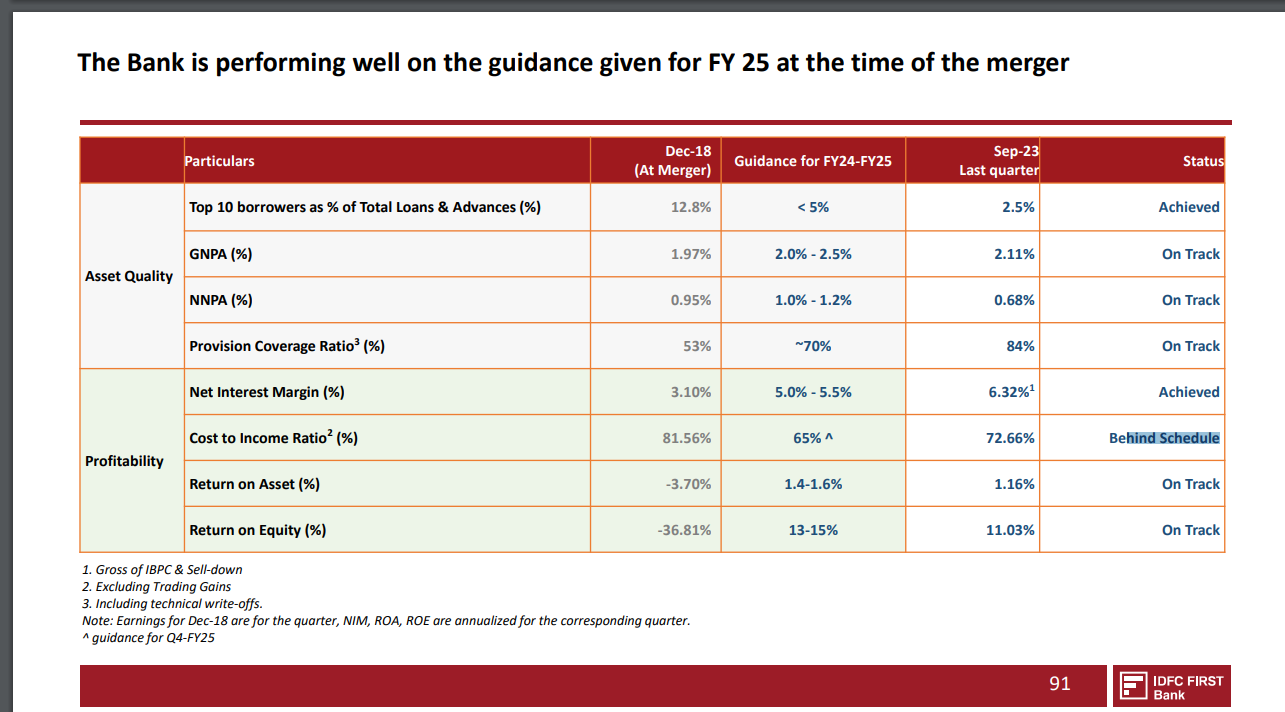

I don’t believe it is a case of miscommunication. In the Q1 FY 2023-2034 investor presentation, they updated the guidance, indicating an estimated decrease to 65% by Q4-FY25.

Q1

Q2:

I don’t believe it is a case of miscommunication. In the Q1 FY 2023-2034 investor presentation, they updated the guidance, indicating an estimated decrease to 65% by Q4-FY25.

Q1

Q2:

(post deleted by author)

Ambika is pure play spinning where KPR is integrated with apparel exports. Garmenting has better margins than spinning.

Their foray into sugar mills and ethanol is what could turn out to be dicey in the future.

Hi,

In the screenshot you shared… they have clearly mentioned that ratio is “Estimated to drop to 65% q4 FY25”.

Not sure why they use the word ‘drop’ though. it is increasing.

Edit: Also, in the last earnings call VV said this’

“So these small movements of 10 basis points, 20 basis points

here or there are not really disturbing us whether in cost of funds or any of these line items”. I am unable to find an questions on the estimated move to 65%. 10% is not small. Right?

Yup, valid reason. If the management keeps up with it’s promise of zero pledged shares soon, we might see an inflow of institutional investors then

Excellent interview, thanks for sharing. Just an update with regards to their holding in Droneacharya

NAV’s Sept Qtr holding has come down from 2.18 to 1.14 → Droneacharya Aerial Innovations Ltd financial results and price chart – Screener and they now have fresh investments in DroneDestination – 2.74% → Register – Screener

Kindly note: my first post here, so if I’ve missed something etc, kindly excuse!

Senco Gold Q2 updates –

Sales up 28 pc !!!

In Q1, sales growth was 30 pc

Same store growth was 19 pc in Q1. Was lesser ( exact figures not mentioned ) in Q2

Same store growth in first 6 months @ 19 pc – commendable

Q2 volume growth –

Gold volumes up 11 pc

Diamond volumes up 33 pc ![]()

Opened 2 new stores in Q2

Stud ratio ( Diamond : Gold jewellery sale ratio ) – up sharply in Q2 @ 13.7 pc vs 11.2 pc last year ![]()

All this despite festive season being firmly pushed to Q3 this FY

Is it the Next Titan ???

Who knows

Atleast, I hope so !!!

Disc – invested, biased

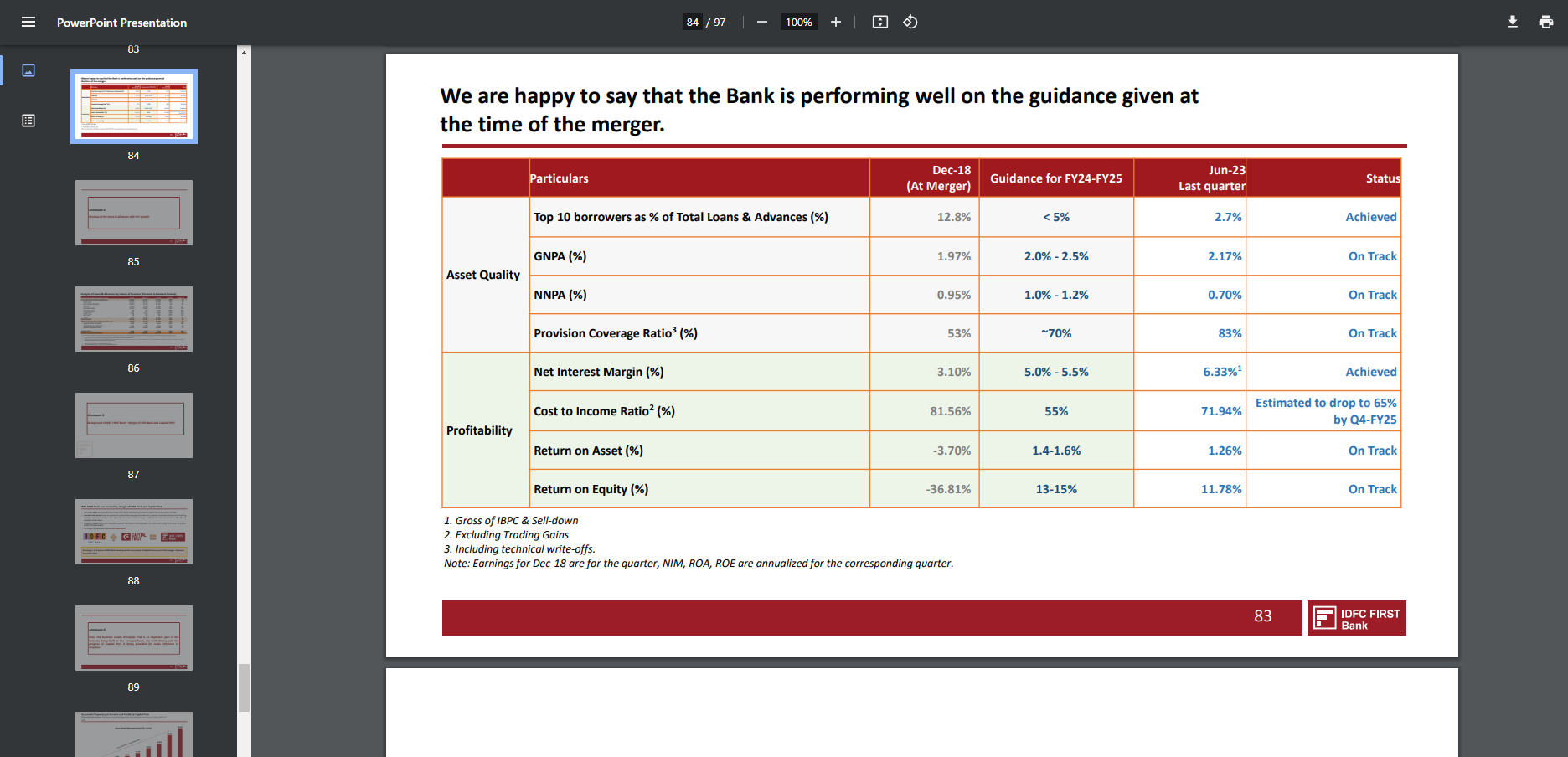

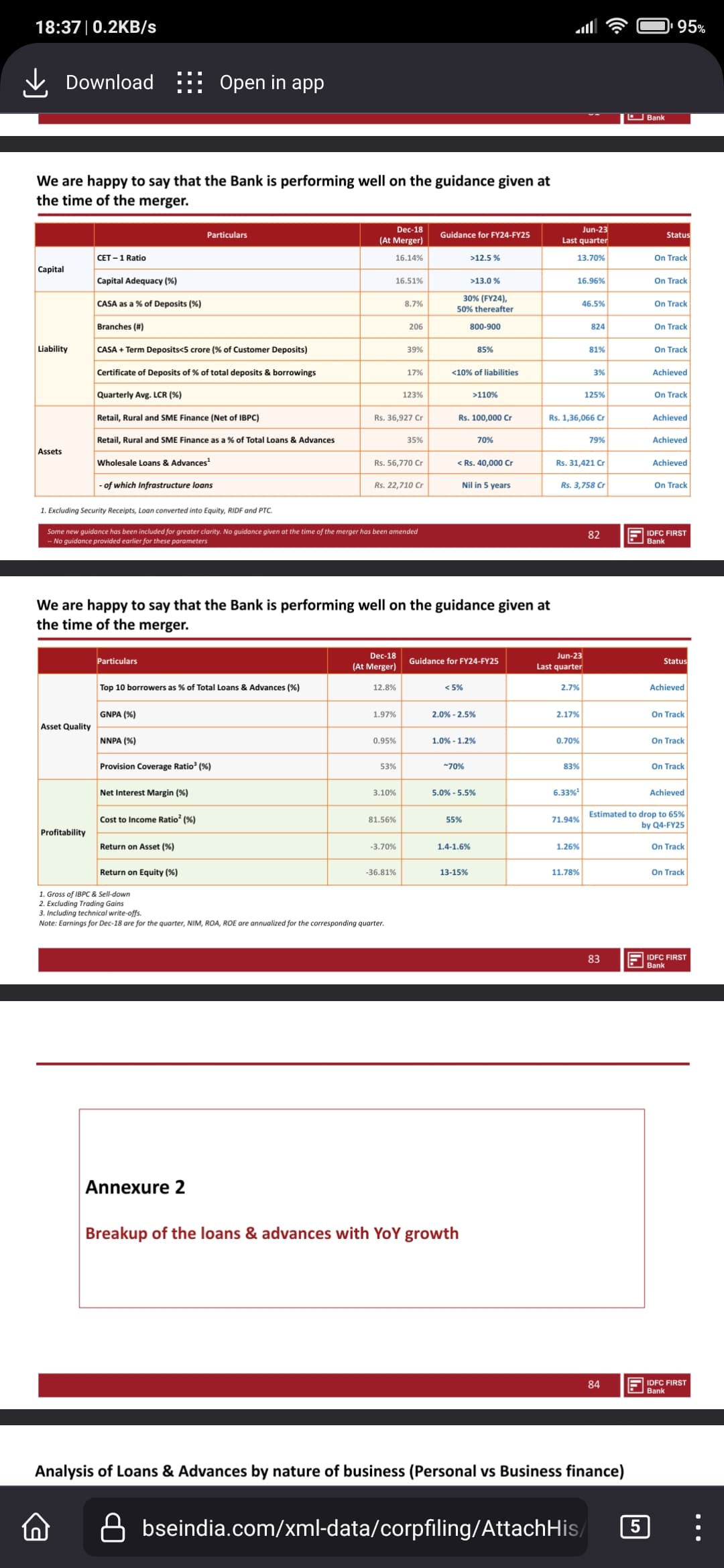

I generally extend benefit of doubt to companies for misrepresentation of data or inaccurate reporting. But I don’t do it for banks and specially for IDFC First whose brand is built on transparency.

They quietly changed the target for cost to income ratio in the investor presentation from 55% to 65%. Now, they are allowed to change the guidance however the slide still says we are performing well on the guidance given at the time of the merger. Saying this, they shouldn’t change the guidance. 65% was not the guidance AT THE TIME OF THE MERGER.

It’s this kind of inaccuracies that start to question the intention behind miscommunications. Attaching the screenshot for comparison.

Although the numbers are good but stock price appears overvalued to me at the moment. 550-650 will be a good range I think to go in big. It may take few years of earning growth & new innovative products to justify the previous all the time high of 1500 price. Let’s see.

Started accumulating slowly between 700-820 levels after I found out that it contract manufactures ENZO liquid detergent for reliance at a very affordable price ![]() compared to SURF and ARIEL. (Buy Enzo Intelomatic Front Load Liquid Detergent 2 L Online at Best Prices in India – JioMart.)

compared to SURF and ARIEL. (Buy Enzo Intelomatic Front Load Liquid Detergent 2 L Online at Best Prices in India – JioMart.)

ECO Recycling Limited – Concall – 27th October 2023

Just want to add few points in from the Concall.

The total market share is around 4 MMT and out of this 50% is in formal sector. Currently industry CAGR is 27% and ECORECO is expected to have better growth then the industry average.

Current capacity is 7200 MTA and new capacity addition of 18K MTA is going to be live by the end of FY 24. The total capex for this additional capacity is Rs 45 Cr and company has already spend Rs 30 Cr and the additional 15 Cr will be spent in the current FY24.

Capacity utilization: Current the company is using 30% of its total installed capacity (7200 MT) and has generated revenue of Rs 7.10 Cr in the September quarter of 2023. With the wining 5 more new clients/producers the company is expecting its current utilisation to go upto 60-70% in the coming quarters. So, the total installed capacity after the above capex is going to be 25K MT at the end of FY24 and with the expected utilisation of 60% in FY 25 the expected revenue can be around 80 Cr and Rs 100 Cr above for the next FY. So there is a good visibility in the revenue and company has ensured that its going to maintain its current margin of 30% (operating margin).

For the battery recycling current capacity is 3K MT.