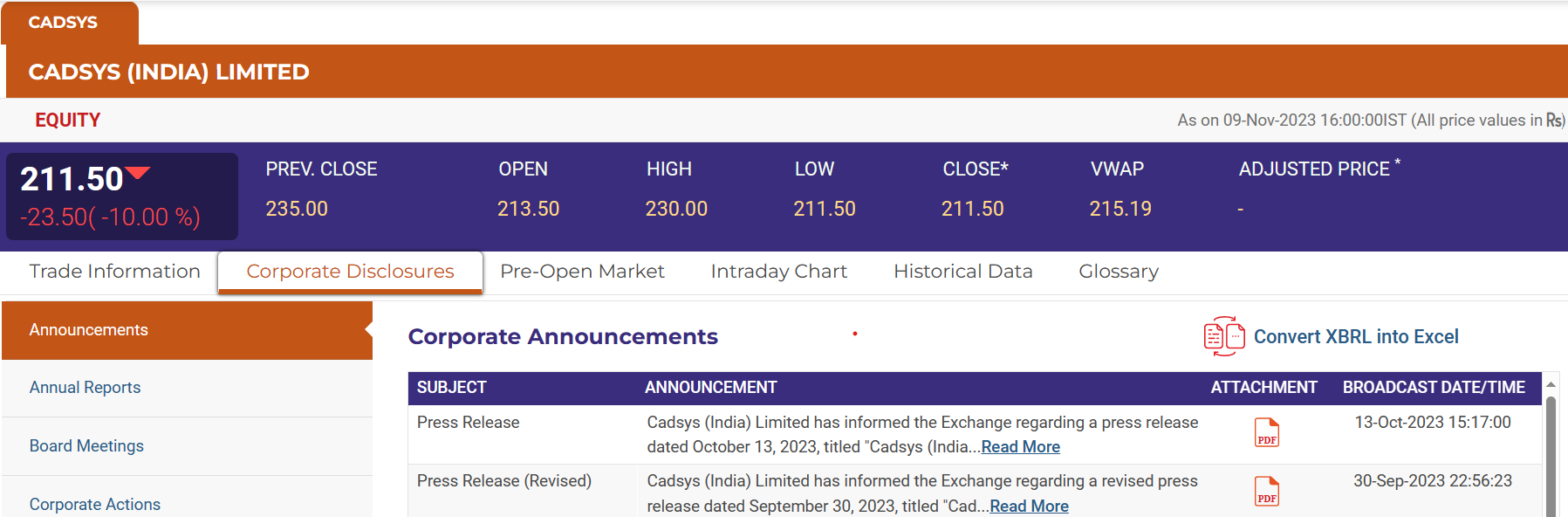

No quarterly compliance and no board meeting intimation yet.

Fire might or might not have affected their primary operations, but administrative side is seeing impact.

As of now the results looks delayed.

No quarterly compliance and no board meeting intimation yet.

Fire might or might not have affected their primary operations, but administrative side is seeing impact.

As of now the results looks delayed.

Has the cloud already burst or is there any air remaining yet?

Recent updates and share price shows clear distrust.

First share price hit lc.

Company gave this

Microsoft Word – Cloud_Investor Meet (nseindia.com)

Now more lower circuits follow.

Random Update:

CLOUD_08112023163143_Reg30Var.pdf (nseindia.com)

Company is very good for Case study. Eagerly waiting to see how thing actually go wherever they are supposed to go.

The platform has been performing without any glitches as far as i have heard.

There is no way the court will force MCX to pay such an hefty amount which is almost all of their profit to a company that has already taken full advantage of the situation.

Its just too extreme to make them pay Rs 150 Cr

They have addressed this issue on concall. Yes, Receivable is increasing from 97 days to 103 days, but Gross margin is increasing by 5%, which is reflated on margin side also.

Q3 and Capex development, to be watching carefully.

Most of the results are out and overall pretty good performance

Shilchar – Phenomenal performance and probably the best of the lot from the pf. There’s also possibility of domestic contribution this quarter as the numbers arent fully accounted by just growth in exports. At current levels though good numbers are discounted for the next few quarters. The promoter too seems to agree and has been selling.

It is generally hard to make great money when promoters are selling. I am not sure who is buying though at 2800 – could be FIIs, as it happened in Apar. They pay very little heed to valuations – a mistake us small retailers cannot afford to commit. I think at 2800 this is a very risky buy. I have been selling and intend to hold around 3% as an investment position.

Garware – The PPF contribution is going up and the 118% utilisation and long-term contract with XPEL are all great signs. The drop in IPD revenues played spoilsport though (32% decline in revenues) and so the numbers appear flat. It is however surprising though that the commodity part of the business has performed poorly when Cosmo/Polyplex seem to have done better QoQ. I was expecting a explosive growth in earnings here like Shilchar, so it is a bit disappointing. Like Shilchar, I had big allocation here which I have been reducing due to valuations entering fair value zone (1500+). I will leave a 3% investment position when am done reducing.

I did not expect this sort of runup in Shilchar (doubled in a month) and Garware (50% in 2 months) so overall these two have been good trades. The momentum could very well carry them further in this market.

Goodluck – Pretty solid performance here too YoY. The big bottomline growth QoQ though is attributable to higher tax paid last quarter. This business seems to have lot of tailwinds and could continue surprising. I intend to hold on to this trade as is long as the tailwinds sustain

PML – Flattish, given the valuations and continues to remain expensive. There is also guidance of EV growth softening but smart-meter demand picking up in the note that came with the results. Maybe the two will balance out? They have also done capex for the alloys business to manufacture superalloys used in aerospace and defence. More importantly, looks like Quadrant JV too proceeding well and sales should start commencing from Q4. However they seem to be starting with magnetic assemblies and not manufacturing NdFeB magnets – which might be a good thing as it might be less capex intensive and probably make higher margins (hoping). This position has now turned long-term for me. The overall size of the position though has shrunk with the other trades in rest of pf working out better

Mazda – Pretty good growth here too but margins are lower compared to last 3 quarters and continues to remain cheap (now trading at 16x). Food business seems to be ramping up well. I think margins here will continue to improve as utilisation goes up.

Ceinsys – Pretty good results. The receivables situation seems to have improved too. This reminds me a lot of my trade in AurionPro (somewhere in this thread) which is currently trading at fancy valuations. I didnt hold it long enough though as I had concerns on the business quality there (regular write-offs). I feel AllyGrow as a business deserves better valuations and so will hold and see it through

Swelect – The softening prices of modules and dumping from China has probably affected the numbers. Until there’s protection from dumping, am afraid this situation will continue. Its a small position I continue to hold to follow if situation changes – especially if policies favor the manufacturers in MNRE approved ALMM list

Taal – Breakout from long-term resistance and re-test.

The company now doesn’t do air chartering so its main line of business is Taal Tech which is a wholly-owned subsidiary of the company which will soon be merged with Taal Enterprises. So for all intents and purposes, this is now a Engineering services firm. The AGM transcript is a good read. They have about 60 customers and largely export oriented and margins are pretty healthy. Current quarter results are pretty good and valuation reasonable.

Overall this results season lot of businesses are doing quite well. A lot is being priced in though with lot of small/microcaps trading at even 30-40x and some SMEs are at stratospheric valuations. We can’t fall into the trap and storify liquidity driven price runups though and indulge in BaaP behaviour (performance of Marcellus’ little champs portfolio is a good reminder of what happens when we do)

I am ~30% cash so views could be somewhat bearishly biased. It helps me stay hungry and look for good bets (selling in Sept 1st week was what led me to buy Shilchar for eg.)

Disc: Have positions in Taal between 2200-2400 and the rest as disclosed in this thread and in this post. Not an advisor and I am just a novice sharing my thoughts.

Out of curiosity:

Can someone pls explain how this company pays taxes at such low rates on their PBT:

Highlighted below in yellow:

This coaching business has never made money. @Nitya_Shah I read a brilliant report of him saying that career point and veranda are in almost identical business they also did not made money. Moat lies in the faculty and not in the centers. They can charge but not exorbitantly to turn around business from here.

Still the working capital cycle keeps on worsening due to rise in inventory and receivables. Although none of the receivables have been mentioned as doubtful as of yet, but we need to keep track and find the reason behind this if they are rising at such a high pace

KIRLOSKAR OIL ENGINE LTD

2X-3Y Strategy: Grow 2 times in 3 years

Not sure if he has fully sold all from fund IV or holding less than 1 %… however he has 7% in total as of now… further if he sells, then yes, need to watch… but nowadays even Pabrai is hopping from one stock to another frequently.