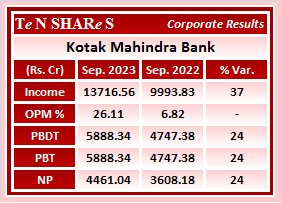

3QFY23-24 Results

Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/df34e601-1ddd-4af9-8b43-4e2cdfbeb385.pdf

Financial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/be1afdcb-bbde-4868-8d56-552716d871a2.pdf

While there are many negatives in the results. There are a few positives

So, once the Capex starts contributing EBIDTA Margins should move towards 25% and may be reach 28-29% in 2-3 years time as the CDMO business pie grows

If we assume the Co makes 8000 cr revenue and 25% Margin in FY 25, the Co is trading at 12-13x Ebidta multiple, which is not cheap by any means.

While there are many negatives in the results. There are a few positives

So, once the Capex starts contributing EBIDTA Margins should move towards 25% and may be reach 28-29% in 2-3 years time as the CDMO business pie grows

If we assume the Co makes 8000 cr revenue and 25% Margin in FY 25, the Co is trading at 12-13x Ebidta multiple, which is not cheap by any means.

Detailed Analysis of Geekay Wires Ltd Market Cap: 316 Cr. 5-year Sales CAGR: 26% 5-year Profit CAGR: 100% ROE: 42% ROCE: 27% PE: 10x

Let’s deep dive into it![![]() ]

]

Business Overview:

-Geekay Wires Limited is an ISO 9001:2008 certified company, located in Hyderabad

-The Company was taken over by the Kandoi Family in 2012

-Geekay Wires has been in the biz of manufacturing high-quality galvanized steel wires & other different wire products

Geekay manufacturers niche quality of

Catering to vast Industries like:

-Industrial, Power Transmission,

-Cable and conductor,

-Commercial Construction,

-Automotive industries,

-Marine & mine Industries,

-Wind & solar Power Energy &

-agriculture applications

In short, the Proxy to Capex cycle & an FMEG Player

Production Process of Wires:

-Main RM is Wire Rod (High Carbon steel)

-Zinc is used for galvanizing the steel wire

-Acid Pickling removes impurities

-Wire drawing provides shape & density

-Galvanizing to make it rust-proof

-Stranding to make the product perfect

-Final testing

Production Process of Nails:

-Drawn Steel Wire Rod main RM

-Nail-making machines give shape as per requirement

-Nail polishing unit gives finishing to the nail

-Then, Plastic or Wire Nails and Thread Rolled Nails can be made from that polished nail

Raw materials used:

-For steel wires & nails it’s wire rod

-For GI steel wire it’s Wire rod + Zinc

RM is procured from both international & domestic markets

Also, entered into an agreement with Hindustan Zinc Limited & Rashtriya Ispat Nigam Limited for the supply of raw material

Manufacturing units:

Unit 1 at Isnapur Village, Medak District, Telangana

Unit 2 at Shankarampet Village, Medak, Telangana

Geekay has an installed capacity of 30,000 MTS PA of GI Steel Wires in various grades & sizes and 30,000 MTS PA of Nails & 10,000 MTS PA of SS Nuts & Bolts

Cliente Profile:

Preferred vendors of PGCIL(Power Grid Corporation of India Ltd) in most of the State Transmission & Distributions companies across India. Geekay also exports products to various countries including USA, Canada, UK, Australia, Saudi Arabia & Germany

Industry Growth/Driver:

-India’s domestic steel demand is estimated to grow annually by 5-7% in Next 3-4 years

-The construction industry in India is expected to expand by 5% in real terms in 2023

-In the Budget 2023-24 the PM & FM have announced Rs. 10 lakh crore capex plan

Key Competitive Advantage of Geekay Wires:

Key Variant Perception playing out:

Sources of Future Earnings:

Financial Analysis:

Will Put it Crisp, One can check the screener for a detailed one

-GP Margin has expanded to 21% from 16%

-PAT Margin has expanded from 3% to 6%

Mainly margin is expanded through improvement in GP Margin & Operating Leverage

-Employee intensive production

Segment Analysis:

-Sales growth of Export Vertical is more than Domestic Vertical in last 3 years

-Last FY Director remuneration increased by 91%, but still in a limit when compared to % of PAT

Ratio Analysis:

-D/E reduced from 2 to 1.3 times

-Interest Coverage improves from 2 to 6 times

-ROE expanded to more than 30% led by PAT margin & Operating Leverage

-Asset turnover also improved & now around 2 times

Efficiency Analysis:

-Receivables turnover ratio improves

-Inventory Turnover improves

-WC Days reduces

-Good CFO conversion in FY23

Valuations:

-P/E around 10 times, median PE is 10.6 times

-EV/EBITDA around 6.6 times, median is 7.4 times

-Industry PE is around 20 times

-Available at a discount to median & Industry level valuations with good sales growth, WC improving & good CFO conversion

Peer Comparison:

It’s closest competitor is DP Wires and other competitors in some products are Usha Martin & Bharat Wire Ropes

DP Wires:

-Sales growth is more than Geekay in 5 years (42%) but Profit has been lower (just 33%)

-GP Margin reduce drastically

-ROCE & ROE constant & above 20%

-WC cycle improved & Asset turnover led ROE Growth

-Available at 21x double the valuation of Geekay

Why does Geekay trade at the lower multiple?

Reason

-Continues inclusion in AGM & ESM List (Caps liquidity & trading)

-High Debt can also be the reason

-Might be still market is accession the stability of operations (Margins & Growth)

Anti-thesis:

Hope you will like it!!

Strictly, No Recommendation

Open for discussion!!

Note: Can’t able to post images because of new member restriction. one can check proper one on twitter

Also, more active on Twitter… if anyone want to connect

https://twitter.com/BansalSwapan

Detailed Analysis of Geekay Wires Ltd Market Cap: 316 Cr. 5-year Sales CAGR: 26% 5-year Profit CAGR: 100% ROE: 42% ROCE: 27% PE: 10x

Let’s deep dive into it![![]() ]

]

Business Overview:

-Geekay Wires Limited is an ISO 9001:2008 certified company, located in Hyderabad

-The Company was taken over by the Kandoi Family in 2012

-Geekay Wires has been in the biz of manufacturing high-quality galvanized steel wires & other different wire products

Geekay manufacturers niche quality of

Catering to vast Industries like:

-Industrial, Power Transmission,

-Cable and conductor,

-Commercial Construction,

-Automotive industries,

-Marine & mine Industries,

-Wind & solar Power Energy &

-agriculture applications

In short, the Proxy to Capex cycle & an FMEG Player

Production Process of Wires:

-Main RM is Wire Rod (High Carbon steel)

-Zinc is used for galvanizing the steel wire

-Acid Pickling removes impurities

-Wire drawing provides shape & density

-Galvanizing to make it rust-proof

-Stranding to make the product perfect

-Final testing

Production Process of Nails:

-Drawn Steel Wire Rod main RM

-Nail-making machines give shape as per requirement

-Nail polishing unit gives finishing to the nail

-Then, Plastic or Wire Nails and Thread Rolled Nails can be made from that polished nail

Raw materials used:

-For steel wires & nails it’s wire rod

-For GI steel wire it’s Wire rod + Zinc

RM is procured from both international & domestic markets

Also, entered into an agreement with Hindustan Zinc Limited & Rashtriya Ispat Nigam Limited for the supply of raw material

Manufacturing units:

Unit 1 at Isnapur Village, Medak District, Telangana

Unit 2 at Shankarampet Village, Medak, Telangana

Geekay has an installed capacity of 30,000 MTS PA of GI Steel Wires in various grades & sizes and 30,000 MTS PA of Nails & 10,000 MTS PA of SS Nuts & Bolts

Cliente Profile:

Preferred vendors of PGCIL(Power Grid Corporation of India Ltd) in most of the State Transmission & Distributions companies across India. Geekay also exports products to various countries including USA, Canada, UK, Australia, Saudi Arabia & Germany

Industry Growth/Driver:

-India’s domestic steel demand is estimated to grow annually by 5-7% in Next 3-4 years

-The construction industry in India is expected to expand by 5% in real terms in 2023

-In the Budget 2023-24 the PM & FM have announced Rs. 10 lakh crore capex plan

Key Competitive Advantage of Geekay Wires:

Key Variant Perception playing out:

Sources of Future Earnings:

Financial Analysis:

Will Put it Crisp, One can check the screener for a detailed one

-GP Margin has expanded to 21% from 16%

-PAT Margin has expanded from 3% to 6%

Mainly margin is expanded through improvement in GP Margin & Operating Leverage

-Employee intensive production

Segment Analysis:

-Sales growth of Export Vertical is more than Domestic Vertical in last 3 years

-Last FY Director remuneration increased by 91%, but still in a limit when compared to % of PAT

Ratio Analysis:

-D/E reduced from 2 to 1.3 times

-Interest Coverage improves from 2 to 6 times

-ROE expanded to more than 30% led by PAT margin & Operating Leverage

-Asset turnover also improved & now around 2 times

Efficiency Analysis:

-Receivables turnover ratio improves

-Inventory Turnover improves

-WC Days reduces

-Good CFO conversion in FY23

Valuations:

-P/E around 10 times, median PE is 10.6 times

-EV/EBITDA around 6.6 times, median is 7.4 times

-Industry PE is around 20 times

-Available at a discount to median & Industry level valuations with good sales growth, WC improving & good CFO conversion

Peer Comparison:

It’s closest competitor is DP Wires and other competitors in some products are Usha Martin & Bharat Wire Ropes

DP Wires:

-Sales growth is more than Geekay in 5 years (42%) but Profit has been lower (just 33%)

-GP Margin reduce drastically

-ROCE & ROE constant & above 20%

-WC cycle improved & Asset turnover led ROE Growth

-Available at 21x double the valuation of Geekay

Why does Geekay trade at the lower multiple?

Reason

-Continues inclusion in AGM & ESM List (Caps liquidity & trading)

-High Debt can also be the reason

-Might be still market is accession the stability of operations (Margins & Growth)

Anti-thesis:

Hope you will like it!!

Strictly, No Recommendation

Open for discussion!!

Note: Can’t able to post images because of new member restriction. one can check proper one on twitter

Also, more active on Twitter… if anyone want to connect

https://twitter.com/BansalSwapan

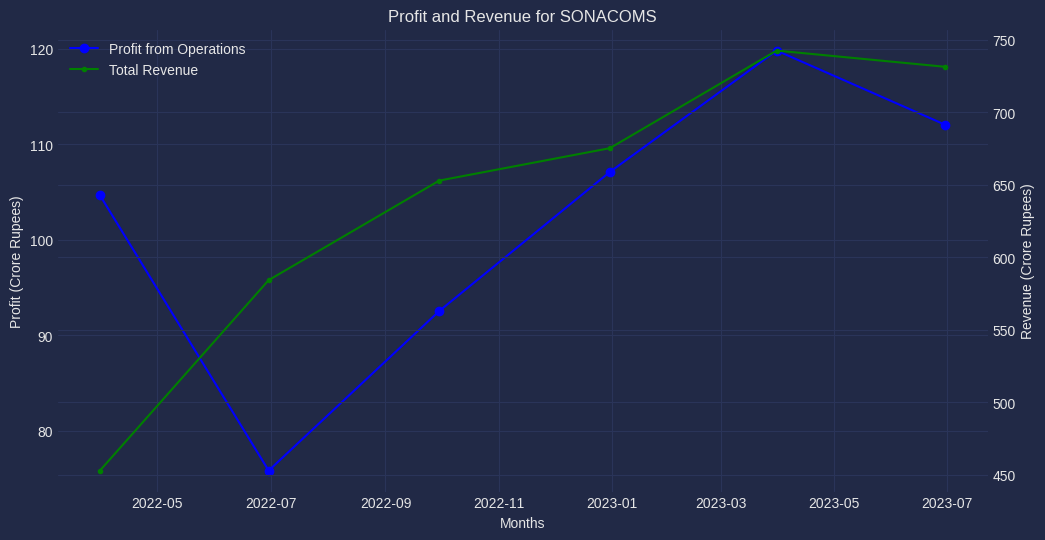

Nice analysis. The US interest rate has been rising for more than 1 year and yet the company has shown almost consistent revenue and profit growth. Please see the figure above.

In fact, the stock price has been rising since April reflecting the growth above.

The labor strike is a very recent event in September 2023 which perhaps explains the slight dip in the recent quarter and also compounded by the flooding of the market by Chinese EV as you have mentioned.

Sorry, if I missed it earlier, but which Portal are you referring to…

It looks like Laurus Management (with due respect to them) is not good at forecasting, understanding business volatility hence most of the time miss out on projected EPS.

I stayed away from this business after initial small investment due to volatile nature of the business and average projections by the Management.

Disc : No investment since was unable to understand the volatile nature of the business.

It looks like Laurus Management (with due respect to them) is not good at forecasting, understanding business volatility hence most of the time miss out on projected EPS.

I stayed away from this business after initial small investment due to volatile nature of the business and average projections by the Management.

Disc : No investment since was unable to understand the volatile nature of the business.

Q2 FY24 : Result and Presentation