If you have any views, post them here.

Posts tagged Value Pickr

ICICI BANK -Stock Opportunities (27-10-2023)

If you have any views, post them here.

ICICI BANK -Stock Opportunities (27-10-2023)

Oct 2023 – ICICI Bank clocked operating profit of 14K Cr in the Q2 results and Net Profit of 10.2K Cr. The bank has a NIM of 4.65 which is very healthy. Market cap of ICICI Bank is 653K crores . The surge in profits is due to its increase in deposits which grew 32% on YOY Basis and 19% from previous quarter

( CASA reduced due to this factor ), Unsecured loans increased and becomes 13.3% of the loan portfolio. Increase in unsecured loans is usually a cause of worry which has increased 37% on YOY basis however the bank on the other side has very low slippages (provisions decreased 65% YOY Q1FY24 ) which is a great number to ponder . ICICI has provisions of 1.2% of loan book at 13.K crore which is a great number . The Bank has not expanded its brannches compared to its peer and envisages increase in operational costs . NIMS are expected to slide further . Neverthless the bank is definitely on strong earnings trajectory despite these headwinds . The stock corrected by 100 points from 1000 levels which paves way to enter . India is on strong growth path and the festive demands and increasing loan books makes strong case for holding the stock for long .

When we look at valuations we need to make appropriation for the value of subsidaries ICICI pru life, Lombard , ICICI Securities , ICICI pru AMC , overseas operations …etc + stand alone Value which will drive the valuation much higher beyond 1200. Most of the brokerages have valued ICICI at a Consensus average > 1180 levels which are already published and part of public domain . These factors point out to accumalation of ICICI Bank in a staggered way to accomadate any slip in prices in global market turbulence and wait patiently for the long haul .

ICICI BANK -Stock Opportunities (27-10-2023)

Oct 2023 – ICICI Bank clocked operating profit of 14K Cr in the Q2 results and Net Profit of 10.2K Cr. The bank has a NIM of 4.65 which is very healthy. Market cap of ICICI Bank is 653K crores . The surge in profits is due to its increase in deposits which grew 32% on YOY Basis and 19% from previous quarter

( CASA reduced due to this factor ), Unsecured loans increased and becomes 13.3% of the loan portfolio. Increase in unsecured loans is usually a cause of worry which has increased 37% on YOY basis however the bank on the other side has very low slippages (provisions decreased 65% YOY Q1FY24 ) which is a great number to ponder . ICICI has provisions of 1.2% of loan book at 13.K crore which is a great number . The Bank has not expanded its brannches compared to its peer and envisages increase in operational costs . NIMS are expected to slide further . Neverthless the bank is definitely on strong earnings trajectory despite these headwinds . The stock corrected by 100 points from 1000 levels which paves way to enter . India is on strong growth path and the festive demands and increasing loan books makes strong case for holding the stock for long .

When we look at valuations we need to make appropriation for the value of subsidaries ICICI pru life, Lombard , ICICI Securities , ICICI pru AMC , overseas operations …etc + stand alone Value which will drive the valuation much higher beyond 1200. Most of the brokerages have valued ICICI at a Consensus average > 1180 levels which are already published and part of public domain . These factors point out to accumalation of ICICI Bank in a staggered way to accomadate any slip in prices in global market turbulence and wait patiently for the long haul .

AGI Greenpac- on the cusp of growth? (27-10-2023)

Key Points from Q2 Concall Summary

- Acquisition of HNG is going to be debt funded; Later on focus will be debt rationalization; In two years from acquisition the debt levels are targeted to be normalized to Rs.2,000 – 2,200 Cr.

- With HNG capacity getting added, 2-3 year down the line, company will be able to achieve revenue of 5,500 Cr. per year. Current market cap is ~ 5,600 Cr.

- Confident to maintain the margins between 20-22% for AGI business. The fluctuations in raw material prices are adjusted in contract with the customers will help to keep the margins. For HNG capacity, there is a likelihood of having the margins lower than that for AGI. Later the optimization and efficiencies will be required to be driven

- There are several cases at High Court, Supreme Court and NCLT level against the resolution plan of HNG acquisition by AGI

- 15-18% revenue growth is guided by the management

- They are optimistic about the benefits of premiumization in alcohol businesses due to demographic and economic evolution of the country

- The current capacities can support the business of about Rs2,500 Cr per year.

AGI Greenpac- on the cusp of growth? (27-10-2023)

Key Points from Q2 Concall Summary

- Acquisition of HNG is going to be debt funded; Later on focus will be debt rationalization; In two years from acquisition the debt levels are targeted to be normalized to Rs.2,000 – 2,200 Cr.

- With HNG capacity getting added, 2-3 year down the line, company will be able to achieve revenue of 5,500 Cr. per year. Current market cap is ~ 5,600 Cr.

- Confident to maintain the margins between 20-22% for AGI business. The fluctuations in raw material prices are adjusted in contract with the customers will help to keep the margins. For HNG capacity, there is a likelihood of having the margins lower than that for AGI. Later the optimization and efficiencies will be required to be driven

- There are several cases at High Court, Supreme Court and NCLT level against the resolution plan of HNG acquisition by AGI

- 15-18% revenue growth is guided by the management

- They are optimistic about the benefits of premiumization in alcohol businesses due to demographic and economic evolution of the country

- The current capacities can support the business of about Rs2,500 Cr per year.

Varanium Cloud SME, the next Brightcomm Group? (27-10-2023)

They are doing Capex (International Scam)

Varanium Cloud SME, the next Brightcomm Group? (27-10-2023)

They are doing Capex (International Scam)

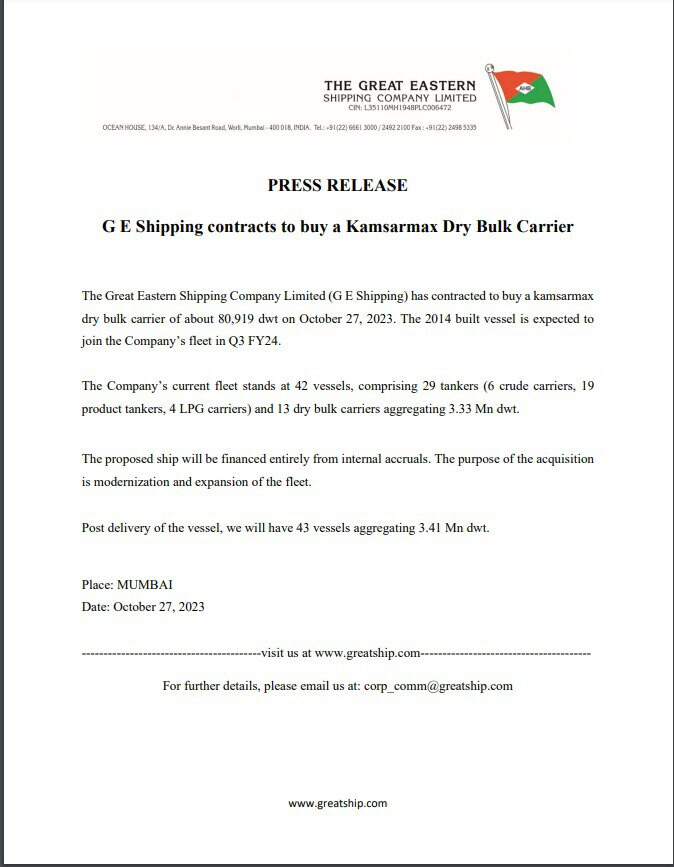

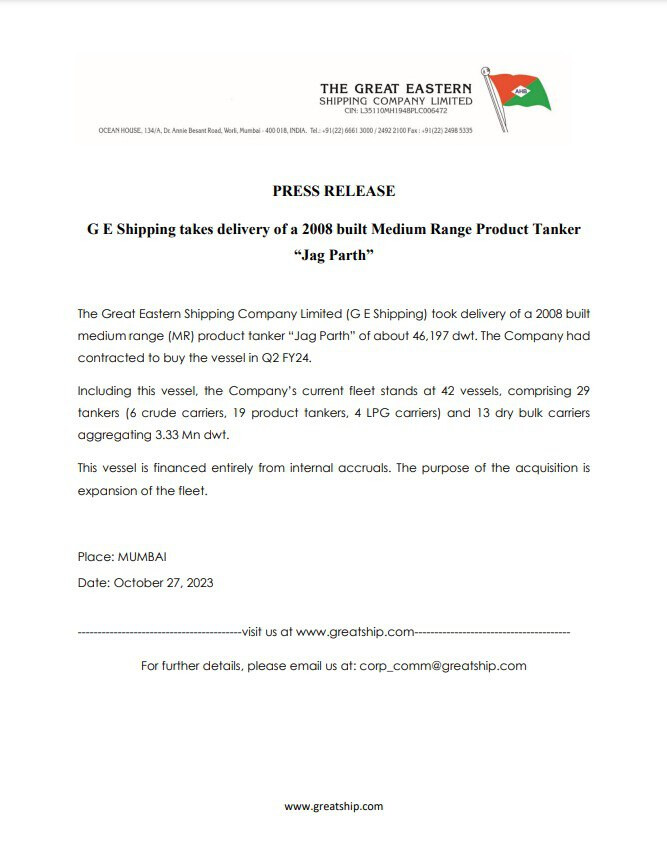

Great Eastern Shipping (GE Shipping) – Possible Sleeper? (27-10-2023)

GE Shipping Company have decided to:

- Buy a type of large cargo ship called a Kamsarmax Dry Bulk Carrier.

- Have received a medium-sized cargo ship called “Jag Parth,” which was built in 2008 and has a capacity of about 46,197 tons.

The company currently has 42 ships in its fleet. These include 29 tankers (which carry things like crude oil, product tankers, and LPG) and 13 dry bulk carriers (which transport things like grains and minerals), with a total capacity of 3.33 million tons.

Company used their own profits (internal accruals) to pay for these acquisitions/expansions, and the main reason for getting it is to expand their fleet.

Great Eastern Shipping (GE Shipping) – Possible Sleeper? (27-10-2023)

GE Shipping Company have decided to:

- Buy a type of large cargo ship called a Kamsarmax Dry Bulk Carrier.

- Have received a medium-sized cargo ship called “Jag Parth,” which was built in 2008 and has a capacity of about 46,197 tons.

The company currently has 42 ships in its fleet. These include 29 tankers (which carry things like crude oil, product tankers, and LPG) and 13 dry bulk carriers (which transport things like grains and minerals), with a total capacity of 3.33 million tons.

Company used their own profits (internal accruals) to pay for these acquisitions/expansions, and the main reason for getting it is to expand their fleet.