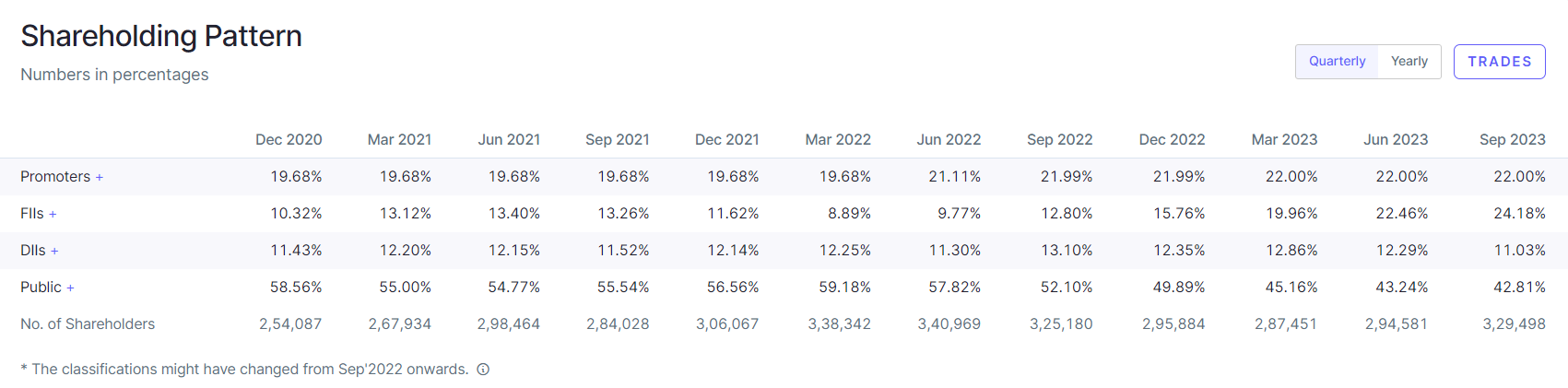

SHP from Screener:

From Mar 2022 till date, FII & DII have increased their holding from 21% to 35%. The share price has more than doubles (from 70ish to 150ish) in the mean time.

SHP from Screener:

From Mar 2022 till date, FII & DII have increased their holding from 21% to 35%. The share price has more than doubles (from 70ish to 150ish) in the mean time.

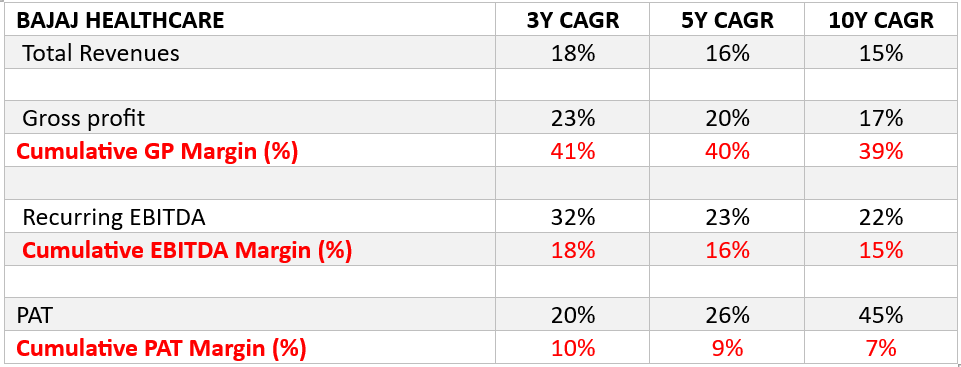

While EPS growth has slowed from 28%+ to just around 11% pre to post merger

June 2022-June 2023 to Sept 2022-Sept2023

The P/B ratio has fallen only from 3.8 to 3

Can we infer that more fall in share price will not be too much…

What could be the next support now that its continuously trading below the 50 and 200 DMAs…

Nevertheless, the company has done decently well in terms of Growth and Margin improvements:

Thanks for correcting me! So in that case, HDFC bank’s cost of fund should go up in future as there are going retail term deposit are growing at around 30% pa.

In the forthcoming approvals NCLT might take time.

Key one would be SEBI; i have notion that SEBI might not approve 6% Holdco discount. Might ask boards to revisit, since this is not in favor of IDFC Ltd’s shareholders.

Disc.: Invested in IDFC Ltd (32% of PF) hence heavily biased.

Thanks for the response. However and this is just from a small part of research, the entire so called FMEG and small FMEG space is extremely competitive. Look at sheer number of companies trying to build a B2C business here. 10 years back what was a 3-5 major competitors for every appliance/lighting system is now 10-15 competitors.

So While growth outlook appears rosy given higher units per home+ increase in number of homes i feel margins will be extemely thin. Would love your read on this.

Hello,

I hope you are able to access the presentation from the link above. The 8 megatrends are clearly listed out in the deck each having a separate section of its own.

I would recommend to open the presentation in a separate screen(if feasible) while watching the video session in parallel and pause to reflect on the data points in each slide and their implications. One needs to really absorb and connect the dots here.

Each cask will produce approx 170L after accounting for angel’s share. In Scotland this is generally 2-3% but in India because of the hot climate angel’s share is 10-15%.

GKW Ltd

MCap of this company (GKW Ltd) is only 425Cr. It is unclear if this deal will result in any revenues for this company.