There cannot be a standard one size fit all answer to all these companies. Its specific to each company. I can share my views about RACL . Auto ancillary companies are always dependent for their sales and price on big OEMs while.on raw material supply side they are dependent on big metal companies . So from both sides they are squizzed and hence not in a great position to expand their Profitability. So I sold it within weeks of realising this mistake. Since business model itself has no moat, I would.never care about its valuations. First business then valuations. Always.

Posts tagged Value Pickr

Arman Financial Services Ltd (01-11-2023)

great set of number by Arman again

Arman qtr 3 inv ppt brief 011123.pdf (403.8 KB)

Investing Basics – Feel free to ask the most basic questions (01-11-2023)

Hello all,

I have a query after looking at performance of companies like RACL, SBCL, AngelOne ,MapMyIndia etc.

What should be the approach for a new investor when looking at companies with good result? Because these companies are in growth phase or already grown a lot, there valuation will always be on expensive side. What option does retail investor have in such scenarios? Does one wait for the correction in these companies or simply ignore these one and look for newer options. ?

This is not from a point of FOMO but when you encounter companies with good recent past record this question can be natural.

Thanks

Natco Pharma: Focusing On Complex Products (01-11-2023)

Any familiar with USFDA inspection process can please update how serious are these observations? And what is the stipulated period to address these observations? Thanks.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (01-11-2023)

As per todays concall of Dhampur Sugar Mills, there will be some impact on cane availability due to new mill coming up near its unit. The new mill will start production from December. But the management was confident of maintaining its numbers even though there is some impact on cane availability.

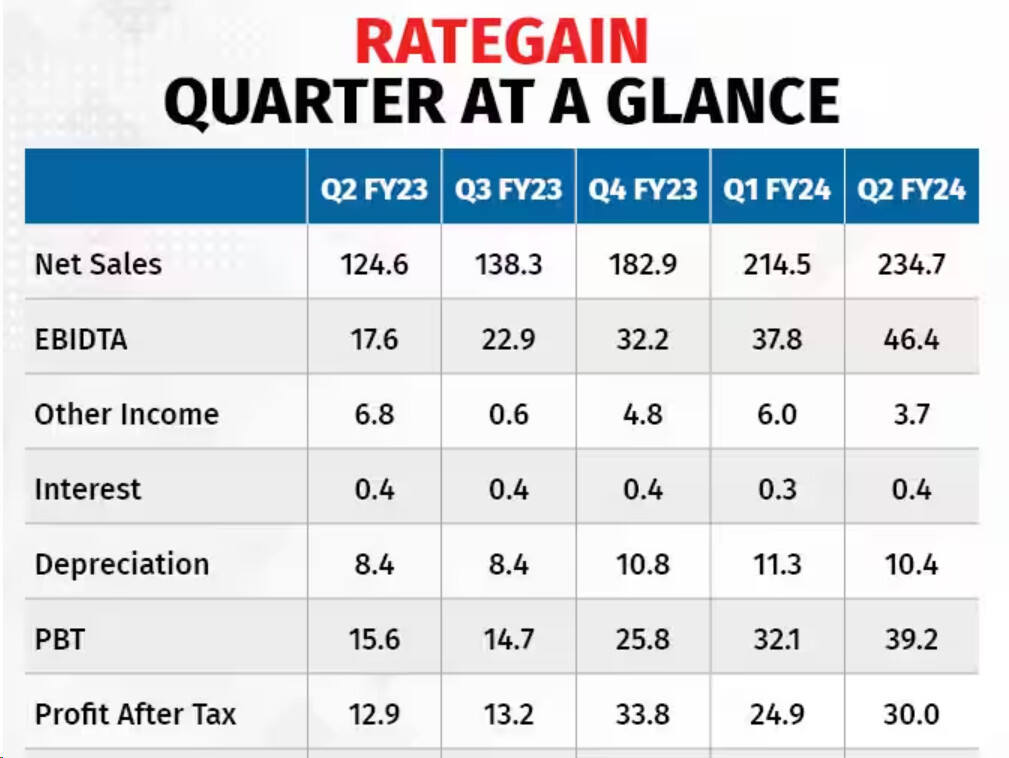

Rategain – Fast Growing SaaS Leader (01-11-2023)

Rate gain has posted a very strong set of numbers .

In the concall management guided doubling the revenue with 25% margins in 3 years. The only concern was that the bulk of the growth in this quarter came inorganically from Adara, which showed exponential growth. The management guided strong growth vis-a-vis flattish performance in Distribution vertical for H2 . They also have a strong war chest ready for future acquisition opportunities .

Overall this company seems to be on a roll .

Key risks would be impact on global travel and tourism due to present wars or some other black swan event , technology disruption etc. Stock has run up a bit , but I think it still has the potential to double from the current levels in 3years if management walks the talk.

Disc :Started Investing and looking to add on dips.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (01-11-2023)

Yes. I have attached relevant one minute volume candles of 30.10.2023 & 31.10.2023 only

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (01-11-2023)

(post deleted by author)

Steel Strips Wheels Limited – Attractive Valuations (01-11-2023)

How much will the depreciation be qtrly after they inccur the whole capex?