Join us as we Commemorate the Listing Ceremony of Max Estates Limited

Date: Monday, 30th October 2023 | Time: 9:00am onwards

Venue: NSE Atrium, BKC, Mumbai

Join us as we Commemorate the Listing Ceremony of Max Estates Limited

Date: Monday, 30th October 2023 | Time: 9:00am onwards

Venue: NSE Atrium, BKC, Mumbai

Q2 FY24 Results Review

Decent results

Total Revenue at Rs. 2,43.4 Cr grew by 17.5% YoY

EBITDA at Rs. 58.1 Cr grew by 37.1% YoY

EBITDA Margin at 23.9% in Q2 FY24

Consolidated Performance Highlights:

Consolidated Revenues of Rs. 2,434 million, growth of 17.5% y-o-y and 1.4% q-o-q

Consolidated EBITDA of Rs. 581 million, growth of 37.1% y-o-y and 21.9% q-o-q

Consolidated EBITDA margin at 23.9% v/s 20.5% in Q2 FY23 and 19.9% in Q1 FY24

Consolidated PBT of Rs. 426 million, growth of 48.6% y-o-y and 29.3% q-o-q

Consolidated Basic EPS of Rs. 2.57 during the quarter, growth of 32% q-o-q

Standalone Performance Highlights:

Standalone Revenues of Rs 2,230 million, growth of 22.0% y-o-y and 3.1% q-o-q

Standalone EBITDA of Rs. 575 million, growth of 31.6% y-o-y and 15.6% q-o-q

Standalone EBITDA margin of 25.8% in Q2 FY24 v/s 24% in Q2 FY23 and 23% in Q1 FY24

Standalone PBT of Rs. 473 million, growth of 41.1% y-o-y and 18.3% q-o-q

Standalone ROCE (annualized) at 23% v/s 16% in FY23

Hospital Operational Highlights:

In patient count (incl. Day Care) of 22.652, growth of 21.6% y-o-y

Total Surgery count of 7,771, growth of 14.2% y-o-y

Occupancy rate at 54% in Q2 FY24 v/s 49% in Q2 FY23

ARPOB during the quarter was 36,136, growth of 8.1% y-o-y

Press release Q2 FY 24 (https://www.bseindia.com/xml-data/corpfiling/AttachLive/49a6e7e9-3b9b-4cf5-ba05-e36c7790f5d4.pdf)

Q2 FY24 Results Review

Decent results

Total Revenue at Rs. 2,43.4 Cr grew by 17.5% YoY

EBITDA at Rs. 58.1 Cr grew by 37.1% YoY

EBITDA Margin at 23.9% in Q2 FY24

Consolidated Performance Highlights:

Consolidated Revenues of Rs. 2,434 million, growth of 17.5% y-o-y and 1.4% q-o-q

Consolidated EBITDA of Rs. 581 million, growth of 37.1% y-o-y and 21.9% q-o-q

Consolidated EBITDA margin at 23.9% v/s 20.5% in Q2 FY23 and 19.9% in Q1 FY24

Consolidated PBT of Rs. 426 million, growth of 48.6% y-o-y and 29.3% q-o-q

Consolidated Basic EPS of Rs. 2.57 during the quarter, growth of 32% q-o-q

Standalone Performance Highlights:

Standalone Revenues of Rs 2,230 million, growth of 22.0% y-o-y and 3.1% q-o-q

Standalone EBITDA of Rs. 575 million, growth of 31.6% y-o-y and 15.6% q-o-q

Standalone EBITDA margin of 25.8% in Q2 FY24 v/s 24% in Q2 FY23 and 23% in Q1 FY24

Standalone PBT of Rs. 473 million, growth of 41.1% y-o-y and 18.3% q-o-q

Standalone ROCE (annualized) at 23% v/s 16% in FY23

Hospital Operational Highlights:

In patient count (incl. Day Care) of 22.652, growth of 21.6% y-o-y

Total Surgery count of 7,771, growth of 14.2% y-o-y

Occupancy rate at 54% in Q2 FY24 v/s 49% in Q2 FY23

ARPOB during the quarter was 36,136, growth of 8.1% y-o-y

Press release Q2 FY 24 (https://www.bseindia.com/xml-data/corpfiling/AttachLive/49a6e7e9-3b9b-4cf5-ba05-e36c7790f5d4.pdf)

Wow, This company has a long history.

Thanks to VP for this detailed info on this company.

Wow, This company has a long history.

Thanks to VP for this detailed info on this company.

The reviews are mostly related to products and people blamed it on logistic company i.e. shiprocket (big foot) which I have seen being used mostly by Instagram/FB/WhatsApp sellers.

The reviews are mostly related to products and people blamed it on logistic company i.e. shiprocket (big foot) which I have seen being used mostly by Instagram/FB/WhatsApp sellers.

Thanks Naveen for your inputs…I agree the margins are higher and hence the valuation relative to Ambika. But if you compare the differential valuation of the two, you would notice that while Ambika has remained around P/B of 1.1- 1.4 over last 10 years while for KPR it has jumped from less than 3 to around 7.5 now.

As pointed by you, what has changed for KPR from pre-pandemic to now is their foray into sugarmills, ethanol and specially the FASOs branded innerwear. Seems to me the market is liking the branded D2C business and in the short run the sugarmills and ethanol are also helping only currently…

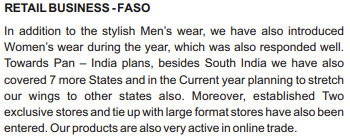

Below from their annual report:

However in the notes, i see the security deposit from dealers has reduced from 3L to 1L.

Does it show reducing demand? Or atleast less favorable terms… But certainly not expansion…

Considering all this, and the current market mood was just trying to seek if there is more which warrants the increased valuation market is willing to give to KPR currently…

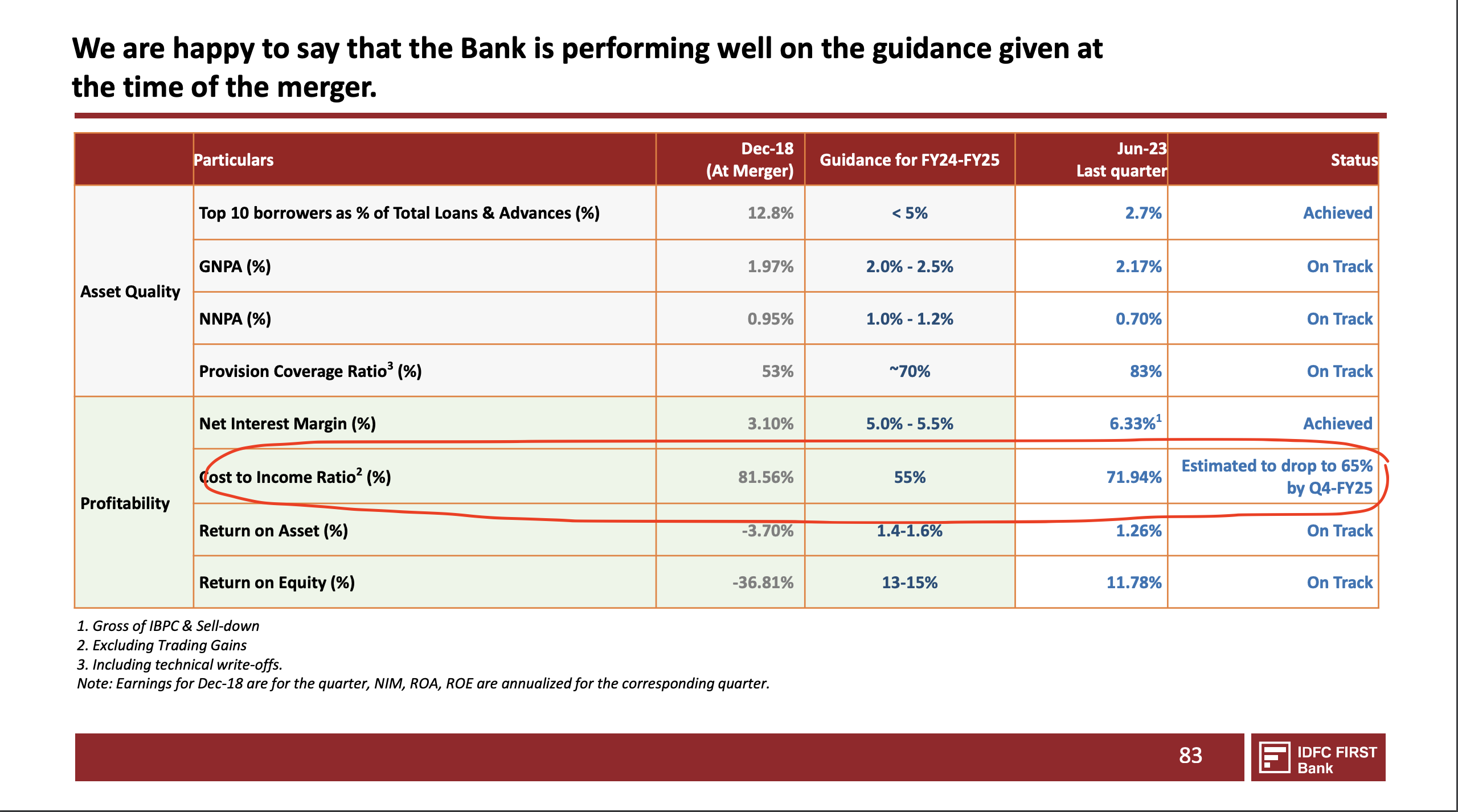

Please see the last quarter presentation where they have revised the guidance – attached screenshot

Is there any website for backtesting our strategies?