I have exited Studds accesories, Lotus chocolate and Borosil Ltd recently. I will enter Borosil after demerger.

Current portfolio comprises of

Senco Gold

Magson Retail

Central Depository Services Ltd

I have exited Studds accesories, Lotus chocolate and Borosil Ltd recently. I will enter Borosil after demerger.

Current portfolio comprises of

Senco Gold

Magson Retail

Central Depository Services Ltd

The Journey for sure from this stage (FY24) will not be as smooth for them which was a year or two later beacuse it was all pentonic led growth and export in new regions.

What we can expect (that would effect the share price) is a more sustainable growth with maket penetration gianing market share from their competitors like flair,cello,doms(which will be there soon in the listed place)

And if they want to achieve the robust growth it is only possible by either developing a new pentonic (grow new product portfolio) or massive sale of DELI products (because GPM on them looks decent)

What are your views??

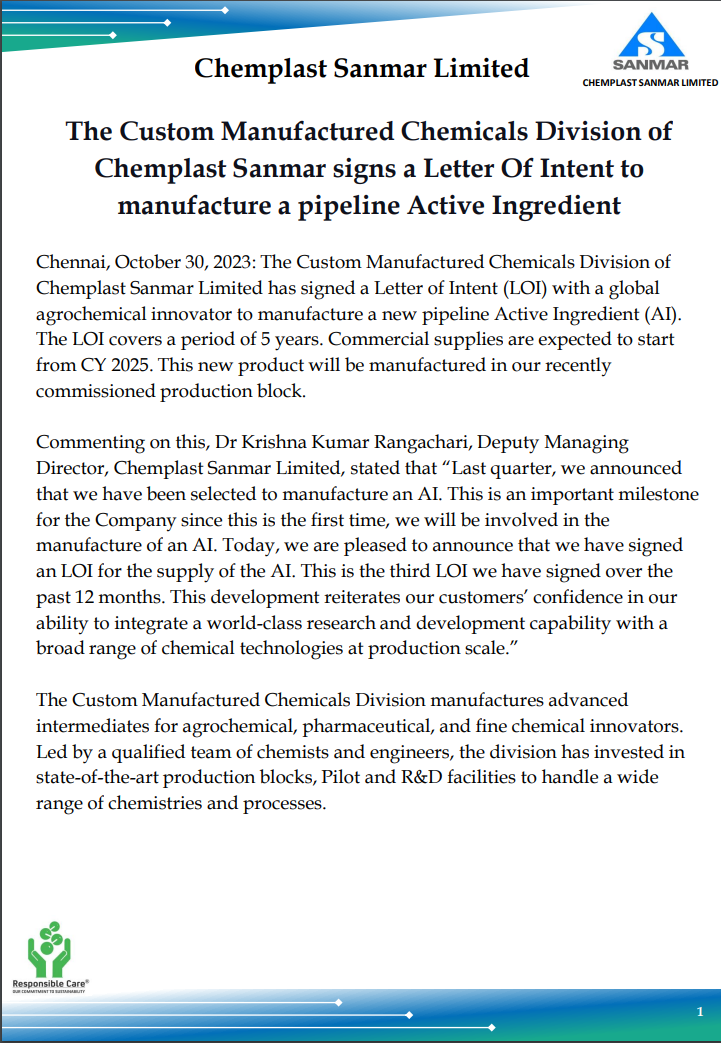

The Custom Manufactured Chemicals Division of Chemplast Sanmar Limited has signed a Letter of Intent (LOI) with a global agrochemical innovator to manufacture a new pipeline Active Ingredient (AI).

Write up on Magson Retail by Progressive Grocer India Edition of October,2023.

https://nsearchives.nseindia.com/corporate/MAGSON_03112023164308_MagazineWriteup.pdf

Future outlook by management

“By 2026, MagSon plans to add 25 new stores in the stable. These stores will come up in different parts of Gujarat, Madhya Pradesh, Rajasthan, and Maharashtra, where the brand is already currently operational and has existing stores.

Most of these stores will operate under the franchise/shareholder model followed by the company since it turned public. They estimate that their turnover will touch around Rs. 120 crore in another two years from now.”

Pentonic’s share reducing this quarter really stuck out to me. It can’t just be because of reduction in exports to Myanmar and Sudan. I might be wrong but I don’t think they sell mostly Pentonic in these countries.

The management seemed very defensive this time with their guidance as well. Revising it down to 700cr (assuming max growth of 20% on FY23’s base) in FY25 from the previous guidance of 750cr in FY25.

We can arrange for a Pune meetup. I can also give a presentation on News based stock screener platform that I have been developing.: https://causalityarrow.com

Not sure if the comparison is mangoes to mangoes.

NSE has about 185 stocks on F&O apart from the Index F&Os (Nifty, Bank Nifty and Fin Nifty being the most prominent ones) as against Sensex F&O being the only F&O product that is being actively traded in BSE. Bankex is still in its nascency.

Eitherway I believe comparing the market share of any of these product is a futile exercise as the products are all different and have independent standalone reason why market participants trade in each of these.

BSE management has done an excellent job in convincing the market participants on the underlying strength and purpose of trading in Sensex contracts. We are currently seeing early signs of Bankex contracts also gaining momentum(though Bankex is not significantly different from Bank Nifty in terms of its underlying).

BSE has a huge opportunity in terms of gaining market share both on derivatives and cash as they have negligible market share currently. Its all about listening to market, introducing the right products, making the trading attractive for participants, providing seamless connectivity and delivering fool proof infrastructure support.

The current management is driven by a purpose to make BSE a vibrant place to invest, trade and hedge by the year 2025 – market seems to be convinced by the actions of the management so for, which is visible from the way price has moved over the last 3-4 months. Now all they need to do is to keep the momentum going and continue to capture the imagination of the participants.

AJ

Disclosure: Remain invested. Views are biased.

Company results on 10th November. I am looking to double position if company can generate profit at least equivalent to last quarter.

No one is talking about the dismal performance of quarterly results. Is it just one off case? or headwinds to continue in the coming quarters?

PSP Projects Q2FY24 Concall Summary