Life Republic out of 632 cr. in Q2)

- Few projects saw realization drop (24K Altura – 8965 vs 9105 in Q1, Little Earth – Kiwale – 4843 vs 4979 in Q1). Is this a cause for worry?

- Ownership in Life Republic reached 100% from 95% post acquisition of 5% stake from minority holders in October 2023, will also need to make some payment to ICICI (125 cr. total payment and then Life Republic township will be 100% owned by them)

- 24k projects: have launched 3 (out of 5 planned in FY24). Have sold out 60%, 20% (in pre-launch stage), and 25% (row house) in these

- Confident of delivering 3mn+ sq.ft in FY24 and book revenues of 1500 cr. (& 2000 cr. in FY25)

- Doing 25-30% EBITDA margin at project level in currently sold projects. This will likely reflect in numbers from FY26. In low rise projects, margins are 40%+

- Construction costs have been locked for next 4-8 quarters for multiple raw materials due to long term construction agreements with vendors

- Exceptional item: Impairment of goodwill (12.4 cr.) on account of merger a subsidiary earlier + reversal of land transaction in Life Republic (6.78 cr.)

Disclosure: Invested (position size here, sold few shares in last-30 days)