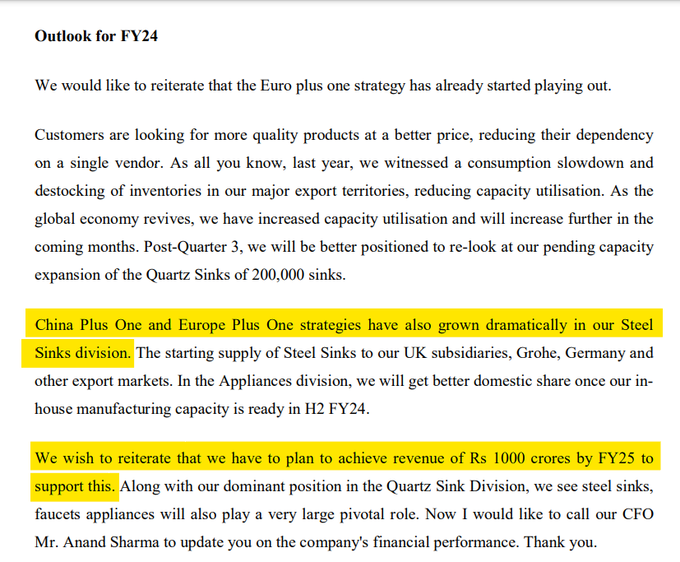

Good Outlook for FY24

-

They believe in their steel sink products.

-

They plan to achieve sales of INR 1000 cr by FY2025. Right now it is INR 594 cr which means double in 2 years

Good Outlook for FY24

They believe in their steel sink products.

They plan to achieve sales of INR 1000 cr by FY2025. Right now it is INR 594 cr which means double in 2 years

Only concern is the valuation. Markets can react sharply even if results go down slightly. Syngene bad a good result but fell sharply because management guidance changed from high teen to low teens.

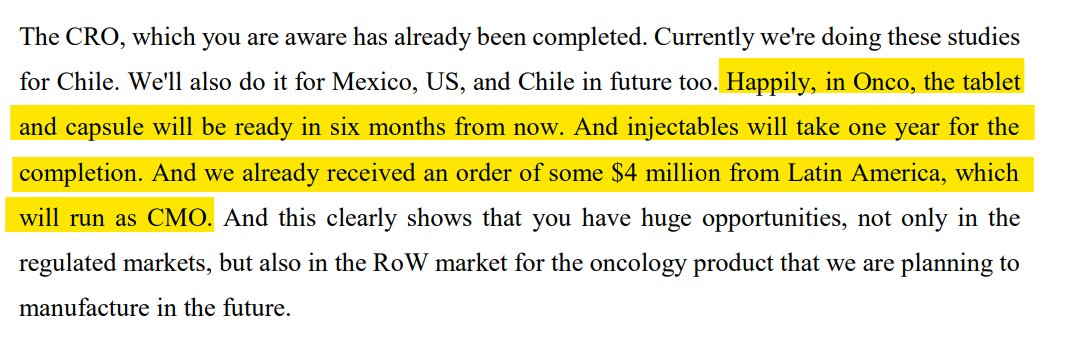

The company is working on ONCO and they have already got an advance order of $4 million.

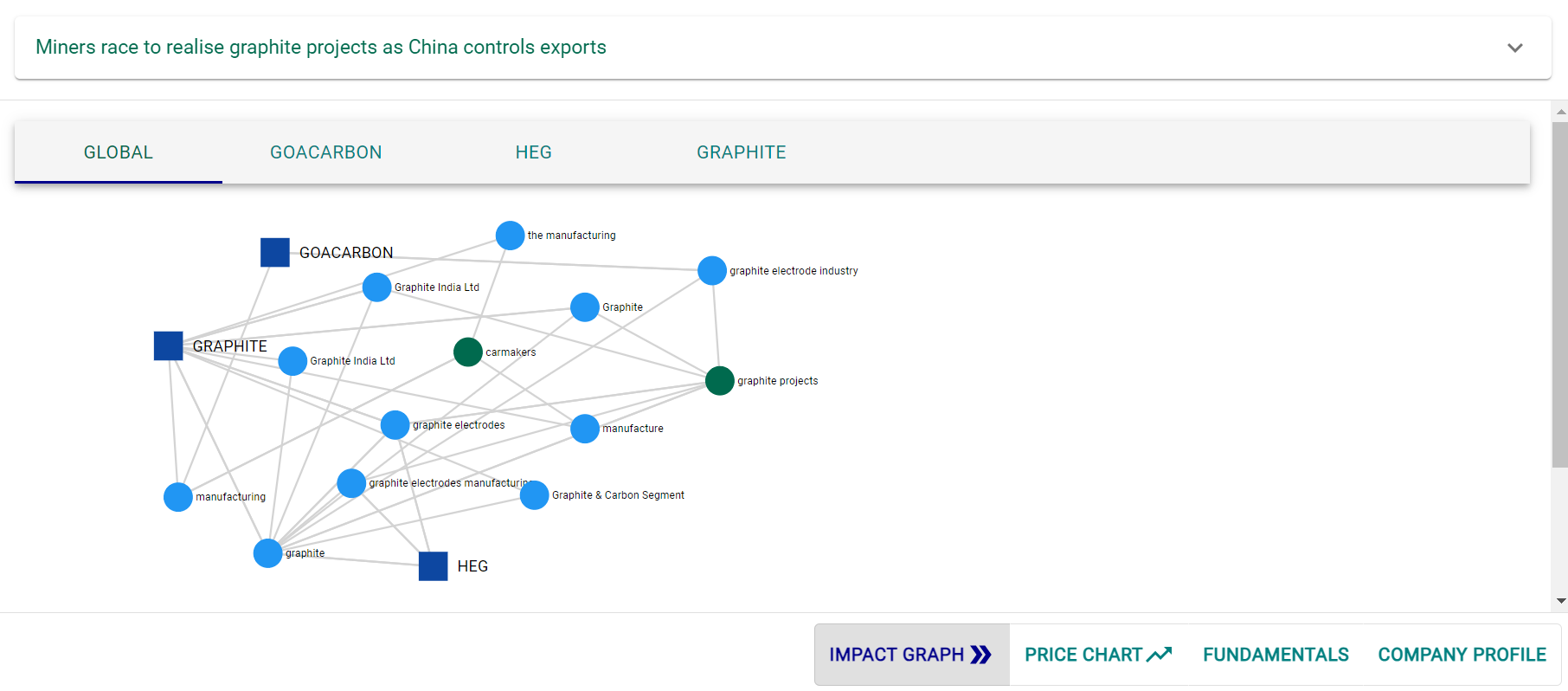

Recent developments in China’s export restrictions on key components for electric vehicle (EV) batteries have raised concerns in the global automotive industry. However, these changes can bring forth opportunities for certain Indian graphite companies.

Specifically, 3 Indian companies – Goa Carbon, HEG Limited, and Graphite India Limited are likely to be impacted as shown above. We will explore how these new export curbs can positively impact the business and stock prices of these companies.

Investment in Mining Projects: To ensure a stable supply of battery inputs, carmakers have been increasingly investing directly in mining projects. This trend benefits Indian graphite companies by offering potential partnerships and collaboration opportunities with these global automotive giants. Such partnerships can lead to substantial revenue and profit growth for these Indian companies, which would, in turn, drive their stock prices higher.

Reduced Competition and Increased Demand: As China tightens export controls on natural graphite products used in EV battery manufacturing, the primary source and producer of these components, the global supply chain may experience disruptions. This situation creates an excellent opportunity for Indian graphite companies to step in and meet the rising demand. Companies like Goa Carbon, HEG Limited, and Graphite India Limited, which are already established players in the graphite industry, can benefit from reduced competition in the global market.

Enhanced Relevance in the EV Ecosystem: With China’s export restrictions potentially affecting EV manufacturers worldwide, the need for a diversified supply chain becomes crucial. Indian graphite companies can position themselves as reliable alternatives for global EV battery manufacturers. As a result, these Indian companies can gain greater relevance in the EV ecosystem, leading to increased business opportunities and partnerships.

Strengthening of Domestic and International Presence: The increased demand for graphite components, including electrodes and carbon products, provides a chance for these Indian companies to strengthen their domestic and international presence. By expanding their production capabilities and focusing on quality and innovation, they can attract both domestic and international clients, further boosting their business prospects.

Conclusions:

While China’s export restrictions on key EV battery components may present challenges to the global automotive industry, they also open doors of opportunity for Indian graphite companies. Goa Carbon, HEG Limited, and Graphite India Limited stand to benefit from reduced competition, increased demand, and potential collaborations with international car manufacturers. These developments are likely to have a positive impact on the businesses and stock prices of these Indian companies, making them attractive options for investors looking to capitalize on the evolving dynamics of the EV battery industry.

References:

China imposes fresh export curbs on key EV battery component

Miners race to realise graphite projects as China controls exports

Disclaimer: The article is not a recommendation or advice as to whether any investment is suitable for a particular investor.

UPL Guidance going down continuously from past 2 quarters.

Revenue growth guidance dipped in Q12024 to 1-5% from 6%-10% and further to flat now

EBIDTA growth guidance 8-12% to 3-7% to 0-(5)% now!!

With high debt and slowing Sales the share price ought to do what its doing currently, down 30% in 6 months. Can one do bottom fishing here, or better to wait out for a turnaround in H2 2024??

Valuation wise on P/B its trading at all time lows of 1.3

Just adding to the notes

-They mentioned willingness to grow in other location for diversifying their revenues (no dependence on one plant)l & current land is enough for next 3-4 years of growth).

-Competitors mentioned include:- Sundram Fasteners, Hitech Gears, Sona Blw.

-Really respect the work both Sona Blw and Sansera are doing in the industry. When I asked them which competitors do they respect.

-Plan to do 60 crore capex per annum going forward (what they stated in the concall).

-Some of the employees were there in the company since 1990s.

-The plant built for ZF housed 7 products which exclusively RACL is doing. 100% supplies. The difference between Japanese and German work culture is:- that Japanese will come to the plant and sit together to rectify mistakes. In one of the past instances a batch of products was rejected due to finger print and also have been rejected due to wrong boxes!

German customers- straight away reject and deduct the amount.

-Observation from visiting other set ups:- plant & machines were noiseless and machinery was mainly from Europe and China.

-Trying to get into differential gears. Lost out on one contract to a large domestic competitor.

-Plans to get into industrial gears. Already supplying:- stated one example how entire Paris can go through a black out as their gears are used in electric circuit of the customer they have supplied to.

-Biggest challenge they face is that of manpower. Training the employees and making them understand the Quality culture is a challenge. Japanese monitor the plant using some software (don’t remember the exact name). They keep checking Quality of each and every product. As all products have a QR code on them.

Promoters strategy was extremely clear when Gursharan sir said this:-

We are a company that is purely focused on niche segments. This is what gives us the gross profit margins. We are not and never will be a mass market company.

Disclaimer:- strictly not a recommendation to buy or sell. Just sharing what I learned on top of notes shared by @First_Principles

Goes without saying the benefits of battery. That way nothing can compete with petrol diesel IC engine vehicles in terms of driveability , power , pick up & Serviceability and no imports except the fuel.

The main issue with batteries are three :

(1) Supply chain and availability of rare earth elements like lithium available only in few nations only. So we are 100% import dependent.

Look at what happened to semiconductor issue during last 2 years. The entire auto industry collapsed.

(2) Lithium batteries stack occupy a lot of space and Requires Recharging and recharging currently done through Thermal power. world over , 90% power is through thermal coal currently.

(3) life cycle Study shows that battery has more carbon emissions than even conventional.

The report is Cradle-to-Grave LCA which takes care of the entire life cycle of extraction, refining , manufacturing, maintenance and recycling for a fixed life of 2,00,000 kms.

Please can someone elaborate on what basis should we plan our exit in this stock, how to keep a track of it and plan your exit as it is cyclical.

Thank you.

Thanks for your thoughts on your portfolio.

Do you feel that XPRO India is expensive at current valuations of 50PE around

Had an insightful meeting in Delhi with Career Launcher management last week.