(post deleted by author)

Posts tagged Value Pickr

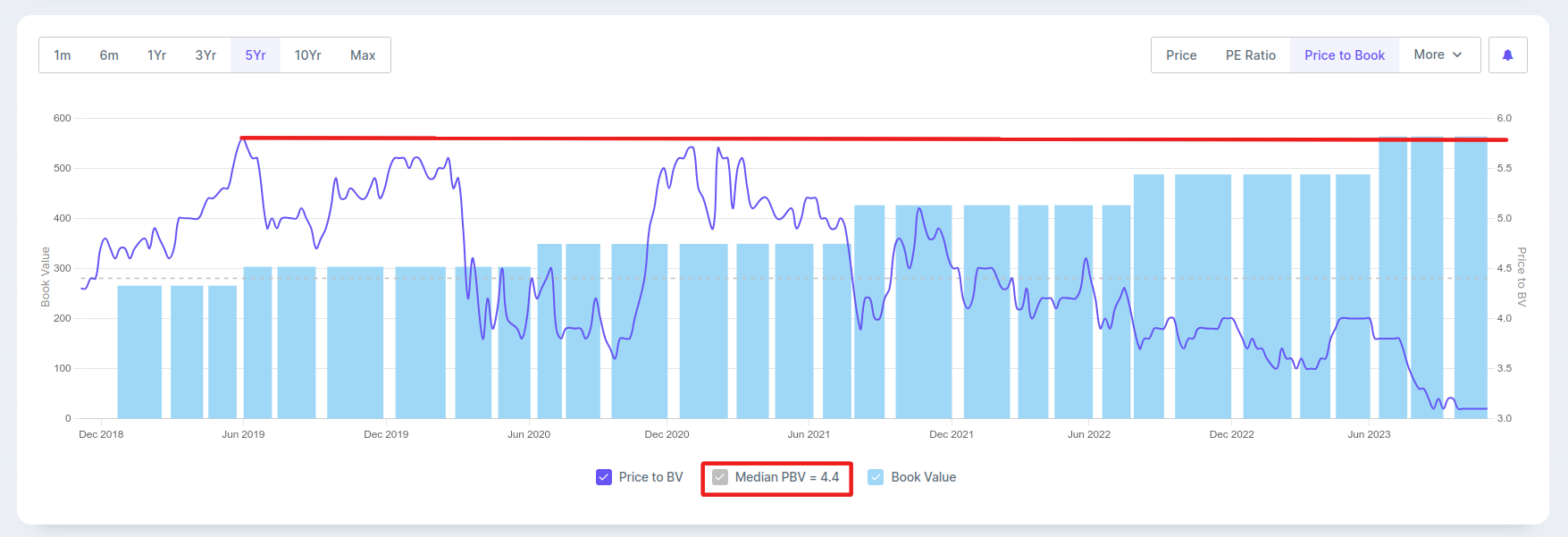

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (26-10-2023)

A very pertinent question is how does one assign a multiple to bank like Kotak? The bank is growing it’s book value per share at the rate of 15% yoy every quarter without fail. Also, the bank has been able to keep NNPA close to zero with advances growing at 15-20% yoy every quarter.

With Indian economy projected to grow at 6% for next decade this bank is well poised for a healthy long-term growth.

If history is any judge here are the historical multiples for the bank

Price/Book

21/oct/23 = 1769/605 = 2.9x

22/jul/23 = 1971/584 = 3.4x

21/jan/23 = 1760/540 = 3.25x

22/oct/22 = (1800/519) = 3.5x

27/apr/17 = 4.3x (900/209)

30/apr/18 = 4.5x (1222/264)

19/jul/18 = 5.1x (1400/272)

01/may/19 = 4.3x (1300/305)

22/jul/19 = 4.6x (1450/313)

Also look at the historical price to book value from the screener, median price to book is 4.4. So again the same question what price to book multiple will you assign to Kotak bank??

I think sometimes Mr. Market gives us Gold at the price of Copper and this is one of the case. Of course no one can time the market so we don’t know how long we have to hold to get some returns.

The only unsolved question from my end is, has the price to book value growth of Kotak bank slowed down, was it growing at 20% on an average between 2010 and 2020? I don’t have data for this.

Disclosure – Invested and biased.

Hitesh portfolio (26-10-2023)

We have had a brutal correction in overall markets since past few days. By now it’s become all too familiar. Whenever these corrections come about, the kind of downward force that is there takes most market participants by surprise. This has happened in the past also and is the case in most corrections.

When these corrections come about is anybody’s guess, and personally I have found them difficult to predict on a consistent basis.

How to negotiate them is often the big question. What I usually do is evaluate my portfolio stocks, and try to weed out the least conviction stocks, both in terms of fundamentals and technicals and try to get into new better options, or increase allocations to existing high conviction bets.

If we take a broader view on overall markets, 18880-18890 was a major top previously. In this correction we have reached those very levels. So logically based on change of polarity principles, we could get support at those levels. Nifty is close to 200 dema at around 18840. So current levels need to be watched for arrest of fall in Nifty and a possible tradeable bounce. Otherwise things can get ugly.

HBL is also in a corrective mode, and has corrected to levels of around 260 from highs of 310. This seems in line with the market correction.

@rmjp Logarithmic scale is used on very long term chart of months and years. For short to medium term, its better to go for normal price charts. While reading William O Neil’s book, (or any other book for that matter) try to focus on the overall learnings rather than getting stuck with a single point. We have to remember that this book was written decades ago, so some things may not apply to today’s markets. But if we get the overall concept described in the book, which is that of getting into stocks with both earnings and price momentum, it should serve us well.

KMC Speciality hospital (26-10-2023)

Please refer to the details of KMC capex on the recent Rating Update Pdf.

-Atmiya

PPFAS Financial Opportunities Forum (26-10-2023)

PPFAS’s view on small caps and small cap funds seems to be playing out almost flawlessly.

FYI, today is the next edition of the FOF. Focus area?

Artificial Intelligence.

Looking forward to it. If you are attending too, it will be great to catch up!

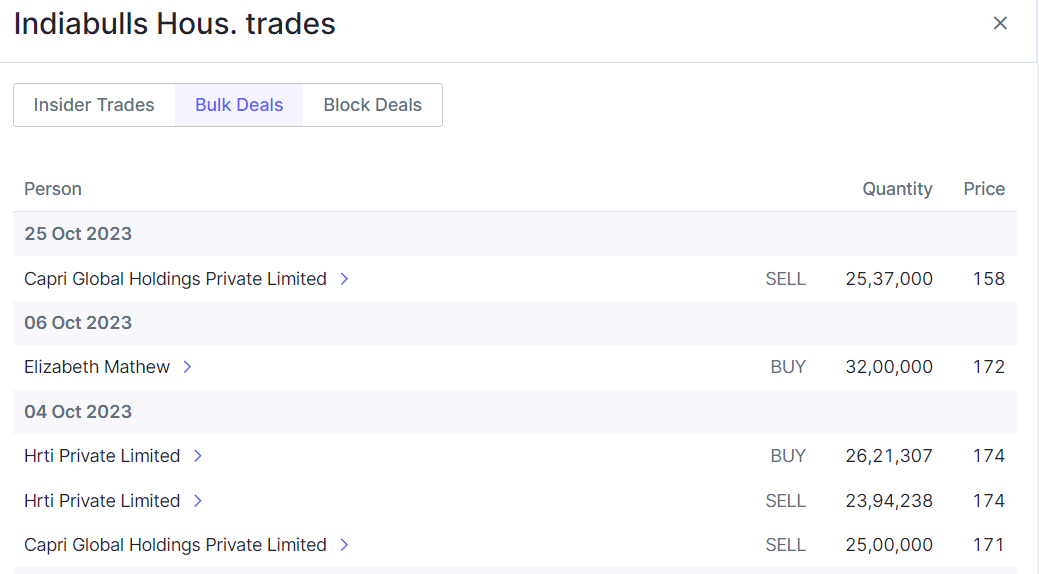

Indiabulls Housing – A compounder from here? (26-10-2023)

Is it possible that Capri would have shorted Indiabulls in F&O and selling in cash to create pressure?

Indostar Capital Finance Limited (26-10-2023)

Indostar sold their loans for 790 crore, which is an 86% recovery on the total loan outstanding of ₹915 crore as per the below article. Honestly I don’t know how it will be treated on the P&L statement and what impact it will have, we will get to know tomorrow.

KEI Industries Ltd – A consistent performer over the last decade (26-10-2023)

Kei ind update

(From credit rating ,concall)

KEI

1…Capex

A… Company plans to invest ~1,000 Cr over next 3 to 4 years to setup a manufacturing facility in Gujarat. It has bought property, and the first stage of the plant is projected to be operational within 18 months from beginning of construction.

…Gujarat project to start sales in Q4 FY ’25.

B… Company plans to invest Rs.50 Cr in expanding its Chinchpada unit. This project is scheduled to be finished in September 2023

C… Plans for a brownfield capex of Rs. 45 Cr in Silvassa plant to be completed by September, brownfield expansion by Q1 FY ’25,

=KEI has lined up a significant capex of ~Rs. 800-1000 crore over the next

three years, likely to be funded by internernal accurals

2…Order Book

Company has a order book of Rs.3,567 Cr, including EPC projects, extra high voltage power cables, and domestic and export cables

3…Segmental

Retail ~ 44%,

Institutional ~ 46%,

Export ~10%

4…U.S. market is a key focus for export growth.

…KEI received clearance for its LT cables, HT cables and solar cables for the US market. It will begin sales in the US market in the 4th quarter of FY 2022-23 to power, gas and petroleum sectors

5…End industries

=Favourable demand drivers in various end user industries such as power generation, transmission and distribution, railways, real estate, among others while maintaining its

profit margin profile.

=ICRA notes that the company’s products are witnessing robust demand from various end-user industries

that are benefitting from government infrastructure development activities, including urban and rural electrification, solar

power projects, tunneling and ventilation projects on highways as well as railway and metro rail projects.

=Additionally, private

capex is currently at healthy levels across sectors such as renewable energy, steel, cement and real estate, including housing

demand, under the GoI’s initiative of ‘Housing for All’

6…To boost its retail sales, KEI has increased its distribution

network to over 1,925 dealers pan India as on June 30, 2023 (Mar 31, 2022: ~1,800), in addition to increasing its employee strength.

7…Despite the commodity headwinds in FY2022, KEI’s margins remained protected on account of

a partial natural hedge as the company maintains an inventory for 2-2.5 months and passes on majority of the raw material

price hikes to customers.

8…NEGATIVES

=KEI’s moderate profit margin profile due to the adverse movements in raw

material prices and foreign currency fluctuation and intense competition in the wires and cable industry, which limits its pricing

power to an extent.

=The cable industry is inherently competitive with the presence of multiple large established

players such as Havells India Limited, Polycab India Limited, Finolex Cables Limited, V Guard Industries Limited, RR Kabel

Limited, etc., in addition to some competition from the unorganised sector. This limits KEI’s pricing power, to an extent,

especially in the retail segment, which is expected to drive its revenue growth over the medium term.

Disc…invested from lower level

Indus Towers Limited (26-10-2023)

The revenue for Q2 FY23 included a benefit of Rs. 1,076 Crores from deferred recognition of

revenues arising from the settlement of old dues with the customers. The same quarter also had an impact of Rs. 1,771 Crores due to provision for doubtful debt.

Net net, the revenues are up YoY if you remove the last year deferred recognition adjustment.

Good results in my opinion.

Indus Towers Limited (26-10-2023)

The Results for Q2 FY 2023-24 is out!!

Revenue Down 10% YoY at Rs.7,133 crores

EBITDA Up 23% YoY at Rs.3,456 crores

PAT Up 49% YoY at Rs.1,295 Crores

A Mixed set of results is what i feel after going through the same…

Positives :

- Good Turnaround with regards to PAT

- VI Paying the amount equivalent to monthly billing from january 2023 is a good sign, but still no clarity regarding the amount standing due till December 2022 the payment for which has not yet been materialised as per the Notes to F.S.

- Achieved 2,00,000 Macro Towers , a pretty good milestone!!!

Negatives :

- Why did the revenue fall despite data usage peaking every month?

- Need Clarity on the revenue aspect (Will Update after the ConCall(If Conducted))

- Finance Income has almost increased 10x…Need clarity on where the excess funds are being invested by the company.

- The extraordinary jump in Net Profit can be attributed to the low base in Sep 22 quarter during which the provisions were charged equivalent to Rs.17,706 Mn against Rs.1,335 Mn charged in the Sep 2023 Quarter…Except this Profit would have fallen since revenue has fallen and all expenses have increased this year

Overall, A Mixed Set of Results…No Big Positive Surprises and Negative Surprises either…

Disc : Invested…And Am an amateur…So kindly correct if i am wrong on any front…

Thanks ![]()

Link for accessing the Results & Press Release :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f2dd0f8e-c444-43ed-a3a0-d4fa252dadcc.pdf – Detailed Results,Notes & Audit Report

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c9f14d04-0a2e-40a7-902f-9d70de20c6f5.pdf – Press Release