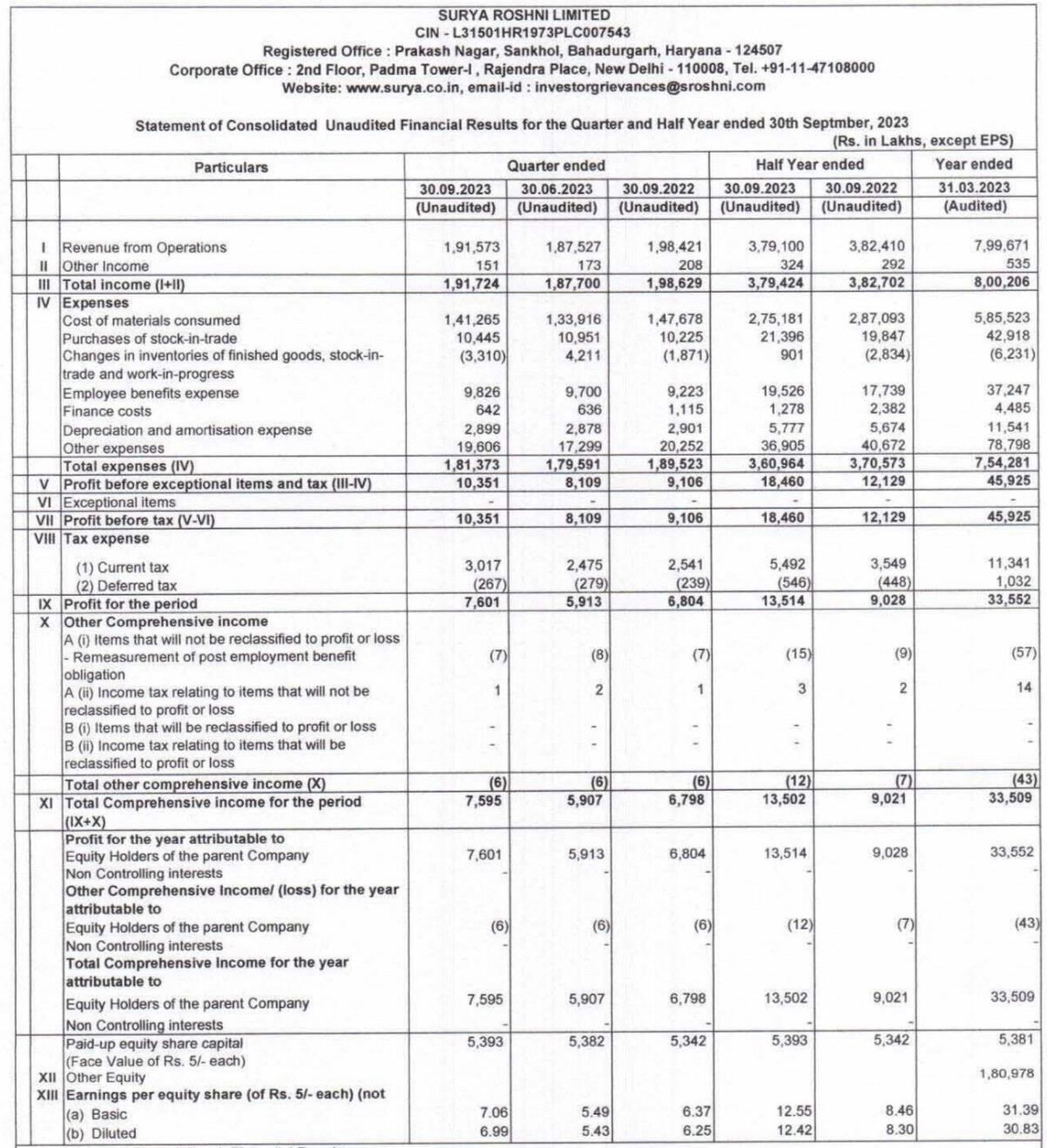

Decent set of results from Surya Roshni. Margin expansion seen

Decent set of results from Surya Roshni. Margin expansion seen

Look at the threads posted my members sharing their PF, they give their rationale for choosing their picks. If you are starting off with VP, this is the way to do.

There are many PF threads, go through them, and you will see how discussions happen and go forward.

There is recession fears in US plus Indian economy is strong and growth is still expected. Credit quality in US is about to worsen due to historically high interest rates.

Any fundamental reason for the price surge…??

Hey there, I’m sorry for the delayed response. I have to admit, you guys are absolutely right – if I had stuck with the companies in my initial post, I’d be sitting on a few real winners. It’s actually the first time I can proudly say I have a knack for picking the right stocks. I’ve mentioned before that I really need to work on my ability to hold onto my investments.

I went back and crunched the numbers, and if I had held onto the original list, my CAGR would be a fantastic 48% (which, believe me, I’d love to have). However, with all the buying and selling I’ve done, my CAGR stands at 35%. So, it’s clear that constantly tinkering with my portfolio has been detrimental.

I’ve generally been good at making the right picks, especially since out of the 12 stocks in my initial list, only 1 (Waterbase) has given me negative returns. I hope that over the last 5 years, I’ve improved my ability to hold onto my investments.

Revenue is not down, wonder why there is such a massive drop in profits. Also a lot of FIIs exited – probably why.

I will share it within short time

Its great to see GCPL declaring dividend after few years. Surely a positive sign!

If anyone has clue why dividend declared this time and any change in dividend policy, pls share.

Based on progress of these two brands, any thoughts if this was a good Capital allocation?

Also some news below which I did not understand completely. If someone has better understanding pls let us know the implications…

I think I had provided my thoughts on this earlier in some thread in one of our discussion.

Most points already covered. I will give some pointers I have in mind –

The total percentage of NetWorth which one invests in equities is important and most critical factor in defining investing style and approach. A 12% CAGR on 70% of networth is much better than a 30% CAGR on 5% of networth. Then it doesn’t matter if 12% is via stocks or mutual fund. An extra couple percentage point is good to have via either means though…whichever is better…

If the invested networth is less than 10% (just for sake of example), then neither Direct equity nor MF would cause meaningful difference unless we keep finding multibaggers.

This feeling of MF vs Direct equity is cyclical . Even other thoughts of trying various investing styles maybe cyclical… When MF do extremely well, the peak is that I wish I was more in MF and when MF go through a lag… I am so much better and let me share all XIRR comparisons…Last few months/year…BSE Midcap has done great and must have beaten many investors who invest in selected well known midcap/small largecaps…hence this thought is common to have now…Its natural…

The biggest positive of being in direct equity IMO is an upside risk if the monkey within me hits the right dart…the well researched human fails to pick up the right company at the right time and in right amounts all the time! ![]()

I’m invested in hdfc bank but now i have started to look into peers which are of same size or bigger compared to hdfc after merger.

hdfc trades at a valution of 16 pe ratio and p/b ratio of under 3 which historically is the lowest it has been for the bank but once we start comparing it the likes of citi group and bank of america which both trades at valution of 7 pe and almost 4% dividend yield which makes them significantly cheaper than hdfc bank.

Can someone please explain to me the logic of paying such a significant premium to an indian bank ,i know we are a developing nation but the bank is already to big and i doubt it will grow at the same pace it has been growing the past few decades the growth in eps is to early to tell but it has been rangebound for the past 1 year.