Does anyone have any update on this company?, The mgmt is very shy to talk to investors.

Posts tagged Value Pickr

MCX and Financial Technologies (28-10-2023)

You are correct, the volumes have not reached the levels seen right before the platform switch. But i can see the Daily turnover increasing everyday as the confidence grows.

Maruti Suzuki – Leader in Passenger Vehicles (28-10-2023)

There is no study to indicate whether people are upgrading to SUV or not. Only thing clear is that small car’s sales are decreasing and SUVs are increasing. So, the company’s focus must be on new SUV launches.

If you look at the presentation highlighting the new launches eVX and New Swift looks promising. But, eWX, mini wagon EV looks ugly.

So, looks like company’s is trying to woo new small car customers. Then there are other products which may open new segments.

SUV launches are over and that’s concerning.

Yes, it looks like spending in lower segments is going down. Inflation is outstripping the salary growth. I agree, we should be looking cautiously at other companies catering to this segment.

Dreamfolks services limited( DFS) (28-10-2023)

Here is my understanding of the business.

Let me begin with the stakeholders involved and then the business model.

Consumer: People who avail of lounge services by paying through a credit card (or sometimes debit cards).

Lounge operator: Simply put, the company that owns/runs lounges at the airport. They provide services including food and beverage, place to rest and entertainment to customers. The cost is ~Rs 700 for using a domestic lounge.

Card providers: Usually the banks (HDFC, SBI, etc.) offer credit card services to consumers. Few credit cards have perks which include a certain number of free access to the lounge, access to the golf course, etc.

Dreamfolks Services (DFS): In my opinion, this is a software company that claims to have a proprietary platform of lounge access management.

DFS’s Business model:

- The consumer wants to enter the lounge. She swipes her credit card.

- DFS platforms check eligibility to enter. The eligibility check is based on multiple criteria including:

a. If the card falls under the free lounge access program

b. If the consumer has any remaining lounge visits from the quota - DFS pays the lounge operator Rs 700 and allows the consumer to avail its service

- DFS adds a markup of about 12.4% (which was ~15% earlier) and charges the bank ~Rs 786

- Bank pays DFS in around 100 days (which explains high receivable days)

Key considerations

-

Is there “moat”?:

I am inclined to say no.

Is it possible for banks to cut DFS out of the chain and build their own platform? I think certainly possible, but it may not be economical for the banks. If HDFC builds the lounge access platform, it will save 12% on Rs 700, which is Rs 84 per consumer per lounge access. It will not be material for HDFC given its huge size. The same is true for ICICI, SBI, Axis, etc.

Can a smaller bank or a technology player come in to disrupt?

I think certainly possible, we will have to wait and watch.

Can banks and lounge operators squeeze the margins?

Yes, they can and the lounge operators did it last quarter. -

Revenue growth:

Banks want more number of users to use credit cards. Hence to entice customers, they offered free lounge access by bearing the cost. Hence, revenue growth is a function of the number of people with eligible credit cards AND the frequency of air travel. Also increasing the number of airports and increasing the size of existing lounges will help. If revenue growth slows or stops due to any reason, valuation may get rerated.

Summary

I think the business is the result of a very smart founder who has extensive experience working at lounge management firms. The founder saw a gap where the banks were not interested in dealing with multiple lounge operators and their technology interface. Banks simply wanted to focus on, well, banking. The lounge operators wanted to focus on F&B, and hospitality rather than creating a technology platform that will interact with multiple banks’ APIs.

We must celebrate that the founder is a lady who made it big in the world of business. Kudos to Ms. Kallat. But I am currently not sure if this can be a long-term bet. I am watching the margins carefully.

I could be completely wrong, please do your own diligence.

Hope it helps!

Mahesh

Why not leave it to the experts? (28-10-2023)

Its not blindly following. I do my own study. But again, since they have already put in lots of efforts, very little is left for me to contribute, as far as study is concerned. Also there are other factors that I check. And these companies are not in the form of tips…They are good investment ideas to start with and backed up by solid research. Now how can you ignore this?

Varanium Cloud SME, the next Brightcomm Group? (28-10-2023)

I am not an investor, and I don’t know if this adds to the perspective or not, but still giving this link, as it reminds me of this thread.

Kabra Extrusion Technik (28-10-2023)

I think Kabra Extrusion is a pure momentum play and with the subsidies removed from EV 2 wheelers, the industry growth has come down to 20%. The huge tail winds are gone and hence the stock no longer justifies the 40 PE valuation.

Dreamfolks services limited( DFS) (28-10-2023)

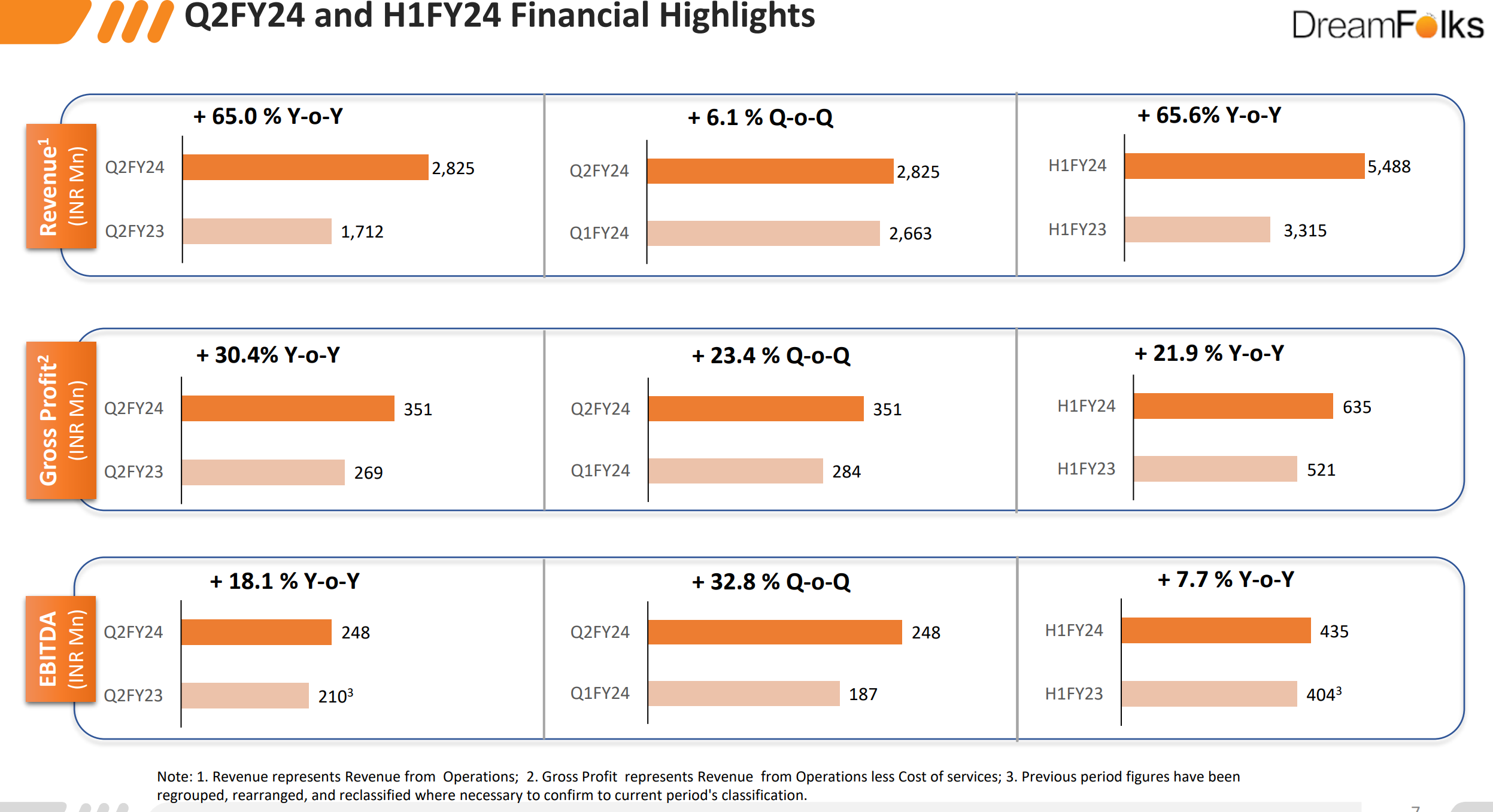

Sharing snapshot from company’s investor presentation.

Gross margin in Q2 FY24 = 351/2825 = 12.4%

Gross margin in Q2 FY23 = 269/1712= 15.7%

They don’t include other income while calculating Gross Margin. Maybe that’s why the diff in your calculations.

Hope it helps.

PPFAS Financial Opportunities Forum (28-10-2023)

Now Kotak Fellas too making a case to move to large caps

They say

Correction in small-mid caps is still not complete, correction in their prices is relatively small compared to the rally.

https://www.msn.com/en-in/money/markets/correction-in-mid-and-small-cap-stocks-not-yet-complete-says-kotak-institutional-equities/ar-AA1iVoOh

![]()

Why not leave it to the experts? (28-10-2023)

-

Ok So let me be the contrarian here. What if you are individual who has to work 70 hours a week ala Mr Murthy

. What do you do here. I know since i have been in that zone. (Never worked in IT). So again, depends on individual basis. What happens if you are bad at accounting / zero knowledge of financials.

. What do you do here. I know since i have been in that zone. (Never worked in IT). So again, depends on individual basis. What happens if you are bad at accounting / zero knowledge of financials. -

But I agree with you on not telling people to follow so called experts who are mostly selling hopium while filling their Tijoris. 99% of You Tube experts are charlatans or fake experts at best and are should be completely avoided. 1% may be usefull for closing out your own thesis or starting research on new companies. (The way most people ideally use ValuePickr). I also agree with you on MF/PMS strategy sellers.

-

Completely agree on this point.

Would love your input/criticism on my thought process.