High court stays new tax demand of 628 crore

Posts tagged Value Pickr

INEOS Styrolution India Ltd (22-10-2023)

Link to updated presentation –

Valuepickr goes Europe (22-10-2023)

Hi, Nice initiative. I am Revanth based out of Mainz, Germany. Please add me for future connects.

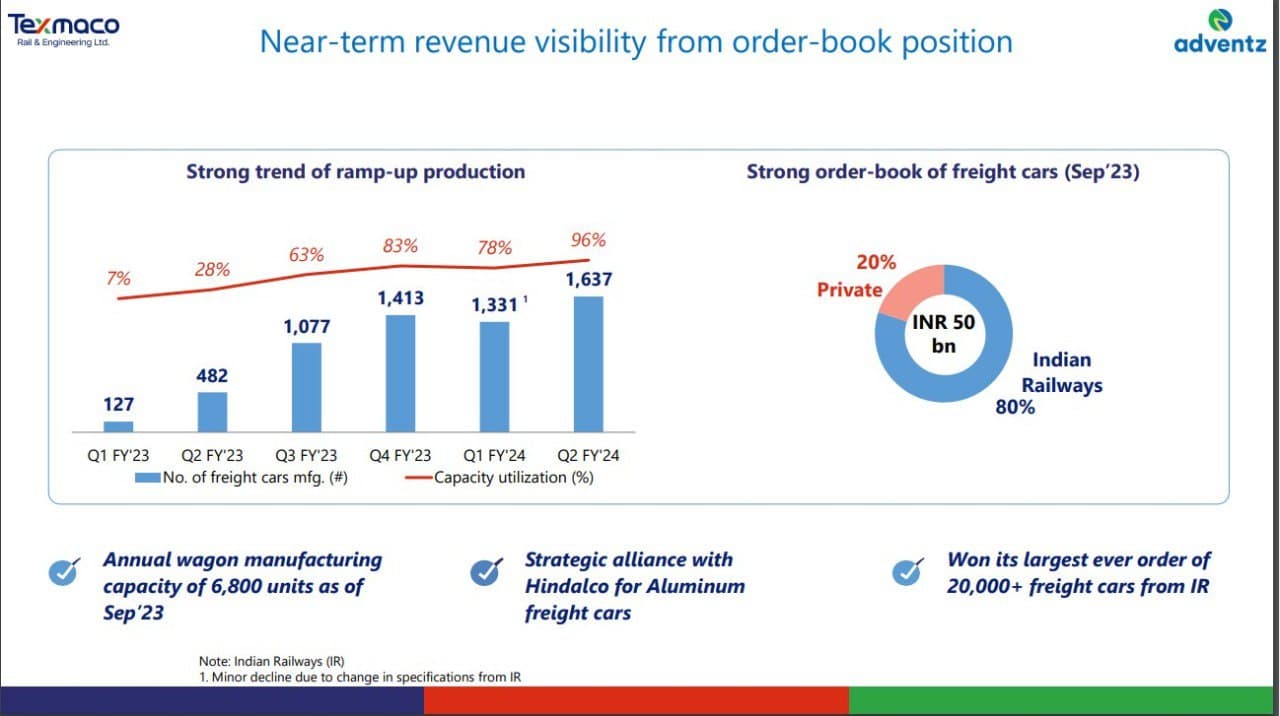

Texmaco rail and engg. – A high tech total rail solutions provider (22-10-2023)

Orderbook visibility and debt free plans in next 3 years

Texmaco rail and engg. – A high tech total rail solutions provider (22-10-2023)

Orderbook visibility and debt free plans in next 3 years

Vivek Gautam Portfolio (22-10-2023)

Some pearls of wisdom from Manu Rishi Gupta @manurishiguptha over the weekend.

The ten blunders to avoid when markets are touching all-time highs

The euphoria is unpalpable, The anchors at the top TV channels have already printed T-Shirts of “Nifty – 21000”. The Nasdaq is about to finally breach its life high (or at least it was just a few days ago) in a few days and there has never been a better time to believe that “This time it’s different”

I have been in markets since 1993 and like most 50 yr olds have seen a few booms, busts, scams and a few financial crisis. As a fund manager – when sometimes my clients ask me – markets are at all-time highs and making new highs everyday why are you not investing our money and simply holding on to cash.

I give all my clients 2 choices – Take Your money Back – Or be patient. But I ain’t changing my philosophy because of the pressure of capital deployment.

Even though I am always fully invested (personally), in markets (Levered to 120%) I am still almost always fearful, as Socrates keeps knocking within me subconsciously with his words – “Fools are always confident and the wise are always in doubt”

Perhaps I am a mad raging bull in a bear clothing. The bull in me keeps me hopeful and the bear allows me to be patient, cognizant of risks and to be non-greedy when everyone around me is convinced that this time its different. Perhaps that’s why our portfolios have been least volatile and have beaten markets with least amount of palpitations for our clients over a long term.

But the 10 lessons that I have learnt over the years and tried to imbibe in my investing style are as follows.

- Be bullish, not foolish

If the world is progressing and must keep moving ahead (with inventions, technology, opportunities, AI et al) markets will always go up over a long period of time. That allows us and encourages us to be a perma-bull ala Rakesh Jhunjhunwala. Sensex at 60,000 seemed like an impossibility some 10 years ago. Today its 66000. So being a bull almost always helps in the long run.

But in the short run becoming a muppet in the hands of commentators is the worst punishment one can allow oneself to be inflicted with. The narratives that emerge at the seeming peak of the markets are always almost misleading and suicidal.

Lesson

When a stock, an idea, or a sector is being pushed feverishly – AVOID.

- Breakout Stocks

Finfluencers are running paid courses on breakout stock strategy and thousands of gullible retail investors fall for this trap.

In the long run everything is driven by fundamentals without an exception (or else Yes Bank wouldn’t have become a No Bank and Suzlon would still be a blue chip) but in the short run, everything is driven by operators and insiders. How else do most shares start to perform or go down just before a major corporate announcement. Examples are galore not only in Indian markets but US as well.

Stocks break out not because the companies have become fundamentally adroit. They break out because too much money and fear is chasing too little items available. And that can make any s*** break out. Sub 1000 Crore companies that suddenly get new narratives built around them, coupled with incessant peddling of ‘the new promise in the lala land’ on social media and sometimes on business channels always prove to be a trap and wealth destroyers. Its surprising that almost all breakouts happen only when markets are peaking.

If Infy or ICICI or the likes of it break out, its great and merits attention but when stocks break out because of positive news (in most cases planted) while promoters are happily offloading their stake, not only should you be fearful, but you should also contemplate sitting out of the markets for a while. As Buffet famously quotes “Only when the tide goes out do you discover who is swimming naked”.

Lesson

If you are a superman and can get on a bullet train (thats running towards an abyss) and get off it – just in time, breakout investment strategy is ok. Else you will almost always get scorched.

- Beating the estimates

When rivers start flowing above the danger mark, the powers that be, worry little about the river or the impending danger. They just raise the danger sign by a few feet so that the river remains below the danger mark. Such is the story of the estimates by analysts. All estimates are always beaten because estimates are not based on the FCF or Earnings Yield. But based on a collective intelligence of sub-optimal and mostly clueless analysts who are experts in guesswork.

And sometimes estimates get beaten because of a low base effect, one-off income etc etc. For this one needs to delve deep into the financial statements. But beating the estimates is one of the most specious narratives to misguide the DIY and the gullible investor.

Imagine Nykaa listed at a peak valuation of some 1,16,000 Cr (Nearly 15 Billion USD) and analysts hailed it as a profitable company going into IPO while the Nayars privatized their profits and socialized the losses. Its present EPS is some 7 ‘paise’ while its trading at 70% below its listing price and still discounted more than 2200 times.

Over the long term there are just 3 things that matter for a strong stock performance that has any likelihood of creating wealth for shareholders. Valuation, Free Cash and Management intent.

Lesson

Stick to the basic principles of investment that have been in existence for decades. Analysts and their estimates can be great entertainment not the bedrock of sound investment strategies.

- Feeling good about bad data

Bad data is bad and good is good. However, markets have started interpreting this inversely. Can you imagine that if the US jobs and inflation data is good, markets react negatively and vice versa. Eventually, the reality will catch up and markets will realize that job losses aren’t good in the long run as data leads the reality by a few months and yet in the short run bad data almost always pleases the market till it doesn’t.

Lesson

If data is correct then trust the data and not the convenient interpretation of it. (eg. Bad data will lead to interest rate cuts and party of excesses will continue). Eventually, something that’s good for the economy will manifest itself into goodness and something that’s bad will manifest itself accordingly in not so distant future.

- Discounting the distant future in the present valuations

Decision of a Capital Expenditure by a company, or establishment of a new factory or a newly acquired business contract spread over multiple years almost always takes the stock price to tizzy heights. And human mind is wired to feel bullish on news that has not produced a single cent yet and no one really knows when it will – These traps are best avoided as euphoria almost always fizzles out. Does anyone remember the infra theme of 2006-2008? Most of those companies aren’t even listed anymore. The present defense theme is no different. Be cautious when buying into future stories.

Lesson

If a company is good it will keep creating consistent shareholder wealth. And any prudent investor will make money in that company’s lifecycle. (Buffet invested so late in Apple’s lifecycle – And How – he didn’t miss any bus or opportunity). Don’t invest just on the promise of a rosy future. Wait for your time.

6 The FOMO factor

History is replete with examples – and I have experienced it personally. If one really is in love with a stock and wants to create a position, the irresistibility upon hearing TV commentators and news flow is intense. But almost always every single stock that you want to buy today will almost always be available a bit cheaper few weeks or months down the line – Even if it’s the HDFC’s or the Bajaj’s of the world. All one needs is a bit of patience to wait and build a stronger conviction while the target or lower price is achieved. If FOMO could be quantified, its directly proportional to the level of indices. Most bitcoin retail aficionados invested between 50000 – 68000 USD. If Bitcoin is really a store of value why aren’t they doubling down at 20000 USD?

Lesson

Investments made in a state of FOMO are never sound investments. Date your stock, understand it better, observe it for a few Qtrs and then say Yes. You will never go wrong.

7 Recency Bias

Anyone who has vivid memories of 2000 and 2009 and remembers Pentafour Software, DSQ, HFCL, Global Tele and JP Associates, would resonate well with the perils of recency bias. When most of these shares fell from (approx.) Rs. 3000 levels by 20%, people rushed to sell their family silver and real estate to capture the opportunity of owning these blue chips of those times. Well eventually all of these companies got delisted and JP is now at an unfathomable level of Rs 8.

The point to remember is that a stock at Rs 1000 can well become a penny stock and the adage “how much more can it fall” is stupidity.

Lesson

Not only should you never catch a falling knife, don’t invest in story stocks. Companies that peddle stories and not profits will always destroy their shareholders’ wealth.

- Herd Mentality

Speciality chemicals was as crowded a trade, 18 months ago as Banking is now. Finfluencers were allowed to blatantly push narratives on TV Channels and the entire sector has destroyed a considerable wealth over the last 2 years. Indian Banks are trading at reasonably rich valuations while the CEO s of the same banks are subtly raising red flags on growth and margins yet the BAAP (Buy at any price) brigade is relentless – and while banking sector is the bedrock of economic growth of any country – valuations do matter.

Lesson

When everyone is chasing the same theme – it almost always spells trouble. DotCom in 2000’s, Housing in 2008’s had the same fate. AI is the new darling theme. Lets see what happens to AI and chip companies a few qtrs down the line.

- Cutting the flowers and watering the weeds

Peter Lynch famously quipped the above adage. I know more than a dozen people who are in love with Yes Bank and Vodafone rather than ICICI Bank and Bharti. A large number of DIY investors feel that the chances of a penny stock doubling are far higher than a respectable and a fairly priced stock. The ‘averaging on the way down’ brigade of Yes Bank, Unitech and JP Associates will continue to sell their winners while collecting mountains of trash.

Eventually such investors get ejected out of the markets forever.

Lesson

The performance of a company gets reflected in numbers and numbers get reflected in the Balance Sheet and the BS gets reflected in the stock price. Stocks are where they are for a reason. A red black on a roulette table offers a better probability of winning than holding onto The Yes’s and Vodafone’s of the world in the hope of they springing a magic.

- Falling in love with stocks or promoters

I recently heard a well known fund manager mention in a podcast how he was in awe of Mr. Gosh and Bandhan bank. This adulation towards a particular management clouded his ability to see the turning fortunes for the worse at the bank and eventually he had to exit the investment at a big loss to his investors.

It is easy to fall in love with stocks/sectors which have given good returns in the past. But this should not blind one’s rational thinking towards changing times. One key TV commentator keeps peddling the idea that the next HDFC bank is the HDFC bank itself, while the stock underperformed Nifty by a huge margin in the last 2.5 years and ICICI snatched the mantle of growth and consistency in the Indian Banking space.

Positive Management Commentary is another trap that most investors love to fall into. Bias clouds their judgements and the performance as well. And most investors get sated by just commentary. Which promoter will ever say that his future is bleak or give a negative commentary?

Lesson

Don’t cling onto stocks where data or price isn’t supporting or where the business model could itself face a headwind. If at all – cling onto relationships, great friendships and emotions – not stocks and commentary.

- Checking the price and not value

We all aspire to upgrade our standard of living (Car, House, Holiday destinations, etc) and happily pay a premium for superior quality and size. But some of the most prudent investors and sometimes fund-managers as well, take refuge of substandard – low priced stocks (penny stocks) in the hope of dramatic turnaround or a story that’s likely to unfold in some distant future. The propensity to indulge in this investment strategy is directly proportional to the index levels.

Lesson

If there is 1% chance that your investment behavior is vaguely similar to gambling, you are most likely to get into trouble. The probability of landing a multibagger amidst an ocean of crappy stocks is like finding a unicorn in a herd of donkeys.

If one could just avoid stupidities in ones investment journey over decades, there is no force that can stop you from compounding your wealth at an appreciable rate. And compounding – the eighth wonder – is everything isn’t it?

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (22-10-2023)

Finally Kotak gets a new boss, CEO appointed for 3 years.

Metro Brands – marketing footwear (22-10-2023)

Metro Brands Ltd –Q2FY24–Earning Call Highlights –20th Oct23 :

Consolidated Financials :

Revenue : 556Cr –Growth of 16.7% YnY

EBITDA : 156Cr –Growth of 5.6% YnY

EBITDA Margin : 28.1% vs 31.0% in Q2FY23

PAT : 68Cr –Degrowth of -13.2% from 78Cr in Q2FY23

PAT % : 12.2% vs 16.4% in Q2FY23

—Stand-Alone : Q2 FY24 witnessed higher YoY revenue growth of 14.8% as compared to 11.7% YoY growth in Q1 FY24, due to tapering of pent-up demand in Q2 FY23 (vs Q1 FY23).

Festive period is also delayed in FY24 v/s FY23 by ~ 2.5-3 weeks especially impacting Q2 sales v/s last year

Store expansion on track with net addition of 29 stores (7 new cities covered in Q2 FY24) across all formats during the quarter

Ecommerce sales (including omni-channel) for Q2 FY24 were Rs 60 cr. Growth momentum in Ecommerce sales (including omni channel) continues as sales grew 45%

—H1FY24 :

H1 FY24 has witnessed stable YoY growth as compared to H1 FY23 which had pent-up buying on easing of Covid restrictions & higher number of marriage dates

Store expansion on track with net addition of 56 stores (15 new cities covered in H1FY24) across all formats during the period

Ecommerce sales (including omni-channel) for H1 FY24 were Rs 121 cr. Growth momentum in Ecommerce sales (including omni channel) continues as sales grew 53%

Premiumisation Strategy with Over 3K Footwear a/cing for 48% of our Biz.

—Update on Fila Integration : 3 yr plan is to : continued efforts to clean up the inventory and rationalisation the distribution & current stores , 2nd year is to reset the brand and position it for success in the coming years & 3rd year will be focussed on acceleration

–Update on implementation of Bureau of Indian Standards for footwear :

The Department for Promotion of Industry and Internal Trade (DPIIT) issued BIS Quality Control Order (QCO) for footwear which was mandatory from 1st July 2023. The implementation date is now deferred to 1st January 2024 for most categories of footwear

While the industry is gearing up for quality control orders (QCO) compliance we expect significant clarity & progress to transpire over next 2 quarters

In order to circumvent any potential supply chain disruptions, MBL has front loaded inventory buying to some extent ,This would lead to higher inventory levels till Mar24

—Read on the prevailing consumer trend in Footwear : We are seeing Temp. headwind of timing , more than the economic head-winds so challenges we faced is due to the pent up demand from last year & the shift in festivals which really is a temp. head-wind of timing and not economic headwind, overall the consumer in our segment is resilient & is appreciative of product offerings that we have

–Margin profile of Online segment and break-up of it ? —-One reason why Ecomm for us is low double digits is because we don’t want to get into discounting game & unfortunately it’s the main stay of Indian etailing today & our biz is is done in multiple ways i.e we see directly to the mktplaces & main biz which we nurture is omni-channel biz where we line up the inventory across all our stores in different platforms and we package it as 2fold : one is we are able to increase our inventory distribution by getting products across the country and also reducing our time for delivery & 2nd is we are able to control any discounting which happens online which is unfavourable to us.

& overall the margin profile is relatively healthy in line with our regular biz and Ecomm is not an easy biz overall with the cost associated so just on the margins profile you look at the end cost profile for pure play ecomm players and its not a very profitable profile for most people. The way we try to grow it is to curate the ranges that will add to both the brand salience and also …

Fila Integration : This year will be spent on Cleaning up the Inventory as its not in line to reflect where we want to take the brand in the coming years & that’s work in progress & hence you need to look at our stand alone no.s to read how our biz is doing & 2nd one is store expansion where we need to rationalise the stores and the distribution i.e the route to mkt that we have today i.e when we look at our real-estate deployment of stores we want to position it both in the right Mall but also in the right locations in those malls as it makes a big diff. on perception of consumers

& distribution to other channels outside of us need to be tightly controlled , expensive discounting & over stocking that further leads to brand disconsonance down the road so this distribution piece is a critical part of how we are going to be approaching in later part of this year and early part of next year

& the last is position —where we strongly believe in Sports Fashion space Fila has relevance , aware ness somewhere similar to building it like the China model where China Fila does roughly 4 Bn $ because they position themselves diff. than typical athletic brands & we see that consumers in India migrating towards that as well & legacy inventory clean-up will be done by FY24

–Ecomm –Online and Omni-channel sales : Right now is a period of immense discounting sales / festival sales that go on the Amazons of the world & that is no different than last year being booked in Q2 and hence you see that ….XYZ ….but Omni still grew very solid over the last season and it continues to grow relative to the rest of the biz as rest of the biz is also little challenged

–Among regions East is not doing well but West is good ,so whats the strategy here for Store additions etc ? —-Its not that east is not doing well as big season in east is Durga Puja which was in Q2 of last year and this year its flowing into Q3 & that is the key driver & when you talk of penetration not being high in the east is correct as its our smallest mkt but its a matter of us not having gone after it just yet so there is opportunity there for us . The west & south continue to be our strong-holds & East is also good as 13% of stores in the east contribute 14% of our sales ( slide 23 ) & this H2 Durga Puja is in H2 and East is imp. region for us and our focus is to expand there

–Crocs is slower expansion , reasons ? —-Its not really much slower than rest of them , what you are seeing is accelerated growth across i.e 4 yrs ago where we grew it from 0 stores in the last 5 years we have added stores & in Q2 we added 2 stores & this year FY24 we will add 20+ range of Crocs stores .We have guided that we will open about 100 stores & in line with the growth of our Metro & Mocchi stores which are imp. for us as well & overall the mkt size for Crocs is not as significantly wide as for Metro or a Mocchi ( they can go go to 400 cities in India ) & Crocs is not that big but still its a big opportunity

—Opex growth is much slower than the topline growth as well as Sqf addition so please provide clarity ? —- It’s a continuous exercise and its in line with sales growth , overall PBT level there is an impact of 1% due to ESOP cost and INDS 116 impact generally comes when you are opening stores aggressively but cost control is an ongoing exercise for us

—Crocs : Every city which has a Metro or Mocchi can not take a Crocs today and India is changing rapidly and Tier2&3 will be hot-beds of growth in Future so it’s a matter of Balancing in what is the right time to enter a city , we don’t see it has reached its full potential as it has more run-way in West and South for growth . We also sell them in existing stores

—Walkway : We closed 17 De-mart stores earlier 2021 so it went backwards of about 25 Store count . The walkway consumer is strong & we want to make sure that we understand it well before we accelerate it & its still WIP –we will deploy resources to unlock its potential

& we don’t see it only in Tier2/3 cities & its consumer segment existing in big cities as well

& Metro & Mochi the avg. capex is 1 to 1.2Cr & this includes inventory , store fitout and security deposit we pay to the landlord & for Walkway this no. is close to 70/80 lakhs & In terms of Profitability since it’s a value brand it wont generate similar profits in % terms as what Metro and Mochi would do & our endevour shows over a period of time we build in a model which helps us generate the same Return on capital employed as that of Metro/Mochi as thats our long term plan

–Avg. Realisation of H1FY24 & Compared that to H1FY23 and if I calculate that for Q2 , the Avg. realisation per Unit seems to have corrected on YnY basis ( only in this Q2 ) ,so is it that Avg. realisation for In-house brands is reducing & 3rd Party brands is increasing ? —In Q2 , we have end of season sales so Avg. ASPs move to slightly lower in Q2 if you compare it with Q1 and if you compare it with last year we have seen an Avg. ASP growth of around 3%

& we have seen our contribution of End-of-Season sales inch up slightly up vs last year so last year it was around 5% and now its 7.5% in H1 so that also has slight impact on the ASPs & gross margins

Revenue per Sqft was down 9% in this Qtr so despite it the gross margins for H1FY24 is 58% so what is the guidance for GM still remain at 55/57% level or would you be revising it upwards ? — Lot of it is due to mix of stores as our most high high productive Sqft is Crocs & you will see some naturally take place as we grow Crocs and we also saw that we went into 8 new cities and new cities take a while for store to get going & we ensure its cash positive in 2 yrs so we have guided that we will hit 55 /57% pretty consistently as we look to the future.

–Gross Margin for Private Lable this Qtr ? —its close to around 35%

–How sustainable is the growth in online channel as I believe majority of it would have been driven by Fila and Proline ,as before this acquisition of Cravatex the Ecomm contribution to sales was around 8% and now its 10% , thought on growth patterns for this channel ? —Its not driven by Fila and Cravatex ,its only Metro brands standalone no. we have been reporting which is 11% so its really a growth without consolidated no. so its not driven by those 2 & India will become digitally savy and in future tech will ease the way as we move forward some of the friction points in Shoes ( which has a return % of 30% ) so brick & Mortar will continue to have vibrancy and need in the mkt & convenience of Ecomm channel

—Internal tgt for Ecomm channel ,as its 60Cr run-rate for Q2 with 240/250Cr so any internal tgts ? —-Our goal is to maximise the growth in all channels without eroding the profits & brands value and its sustainable & that is an evolving no. and we cant comment on it

–Slide no. 26 ASPs and Price points for the Q2, product pricing sales mix , more than 85% of sales is drived from products which are priced 1500 to 3000 & 3000+ but when we look at Avg. shoe price its around 1500/- so since we don’t have volume data , trying to figure out why ASP is around 1500/- whereas more than 85% sales is coming from products more than 1500 & even more than 3000+ ? —-ANSWER

& This is primarily due to impact of accessories , we sell lot of them with price points even below 500/- as well eg. Crocs Snippets which is 300/350INR per piece so if you see ASP for footwear specfically it would be around 2200/2250 INR

–Margins : If we see ex of Cravatx brands its very much comparable to the last year H1 no.s and this is despite the fact that there has been some dryout of sales per sqft & there is a 100bps impact due to ESOPs & INDS impact so what is really helping to drive this margins ? —Our GM are more or less in line & if you see we have seen increase in our 3rd Party brands & this increase to 30% is primarily driven by Crocs where we enjoy GM similar to our in-house brands & hence you don’t see any significant impact of that on our incoming GM that you saw hence its relatively stable , below the line, we also keep tight watch on expense line items , another imp. point is most expenses are variable in nature so it also helps , i.e increase in sales will see increases in expenses & in lower Qtrs it helps so its a combination of all these factors drive this.

& in standalone no. the sales has grown by 13% in H1 and our PAT has grown by around 8% , wherein explanation of 1% delta due to ESOP & INDS and balance 50/60bps is on a/c of certain increases under certain line items

–Contribution of 3000+ segment has remained at that 40% avg. for H1 , what kind of segment is contributing to this 3000+ product contribution ? —We have 2 brands of JFontini and Davinchi’ which are our own brand which we operate in Metro and Mochi stores that focus on more premium product ranges & we are seeing growth on both those brands 2) Crocs Avg. ASP is much higher than 3000/- so is Flip-flop where its 7000/- and then we also carry key brands like skecthers and Birkenstock which also have high ASPs & this is attributed to pent-up demand and diff. consumers who want to maintain that level of Quality and Value in our products

—Demand : Early indications are in line with our expectations i.e East is closer to Durga Puja and we are seeing impact of that & lot of these things you cant map all this as there are many variables and we are confidant that this was a timing headwind and not an economic headwind

—Revenue/Sqft : Last 2 Qtrs we saw 5500/-revenue per Sqft , can we broadly say that , the new normal will be this around this 5000/Sqft or its due to timing issue or it can revert back to that 5500/Sqft ? —-We will get back to that no. and there are lot of variables and lot of that is to do with new stores that we open & new stores in the town where we open and then concept that you open i.e Crocs is a high sales / Sqft but Metro does significantly more volumes than Croc does so you have to look at it in balance and last year post pandamic getting to a 5500/Sqft no. was the guidance on annualised basis

–At store level we offer a high level of Variable pay to our staff which incentivises them to get more sales , so at store level what is the split between fixed n variable component ? —Broadly the split if 60/40 where 60 being fixed and 40 variable , it differs depending upon space and cities & for Managers the entire amount is variable

–Other aspects which are different which has made us a leading player in the industry ? —-We see it as executing the details of retail every single day & making sure we are focussed

–Fila breakeven : We will tgt it towards the end of FY25 Q4 is our endevour to break-even

PS : I may have mis-heard some points due to the pace of the conversations , please refer to detailed transcripts for clarity when its published

Bhansali Engineering Polymers – An Import Substitution Story! (22-10-2023)

Bhansali’s results –

The results look decent. For updates on their expansion problems, check out the last 2 pages of the above earnings results document.

This foillows Styrenix’s positive results. Supreme Petro (an emerging competitor) has also seen its stock price rise considerably of late.

Xpro India – getting bigger? (22-10-2023)

No. As per the comment from Sahil, first you need Biax film and then you can metallize it. Cosmo doesn’t seem to have capabilities (at least till now) to manufacture Biax films.

Cosmo may end up being a customer of Xpro, buying biax films from them and then metallizing those films.