Summarizing the growth triggers by the managment:-

1-Exapansion of new PENTONIC product portflio (launch starting from Q3FY24)

2-Growth in sales of Other stationery products (exluding writing) under the name of DELI

3-Market Share growth in higher margin products ultimately showing up on their GPM.

4-Leveraging their export network to introduce international markets (espicially Africa) to Linc products focusing on low ticket size and writing instruments.

Posts tagged Value Pickr

Linc Ltd: Writing the future of Bharat (03-11-2023)

Krishca Ltd : A SME offering steel strapping Solution (03-11-2023)

KRISHCA.pdf (3.1 MB)

Posted good set of results. Half yearly Revenue – approx 48.5 cr (Last year Revenue – 72 cr)

But, in their statement it appears they are comparing half yearly revenue (Sep 2023) to Full last year revenue (Apr 2022- March 2023).

This created a confusion among the investors. And hence,we can see selling in the stock.

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (03-11-2023)

Hazoor Multi Projects Limited (03-11-2023)

Business Overview:

Company was initially engaged in construction of residential projects. In FY21, company changed its line of business and is now mainly engaged in infrastructural development and works as a sub-contractor in executing various national highway road projects awarded by government authorities such as Maharashtra State Road Development Corporation Ltd and National Highways Authority of India. Apart from this, company has also started the EPC contracting business.

New Promoter:

In October 2021, Mr. Pawan Mallawat acquired 25.93% share of company (through direct purchases and his company Keemtee Financial Services Limited) and has since been managing day to day operations of company.

Order Book:

Company’s un-executed order book is at Rs. 1200 Cr. as on August 31, 2022. The increase in the order book is on account of receiving the balance part of work order of Nagpur-Mumbai Super Communication Expressway Limited of more than Rs.1000 Cr from Gayatri Projects Limited and originally awarded to them by Maharashtra State Road Development Corporation Ltd. (MSRDC).

Important Parameters:

Annual Report Analysis by CA Rajesh, who collaborate with me.

Positive:

-

There is phenomenal increase in Company’ turnover and profit that can be seen in financial statements. Turnover increased from 112 crore to 775 crore (Year to year basis) which is very impressive. Profit increased from 2.48 crore to 45.34 crore.

-

The main director Mr Pawan Malawat is not getting any remuneration. Further other director Mr. Dinesh is getting salary of only 6 lakh p.a. which is very nominal considering volume of business.

-

Co has recently appointed chief head / chief engineer for salary of Rs 6.00 Lakh per month which is good sign for aggressive operation of business.

-

Debt equity ratio has decreased from 0.9 to 0.26 which is sign of reducing debt.

-

Debtor ratio, RoCE and G/P and NP ratio has also increased which is also good sign.

-

There is no pending govt dues which is also good sign. Further there is no pending disputed tax liability with government which shows good compliance from Co.

-

Co has completed major portion of project awarded to it by govt.

-

There is no major negative comment by St. Auditor, Co secretary which also good sign.

Negative:

-

The director are getting salary less than most employees. There is no dividend declared except in current year 2023 and back to it declared in 2008. So how director are working without proper pay.

-

Co has appointed Independent director Ms. Pratima with nominal salary of Rs 5000/- p.m. again doubtful. Sebi has prescribed independent directorship for greater corporate governance.

-

The Co is not regularly paying dividend. It means co does not have good cash flow.

-

There is debt receivable of more than 44 crore which is outstanding for long time. In govt contracts, payment are received in 3 months except disputed bills. Even some debt is outstanding since more than 3 years and co has not written off it as bad debt which also not good sign as it artificially shows good picture. This can be ignored as new orders should not have any problem.

-

Auditor has not pointed any irregularity compared to some apparent things which i can see in fin statements and also firm is not big CA firm so question of due diligence arises.

-

Co has negative operating cash flow which is surprising considering increase in such profit and turnover. Negative cash was met by issue of fresh shares as mentioned in report. Means co has incurred and managed operating deficit from issue of capital from public. (This is very important).

Investment Thesis:

-

New management start bringing orders from 2021, it should continue.

-

Current order gives visibility for 1 year of approx. 939 cr.

-

New Orders must come in 1 year time.

-

Promoter should start increasing their stake.

-

Market cap to sales is only 0.26 and PE 4.

-

As of now, no negative in media for promoters as far as I searched.

Risk:

- Micro cap

- Promoter Holding of 26% only.

- Inhered risk of Infra business.

- No new order will consume current order book and there can be no revenue at all.

Note: As old thread was closed, as advised by Moderator, new thread is created.

Disclosure: Have tracking position of 1.5% of my portfolio.

Usha Martin- Coming out of Chaos (03-11-2023)

Usha Martin q2 fy 24 results out.

Sales for q2 fy 24 — 800 cr vs 825 for q2 FY 23. (probably due to moving towards higher margin products and lower raw material costs.

Op Profit for q2 fy 24 141 cr vs 96 cr.

Net profit for q2 FY 24 109 cr vs 79 cr.

Half Year EPS at 6.9 per share. (not annualised)

usha q2 fy 24.pdf (6.6 MB)

Caplin Point Laboratories (03-11-2023)

Very strong guidance. Company targeting for 40-50% growth in revenues in FY24 with stable margins. Increase in revenues targeted through new product launches and higher market share from current products.

Britannia (Buy Commodities, Sell Brands) (03-11-2023)

Britannia Q2FY24 Concall Summary

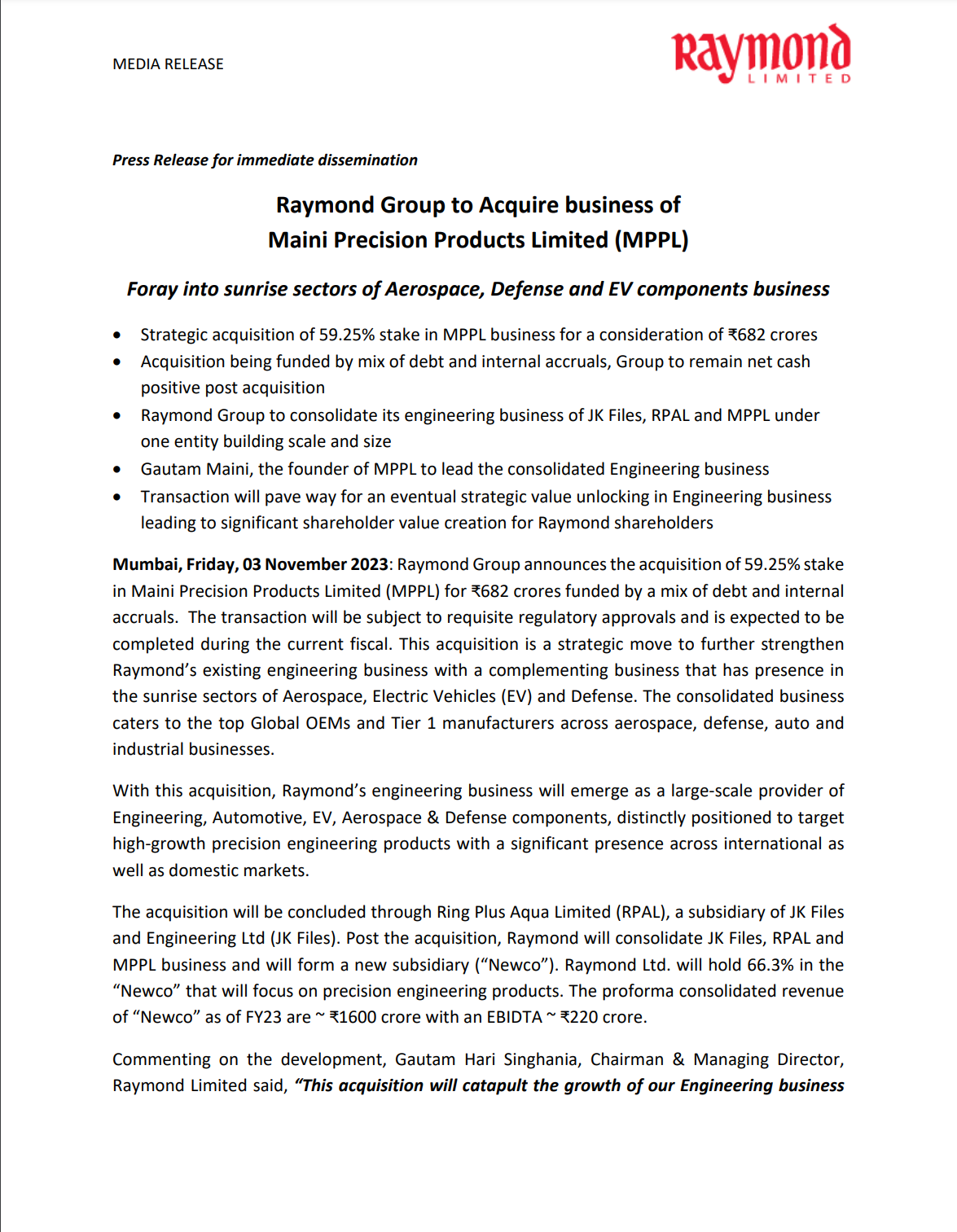

Raymond – The Complete Man (03-11-2023)

Raymond Limited notified about two important updates:

- They’re buying a 59.25% stake in another company called Maini Precision Products Limited (MPPL) for ₹682 crores. They’re using a mix of debt and their own money to pay for it. This will help them expand into growing areas like Aerospace, Defense, and Electric Vehicles (EV).

- They’re reorganizing their engineering businesses by combining them into a new company. This new company will focus on precision engineering products, and Raymond Limited will own 66.3% of it.

This is a strategic move to grow their engineering business and enter new, promising industries. They’re excited about the opportunities this will bring. The acquisition will be subject to regulatory approvals and should be completed soon.

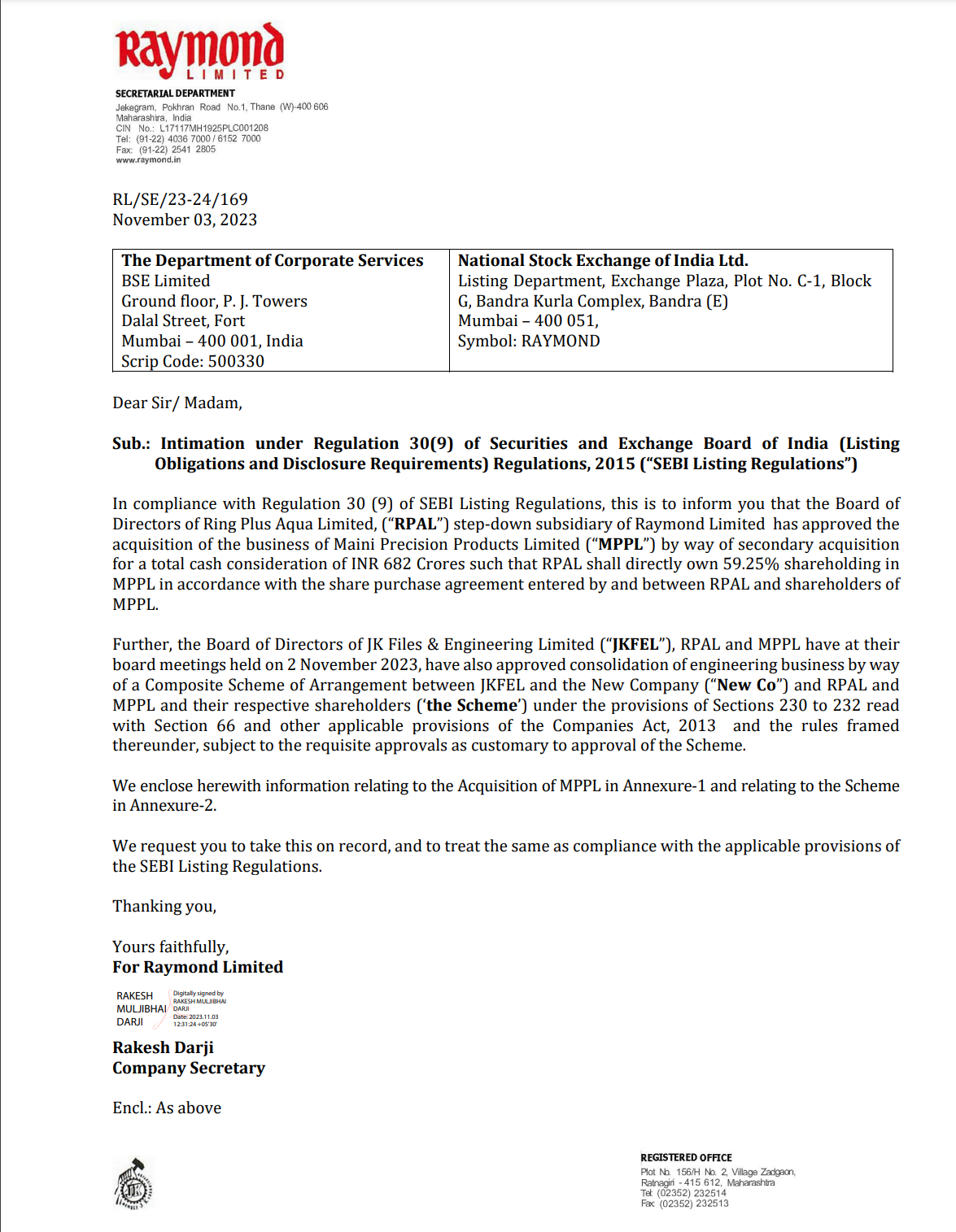

Raymond – The Complete Man (03-11-2023)

Raymond Limited is informing these regulatory bodies about certain business decisions made by the company.

Here’s a simplified explanation:

- Raymond Limited is a company in India, and they are writing this letter to inform the stock exchanges about two important decisions they’ve made.

- The first decision is about a company called Ring Plus Aqua Limited (RPAL), which is a subsidiary of Raymond Limited. RPAL is going to buy another company called Maini Precision Products Limited (MPPL) for a total price of INR 682 Crores (Indian currency). This means RPAL will own 59.25% of MPPL.

- The second decision involves three companies: JK Files & Engineering Limited (JKFEL), RPAL, and MPPL. They are planning to combine their engineering businesses into a new company, and this process is called a “Composite Scheme of Arrangement.” It requires certain approvals.

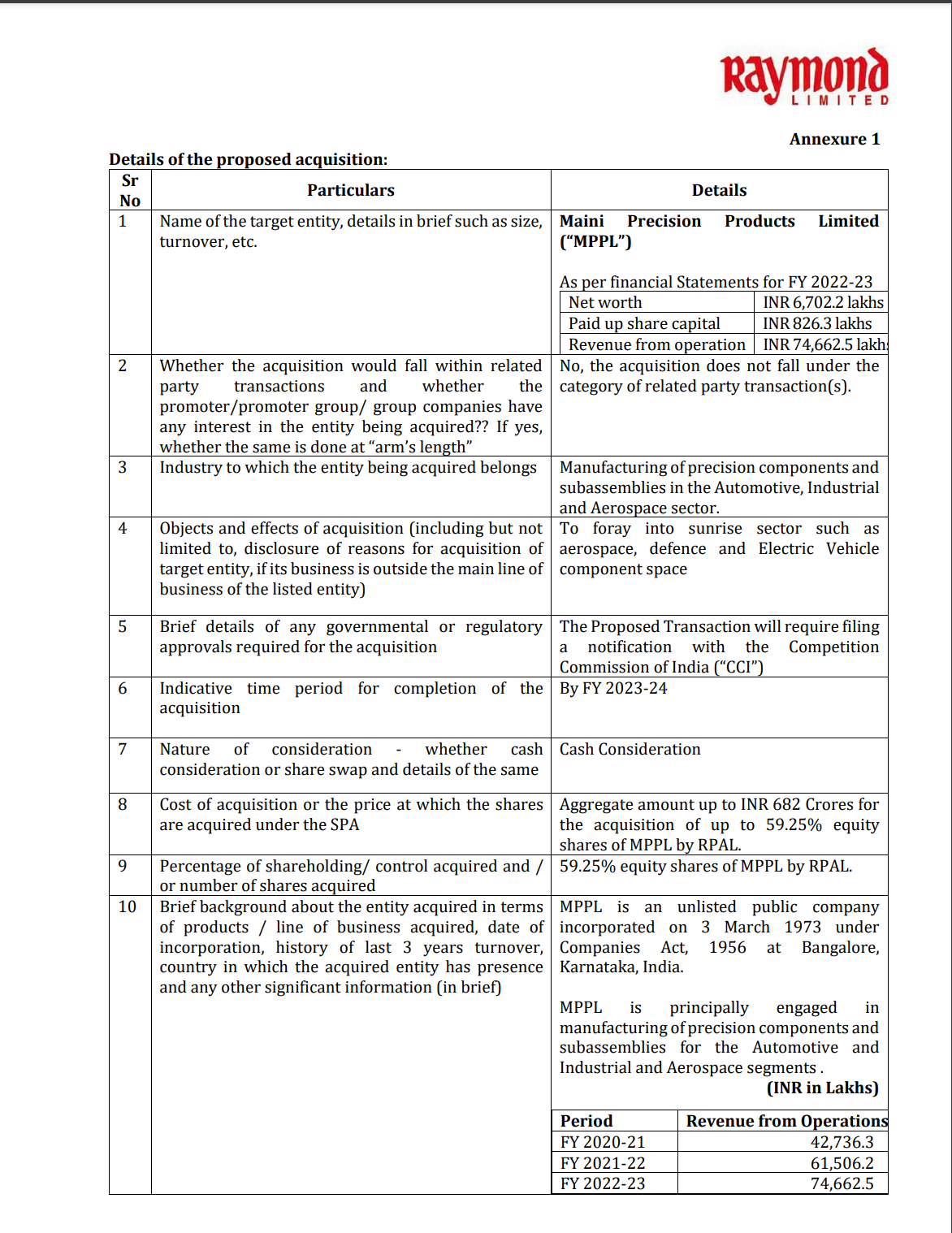

- The letter provides details about the acquisition of MPPL in Annexure-1, including information about MPPL’s financials and the reasons for the acquisition.

- Annexure-2 provides details about the Composite Scheme, including the entities involved, the division to be demerged, and the reasons for this restructuring.

In simple terms, that Raymond Limited is making some big changes in its business by acquiring another company and restructuring its engineering business.

Page industries (03-11-2023)

I tried online too, but for Innerwear boxers there is no option to select the print you want. It simply says “Assorted Prints” or “Assorted Checks”.

I believe Jockey had a system where they would automatically replenish stock as soon as something was sold. I wonder if this has changed post covid.