No mutual fund has any holding in this company even though it is above 1000 cr market cap. QIP failed as Institutions do not want to own the company. Promoters buying from open market to show their confidence in the comapny. But i suspect something fishy here, i might as well be wrong. But in any market conditions if there is growth in the company institutions are the first one to smell the same and line up to buy the shares. Here i think promoters are just circular buying from their own undeclared pseudo promoter accounts. Again I might as well be wrong.

Posts tagged Value Pickr

HDFC Asset Management Company (16-10-2023)

Auto anciliaries business needs innovation and seperate key competence which OEM may find difficult to pursue along with their core business…also auto anciliaries arenmot dependent on regulations from gov. etc.

CAMS type business imo needs no drastic innovation, R&D and its just transactional and dependent on regulations as well (directly & indirectly)

Cams type business is not comparable to auto anciliaries in this context as well…

we cannot say for sure that growth in amcs will always result in growth of transactional companies that serve them…any change in regulations can even put a question mark on existence of such businesses as well or the way the operate and make profits…

Above only my thoughts and i can be wrong in my assessments…not a biy/sell recommendation.

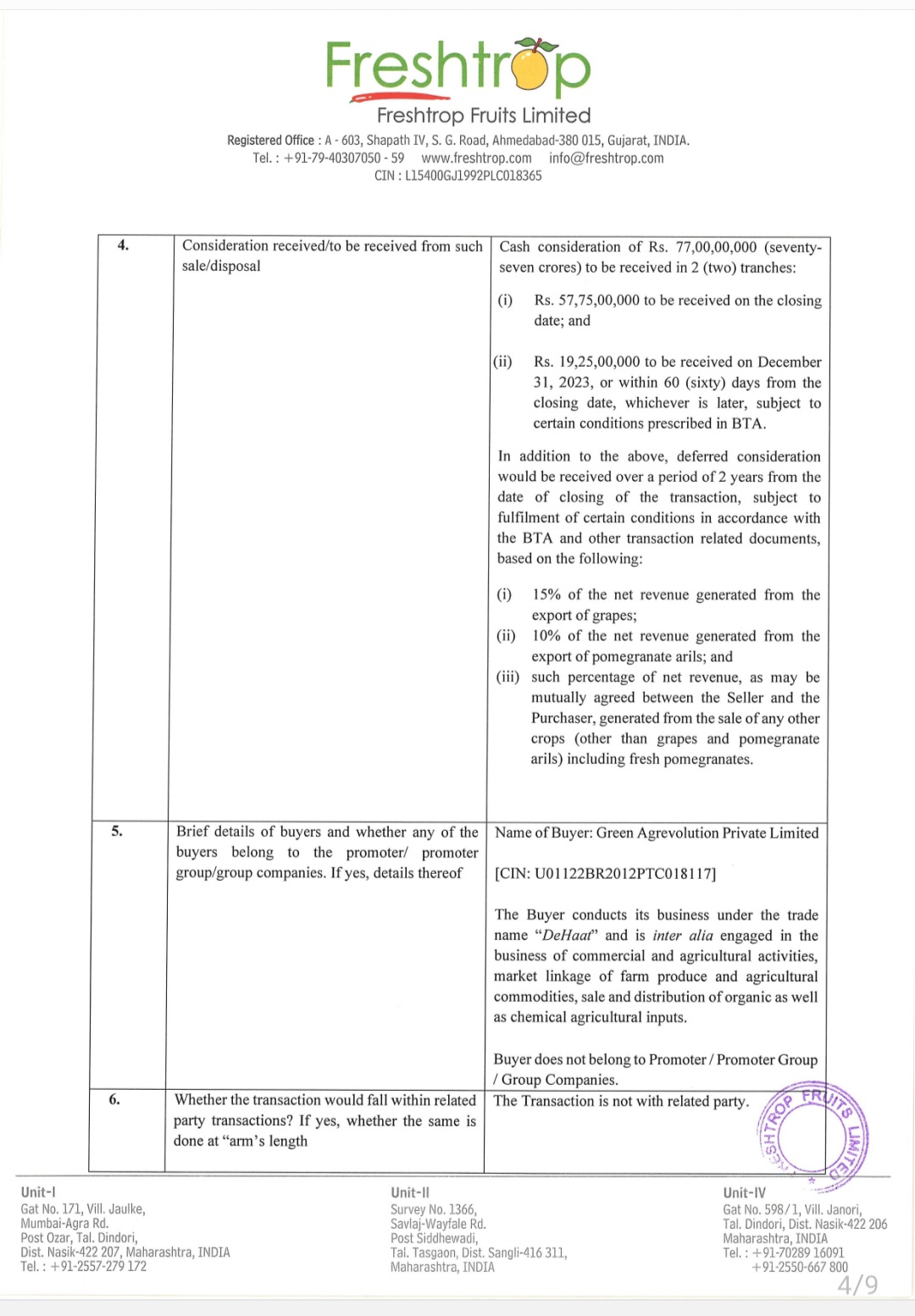

Freshtrop Fruits Ltd (16-10-2023)

Freshtrop Fruits

Sells fresh fruit business for 77 Cr + additional deferred consideration for 2 years

It will be used in investment of food processing business & return surplus funds to shareholders

Reason for sell: No growth, high investment & long gestation period, restrictions in farming.

Sell valuation is not very encouraging in my view.

About 100 Cr. ( including deferred revenue ).

However, they sold it out of frustration of poor performance & restrictions and want to improve & focus on food processing business. – Good initiative for a long term plan.

Disc: Invested

Investor Grievance Mechanism (16-10-2023)

I have Demat account in ICICI direct. They have started scheme of Upstream .

Up Streaming of funds means debiting the peak margin (Highest margin created anytime during the day) and pay-in obligation from client’s account and upstream the funds to Clearing Corporations (CC). The movement of fund would be customer depositing funds in ICICI Up Streaming Client Nodal Bank Account- USCNBA), from their money will move to Broker’s Settlement account and then to Clearing Corporation. That means, the funds will be debited from the clients account and same will be Up Streamed on the same day to Clearing Corporation within the given cut off time. The Cut-off time given by CC for the same is 7.00 PM.

This means ICICI direct will block money for any Buy order with target price if NOT executed for one Night for weekdays and 2 days for weekend days.

As I understand, this scheme is only for ICICI direct and Not for other brokers.

Following is SEBI circular.

V. Upstreaming of funds: Funds received on a given day by SBs shall be transferred to CMs, and by CMs to the CC any time during the day, but not later than the respective cutoff times. The respective cutoff times for upstreaming are as follow: Sr. No. Particular Cutoff time 1 CM upstreaming cutoff time To be decided by CC – not earlier than 6:00 PM 2 SB upstreaming cutoff time To be decided by CM – not earlier than 1 hour prior to CM upstreaming cutoff time

Read more at: SEBI Circular: Upstreaming Clients’ Funds – Implications & Guidelines

Ultimately this is client money and what is right to ICICI direct to block money. Is it legal and SEBI approved?

Request your opinion from seniors whether this is OK

Selan Oil Exploration (16-10-2023)

A good set of results. Production from Karjisan has revived. During Q1’24 guided to 800 boepd production and they have achieved that by the end of Q2’24.

52 week highs and all time highs strategy (16-10-2023)

UPDATE: MSTC 316-530, a new ATH…

- An excellent base breakout seen in MSTC. Base formed since October 2021.

- A small pennant type pattern seen just before breakout as well.

Safe to assume a bullish bias ahead…

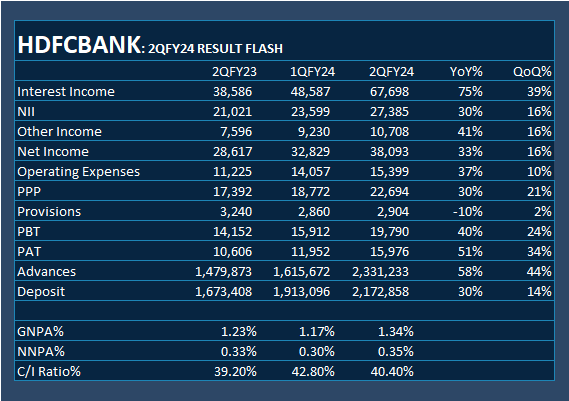

HDFC Bank- we understand your world (16-10-2023)

Q2FY23-24 QUARTERLY RESULTS

FINANCIAL

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (16-10-2023)

I had a conversation with the head of co-lending at a large PSU bank. They have interacted with Ugro daily for the last two years.

Key pointers from the discussion:

On Co-Lending

-

Co lending uptake from PSU banks has been slow due to skepticism about the MSME segment in the wake of covid. Finally after the second wave resolved, co lending has picked up to an industry size of around 25,000 Cr. today. The formal landscape is around 400,000 Cr. and can be easily reached in 10-15 years.

-

There is a split between private and public sector banks on co-lending. Public sector banks want to partner with large NBFCs and are keen to have a social impact: formalisation of credit, bring more people within the purview of a bank, without compromising on asset quality. Private banks in comparison want to partner with small niche NBFCs, where they see co lending as a way to create a product, and lend to a segment they haven’t already tapped (example: Trucap and HDFC).

-

Banks have daily reviews of portfolio quality on co lending, and set collection efficiency targets for NBFCs, and have close discussions on all aspects of the book frequently. If something isn’t right, they slow down. Conversely, if things work, they will scale relationships.

On Ugro and the Competitive Landscape

-

Tech integration is extremely important in co-lending. RBI regulations require co-lending to be done on the same day as disbursals. This cannot be done by manual entries at scale. Ugro very early understood this and were ready with an API stack, middleware and a digital platform. They were an early mover/leader in the space, and this alone is not an advantage today, as everyone else has had to invest and build to get to the same stage.

-

Bank and NBFC have to simultaneously underwrite the loan. NBFCs have proprietary scorecard models, and do not disclose the workings to banks. Ugro’s approval ratings were very low in the early stages of the relationship. Today, the approval ratings under co-lending are up 8x from the early days. Rejections are due to a difference in interpretation of policy, and 70% of loans sent from Ugro’s side are accepted by the bank, and is a great number in the bank’s eyes.

-

There are several things Ugro does right in the bank’s eyes.

a. Relationship was slow in the early days until bank got comfort in Ugro’s collection mechanism and quality of the book that was passed on. Did secured lending initially, but now have started to do unsecured.

b. Middle management is very good, no one has left in the last couple of years. This keeps the bank happy, as there is continuity in working relationships. They have brought on more quality people, and have become more stringent with regulations and underwriting.

c. A loan that is sourced doesn’t differentiate which bank it goes to. Ugro is very good with knowing what exactly the bank wants, and sending them the correct loans for their requirements.

d. There is no USP today on a product / segment. The market is very large and can accomodate lots of players. Working culture is more important to the bank than a lot of things investors look for like USP. There is no complaint with Ugro at the moment, no challenges and Ugro is upfront in their discussions with the bank. They constantly ask what kinds of expectations and ratios the bank wants in their secured/unsecured book. Softer USPs are the ability to bring the right pockets of people into formal credit.

e. Religare was a non issue. Regulators have no complaints, company has managed to raise a lot of capital from a good investor base. Management is known in the industry and is capable.

f. Another highlight is the digital collections system, where collections are based on NACH/e-NACH, and documents are digitally signed without physical copies. Cash collection has a lot of compliance risk. Peers like Paisalo have fallen behind in this respect.

g. Co-lending discussions start with an expected credit cost of the product, and then targets are calculated in reverse. As an example (not actual figures), if you are pricing in 5-7% stage 2 NPAs, then collection efficiency targets are around 93-94% initially. These are then recalculated on the product and life cycle.

IIFL and SBFC were also discussed as really good names in the industry. SBFC was called an excellent company. Capri Global has poached good people from IIFL and has built a book quickly.

Lastly, by regulation, direct assignment can be classified as co-lending. A lot of PSU banks talk of scaling the co lending book, but it’s DA that gets scaled, not true co-lending. It’s important to focus on this distinction amongst stakeholders in the future.

Disclosure: invested and biased. These conversations rarely are made public, and I’d like to give back to the community.

Avenue Supermart: a compounding machine? (16-10-2023)

The taxation in last years quarter was lower as compared to their average taxation rate. Since that got moderated now, we got a lower PAT number. Cumulatively, margin contraction is only a negative. Profits will grow once the recent stores that opened will mature in next 2 years. But improvement in their product mix will be even more important for profit growth.