Good quarterly result by Dr Lal Pathlabs.

Source – https://www.bseindia.com/xml-data/corpfiling/AttachLive/b2c675f3-8b1c-4538-b0d7-ba066ab36542.pdf

Note – Invested

Good quarterly result by Dr Lal Pathlabs.

Source – https://www.bseindia.com/xml-data/corpfiling/AttachLive/b2c675f3-8b1c-4538-b0d7-ba066ab36542.pdf

Note – Invested

Compared to Father, son looks like more sort of business guy than a technical one. Do we foresee any lack in the vision atleast technically once Gursharan hands over. Did we had any interaction with other CXOs who can carry the vision on the lines of Gursharan singh, which hardly anyone talked about

Hi @Pragnesh sir, did you make any new entry at this time? Could you please share your thesis/rationale?

https://youtu.be/fXUsH3gqOdM?si=161UPG1cV_27cGEL. Ads in world has started as guided by management in last concall

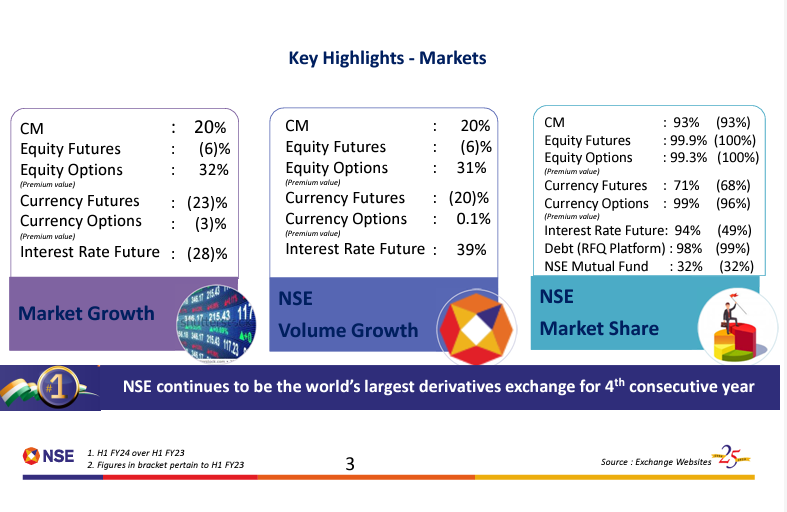

I think effect will be visible from next quarter result. Market share of BSE Vs. NSE in derivatives.

https://twitter.com/darshanvmehta1/status/1714503015473033348

Worrisome part for me is BSE is loosing in other parts – currency (After last quarter result, i wrote it here), Interest rate derivatives & even loosing market share in SME Ipo.

Also if anyone analysed NSE’s result, SGF expense has rise to 1000% due to increase in volume & volatility. For BSE also i suspect there will be increase in SGF expense due to derivatives volume.

This is a slide from Q2 & H1 FY24 results of NSE published yesterday. NSE’s market share has only marginally come down during H1FY24 from near 100% in H1 FY23. Given the rising derivative volumes at BSE, I was expecting the market share gains for BSE to be much more than what is coming out.

Any thoughts? Am I reading this right?

Results are extremely bad, don’t know what happened. Waiting for investors presentation and earnings call.

Results will be declared on 9th Nov it seems.

https://m.bseindia.com/MAnnDet.aspx?newsid=7fa0c270-a123-43cd-937f-9aa7357f8eb9&Form=STR&scrpcd=543957

Thanks for the summary. I have one question here, They upped their FY24 gross leasing guidance to 6.5 msf from 6.0 msf last quarter. This was on the back of an early renewal of 0.6 msf which essentially would have happened next FY anyway. Adjusted for this, their leasing guidance is actually down 100 k sqft compared to last quarter. Any particular reason for this?

As per our GOV guidelines the ethanol blending in fuel % will increase steadily. As more and more Sugar cos start making ethanol for this purpose, how will that effect the cyclic nature of the sugar industry?