Posts tagged Value Pickr

Techno electric engg ltd (17-10-2023)

I think, intent is to allow JV partner to decide Power supplier for RE . Now days, lot companies are buying stake in power generator to sign long term sheet.

Where can i find recording of the interview which you are sharing ?

Techno electric engg ltd (17-10-2023)

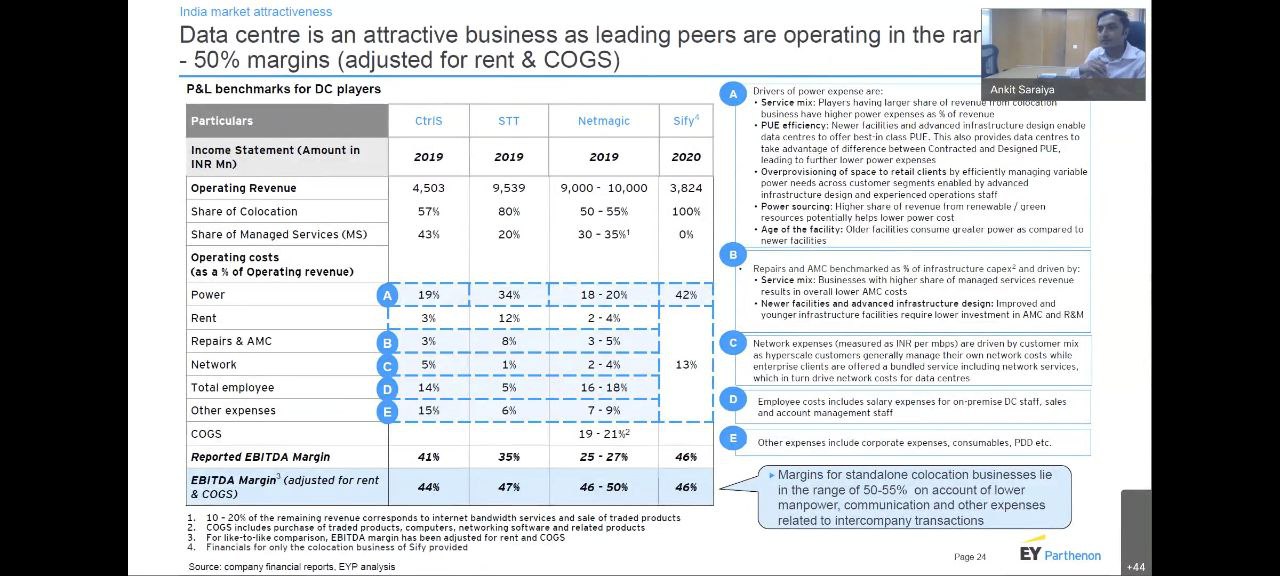

Power cost is the biggest running cost for a data centre ,earlier the management had said that they would be drawing power from their renewable assets for their Chennai data centre ,but now since they have sold off the wind business do they have any other renewable assets to supply power ?

Amit Singh Learning page (17-10-2023)

Kalyan Jewellers:

Company profile:

a) 161 Showrooms in India, 33 Showrooms in Middle east (Q1 Fy24 update)

b) 30 Years in business

c) 10779 employee strength

d) 5 countries, 22 States presence.

e) Jewelry Industry is changing from Unorganized to Organized currently around 35% has converted.

f) Wedding is 60% business share, Daily Wear- 30%, Fashion 10%

g) Rural India Demand and Ownership of gold jewelry is 60%

h) Indian Jewelry market, North-20%, East 15%, South 40%, West 25%

i) 70% of total gold share in India is Jewelry.

j) 6 Lakh SQft Showroom in India, 43L Sqft in ME.

k) FY23 ROCE 17.4%

l) Debt is ~29% of its current annual sales rev.

m) Total Number of Shares 103 Cr

n) Promoter holding has remained same from last 3 quarters and improve by .01% from the last 4th @ 60.55%.

Q1FY24

Salient Points

- Ramesh Kalyan Raman MD Consolidate rev growth 31%, PAT 23% (108 crores to INR 144 crores), Rev from India 34%, Operating momentum is good.

- Share of new customer in excess of 36% from last Quarter, Non South market 44% share up 35% from YoY,

- 16 new showroom opened, 10 new show rooms in plan out of 52 new showrooms in Non South Market was planned.

- Jammu opened 200th Showroom.

- Middle East rev 22%, Eid holiday driven sales

- Online platform Candere to launch omnichannel expansion strategy, 20 plus physical showrooms of Candere to be established during the next six months starting from August 2023.

- Divestment of the non-core assets which has been previously announced and we expect to conclude the transaction around the end of the current quarter. Selling its company owned Aircrafts and using the proceed ~Rs. 100 Cr net of Tax

- Candere is a Franchise Model FOCO. Cautious Approach, opening one store and letting it settle down and then going for the next.

- Eastern India to see more store opening, Jharkhand and Bihar

- Rev split between Plain gold jewellery 70% and Studded jewellery 30%

- COCO has 16% margin and FOCO has 8% margin.

- Next two years ESOPs will be given to Kalyan Jeweler employees till Store Manager level. ~400 employees. 30 Lakh shares pool is created for this ESOP.

- Ad expense as % of revenue will be around 2 to 2.2%.

- Same Store Sales Growth for ME is 21%, India business 15%.

- Studded Business comes with lesser margin, Non South market has more studded than Plain gold.

- Non South is FOCO model.

- Plan to reduce 15% debt. Debt is around Rs. 4295 Cr.

- Gold import which is being done from UAE under that Comprehensive Economic Partnership Agreement. 1% duty concession on import duty of Gold from UAE. KJ will take this benefit.

- Inventory is 15 to 20 Days in FOCO.

- Making charges used to be 25-30% which have dropped due to immense competition to 10-15%.

Q2 Earning Update:

- Consolidated growth of 27% YoY, Rev to be around Rs. 4410 Cr.

- PAT to be around Rs. 134 Cr, and EPS Rs. 1.3

- EPS for 4 passed Qtrs till Q2 FY24 to be around Rs. 4.83.

- Industry PE ratio is around 32 ( range of 91 PE of Titan to 32 PE of Senco). Kalyan Jewelers is having current PE of 62, CMP 295

- Debt is 28.4% of TTM FY24 @ Rs. 4295 Cr. This is to be kept in view as management intends to reduce it in Q2

- 13 new stores added in Q2 and 26 new stores FOCO to be added in non south market before Deepawali and 7 Candere stores.

- Candere stores recorded degrowth of ~15%. This is a concern as in last quarter it had loss of 6% from its buniess.

- As on 30th Sept 2023 Store count is 209.

Techno electric engg ltd (17-10-2023)

- Few pointers why i would delay the investment in this company

Data centre Chennai data centre commissioning pushed from sept23-dec23 to now march 24

data centre and AMI business is pulling the numbers down on a consol level

all the investments in data centres and AMI is not generating any revenue so mostly the kicker will come from q4 fy23 or maybe q1 fy24

but i guess the price may shoot before that if they get some strategic investor to do a JV or Buyout the data centre business

Techno can also be a good pick as it caters to all the themes which are currently in momentum namely power transmission,Smart meter,Data centre etc

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (17-10-2023)

They have already set it up

Breaking Ground: Gensol Electric Vehicles’ Futuristic Manufacturing Facility

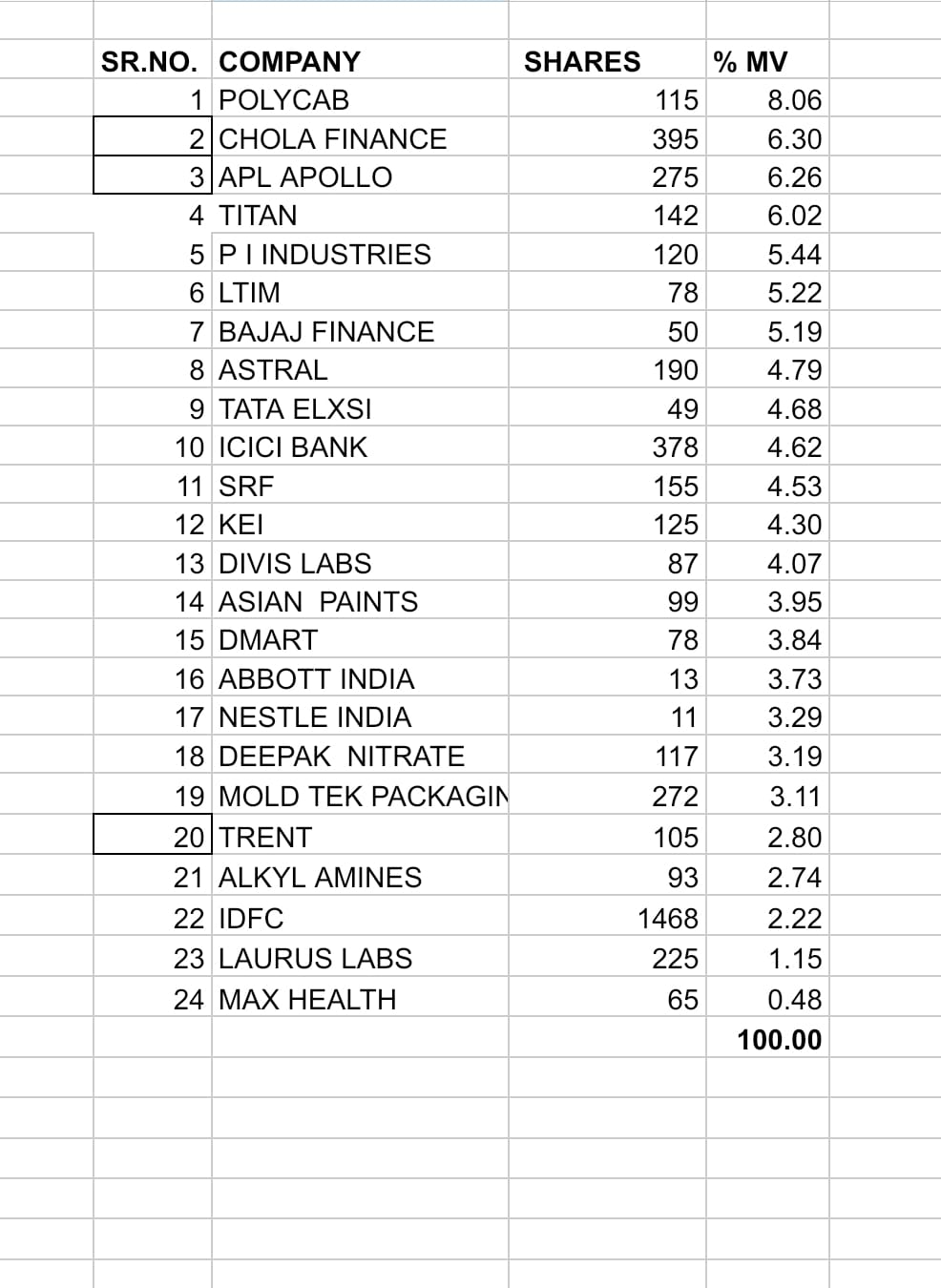

Mudit’s Portfolio (Passively Active) (17-10-2023)

Rationale Behind adding Max HealthCare :

- In healthcare I have 2 pharma companies Divis Labs and Abbott India ( Laurus Labs , I am going to sell soon), but I didnt have hospitals or diagnostics.

If you can notice, I want to reorient my portfolio towards consumer centric with more companies from B to C rather than B to B. Hence recent additions like IDFC, Trent, Nestle, Titan etc, So in healthcare I wanted to add Hospital company. - Hospital Industry is a capital intensive business , so it acts as a moat and strong entry barrier.

- Hospital business is very secular in nature, with complete disregard towards macroeconomic situations. Whether economy is in recession or in boom, if someone needs dialysis, once in a week, he has to do it, no matter what. Bed capacity , GDP expenditure on health is very low , so long runway for growth. there are 10 more reasons for visible growth in this sector…But I know you get it.

- Why only Max health? why not Apollo or Narayana or Rainbow?

Max Health has highest revenue per occupied bed and also the occupancy rate is high compared to peers. In hospital business growth comes from acquiring other famous and matured hospitals or taking on lease Trust hospitals and I feel Max Person is good at this game . He has proved it many times, Their expansion strategy is aggressive compared to others. Being secular nature of business, this will also give stability to my portfolio. Again there are many reasons…But this much is enough. I am not a “Baal ki khaal” person. If something appears approximately correct, not precisely correct, I go ahead with it. After all business lies not only in screener… There are many qualitative non-screener attributes to each business… Open to critical opinions as always.