ADF Foods – 20% topline growth in FY24 and topline double by FY26

Posts tagged Value Pickr

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (18-10-2023)

It looks like a commercially made clip , does not look real. That’s purely my opinion , i may be 100% wrong. We need more authentic proof.

Tips Industries Limited – Ready to RACE ahead! (18-10-2023)

I think it’s set for a massive bull run

Tips Industries Limited – Ready to RACE ahead! (18-10-2023)

FII’s and DII’s have finally started to buy into TIPS Industries…!!

Bajaj Finance Limited (18-10-2023)

the Company has entered into a binding term sheet with Pennant Technologies Private Limited (‘Pennant’) on 16 October 2023, at or about 8:40 p.m., for acquisition up to 26% equity stake in Pennant.

The object of the strategic investment is to strengthen Company’s technology roadmap.

This is significant for the long term strength of the company. Jio Finance in it’s presentation has clearly shown it’s focus on Tech to grow business.

National Peroxide (18-10-2023)

please update here if anybody has any any updates regarding the listing date.

Megamind portfolio (18-10-2023)

Added Fine Organics at ₹4880

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (18-10-2023)

The Reserve Bank of India (RBI) has, by an order dated October 17, 2023, imposed a

monetary penalty of ₹3.95 crore (Rupees Three crore Ninety Five lakhs only) on Kotak

Mahindra Bank Limited

Reportpertaining to ISE 2022, and all related correspondence in that regard revealed, inter alia, non-compliance with the aforesaid directions by the bank to the extent it (i) failed to carry out annual review / due diligence of the service provider, (ii) failed to ensure that

customers are not contacted after 7 pm and before 7 am, (iii) levied interest from disbursement due date instead of the actual date of disbursement, contrary to the terms & conditions of sanction, and (iv) levied foreclosure charges despite there being no

clause in the loan agreement for levy of prepayment penalty on loans recalled/foreclosure initiated by the bank

While the penalty is paltry and no major ramifications, it does shows how the Banks rarely follow rules.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (18-10-2023)

@Chins Thank you for the scuttlebutt update.

I have had cursory look at Ugro Capital and have not been comfortable with overall setup. I have not done deep dive work. It would be good if you can help with following basic questions.

- How does the profitability gets shared in the co-lending model between bank and NBFC? Who dominates the underwriting decision and consequently who has to provide for slippages?

It would be good if you can explain above points with current balance sheep of Ugro as an example.

The reason for asking this is simple. Banks struggle to make 1.5-2% RoA as it is on a consolidated diversified book. Corporate lending and housing loans are low RoA segments. So to boost RoA, banks have to go after credit cards, gold loans, MSME, consumer appliances financing, personal loans etc. These segments provide 3-4% RoA and at an overall level bank makes 1.5 to 2% RoA.

In this case, it looks like Ugro has ambition to make 4% RoA and bank wants to make 3% RoA. That is 7% RoA – which is really high !!!

To achieve this kind of RoA, you have to go after risky segments – unsecured lending, micro enterprise loans etc. You also have to go to kind of customers who are willing to take yield on advances of 20%+.

I am also seeing that collection efficiencies are in the range of 95% which means that credit costs are 4-5% range – which means yield have to be even higher.

With this kind of setup (poor segments, poor customers), why should one get excited about co-lending?

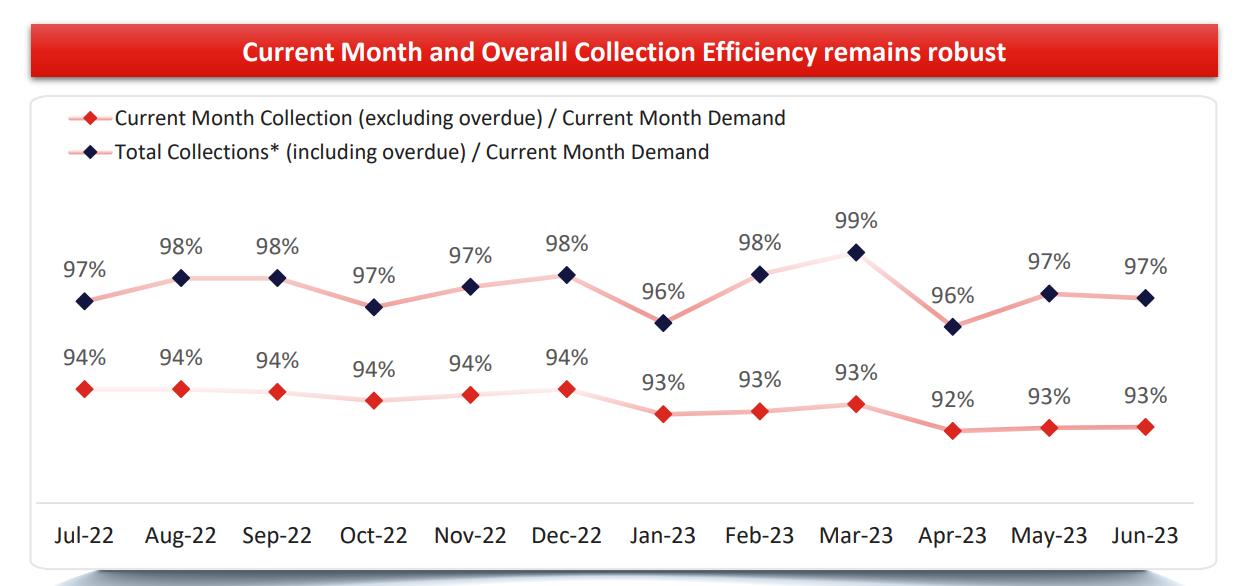

- Following chart is quite worrying for me. When a finance company is growing at fast pace, assumption is that new loans will not become NPA. Which means that collection efficiency numbers should look very good. In this case, I am seeing collection efficiency numbers of 93% even with the fast growth. Which means one of two things – either new loans are also slipping or old loans are slipping at a very high rate (10-15% of the book type).

Please help to reconcile this low collection efficiency numbers.

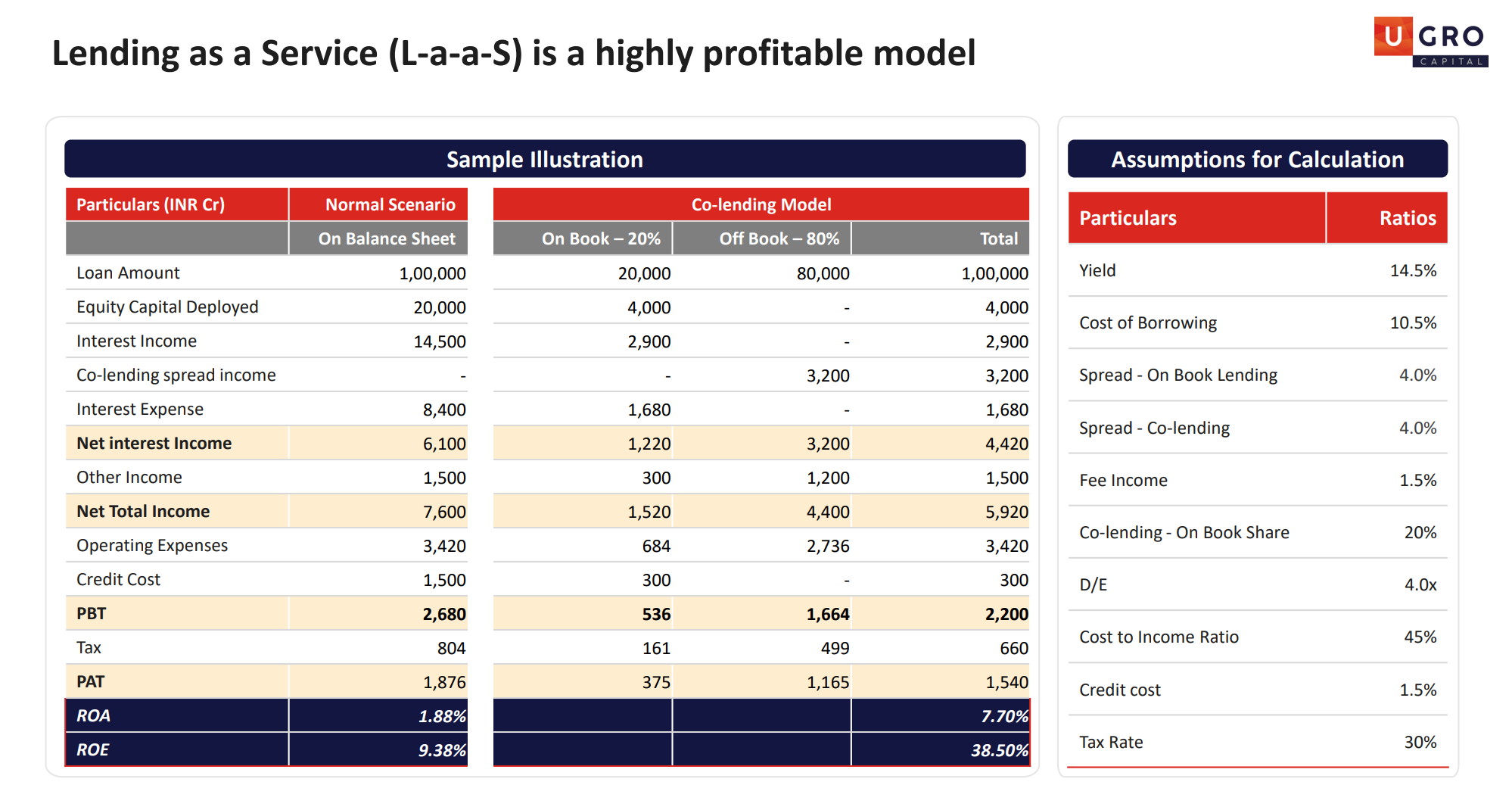

- I also do not get this slide below.

In on-balance sheet model, one is making PAT of 1876 rupees on Asset of 1,00,000 Rs. RoA – 1.8%.

In hybrid balance sheet model, one is making PAT of 1540 rupees on Asset of 20,000 Rs. RoA – 7.7%.

Who are these banks who are willing to take 80% of loan on its book, bear the 80% credit cost and only take miniscule profitability – at NII and PAT level.

Bank’s share of NII = 6100 – 4420 = 1680

Bank’s share of Credit cost = 1500 – 300 = 1200

Bank’s share of PAT = 1876 – 1540 = 336.

i.e. PAT of 336 rupees on asset of 80,000 i.e. RoA of 0.42% !!

It looks like a super raw deal for the bank and very hard to believe.

Bank is taking all the risk on its balance sheet and giving away all the profitability to what is essentially a sourcing agent.

I would expect that bank would have more power on negotiation table.

Disc – No investment whatsoever.