-

TCS saw a net reduction of 6,333 employees in the second quarter of FY24, while in the previous quarter, they added 523 employees.

TCS saw a net reduction of 6,333 employees in the second quarter of FY24, while in the previous quarter, they added 523 employees. -

Chief Human Resources Officer Milind Lakkad credited TCS’s strategy of hiring and training freshers for the decline in headcount, highlighting increased productivity.

Chief Human Resources Officer Milind Lakkad credited TCS’s strategy of hiring and training freshers for the decline in headcount, highlighting increased productivity. -

In the first quarter of FY24, TCS was the only major IT company to increase its headcount, while others experienced declines due to the uncertain economic climate.

In the first quarter of FY24, TCS was the only major IT company to increase its headcount, while others experienced declines due to the uncertain economic climate. -

TCS’s headcount as of September 30, 2023, stood at 608,985 employees.

-

Attrition decreased to 14.9 percent on a last-twelve-month basis, down from the previous quarter’s 17.8 percent.

Attrition decreased to 14.9 percent on a last-twelve-month basis, down from the previous quarter’s 17.8 percent. -

Industry-wide, net additions and hiring have slowed, not limited to TCS.

-

TCS faced delays in onboarding laterals for several months.

TCS faced delays in onboarding laterals for several months. -

In the previous quarter, TCS provided salary hikes, offering 12-15 percent increases to exceptional performers and initiating a promotions cycle.

In the previous quarter, TCS provided salary hikes, offering 12-15 percent increases to exceptional performers and initiating a promotions cycle.

Posts tagged Value Pickr

TCS opportunity (11-10-2023)

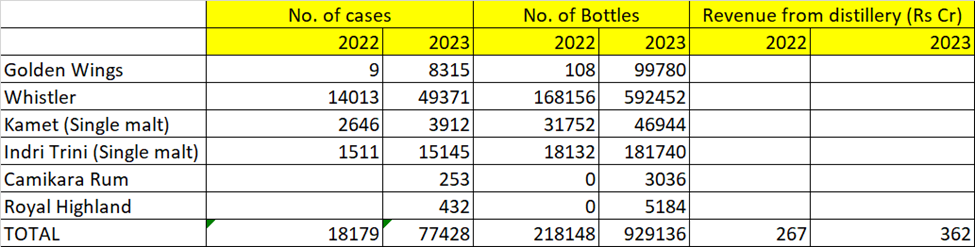

Piccadily Agro Industries Ltd (11-10-2023)

Any idea on capacity utilization across SKUs?

As per two years annual reports overall production has gone up multifold however revenue has gone up by by 40%. Below are the SKU wise numbers and corresponding revenue.

Buyback Decision – NTPC/TCS and all others for retail investors (11-10-2023)

Any Calculation for TCS Buyback 2023?

Risk Reward & Profit if acceptance ratio around 100%.

CMP 3,610

Buyback Price 4150

Buyback Size 17,000 Crore

Mazda Ltd – Sheer Undervaluation? (11-10-2023)

Also Clientelle information is not provided.

Investing Basics – Feel free to ask the most basic questions (11-10-2023)

hi,

How to get sector P/E in a particular case?

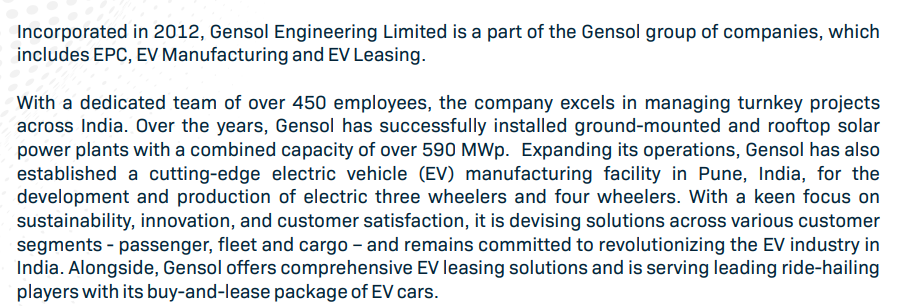

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (11-10-2023)

Hello Dear Forum members,

Over the last couple of years, I have derived immense value from the contributors of ValuePickr forum and today I am taking my first step from being a reader to a contributor. ![]()

I’ve been investing for the good part of last 7-8 years (only) and therefore this article is to invite the VP community to collaborate and fill my blind-spots and make it worthwhile for all reading this piece.

The company I am referring to is in the Solar EPC (Engineering, Procurement and Construction), Car Leasing and EV manufacturing space and is listed on the main board of NSE and BSE as Gensol Engineering (NSE: GENSOL and BSE: 542851)

About the Promoters:

The company is Promoted by Anmol Singh Jaggi (21.73%) and Puneet Singh Jaggi (19.07%) and Gensol Ventures Pvt. Ltd. (23.87%). Anmol and Puneeth (brothers) founded the Gensol Group in 2007 and have led it to today being a large service-oriented company with a team of 600 engineers & technicians. Together the Promoters family holds ~64.67% of the company. (This is after a recent QIP and equity dilution of ~6.6% in Q3, FY23)

Profile of Promoters:

Anmol – Anmol Jaggi | LinkedIn

Puneet – Puneet Jaggi | LinkedIn

Incidentally, Anmol is also a founder of Electric Cab hailing company, BluSmart Mobility, which is rapidly gaining market share in Tier 1 cities like Delhi and Bangalore. (To my best knowledge Gensol Engineering does not have any equity in BluSmart, however it stands to benefit from its EV leasing business to BluSmart, which I will talk about little later).

Apart From BluSmart, Anmol is also the promoter of Matrix Gas and Renewables Ltd., which is a gas aggregator in India with a portfolio of rLNG and domestic gas. (The promoters plan to list Matrix Gas soon and DRHP has already been filed earlier this year).

Talking about Puneet, he is also the founder of Prescinto Technologies Private Limited which is a AI-powered monitoring, analytics platform (which augments the automation of maintenance of their Solar EPC projects).

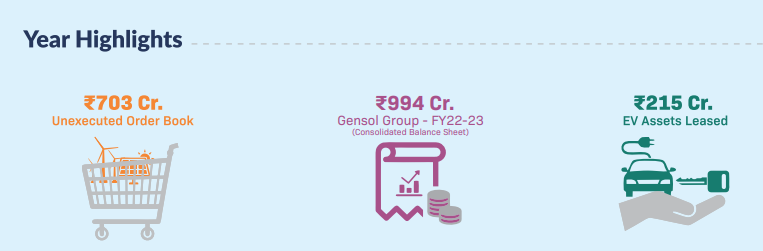

About the Business: (Snippets from AY 2023)

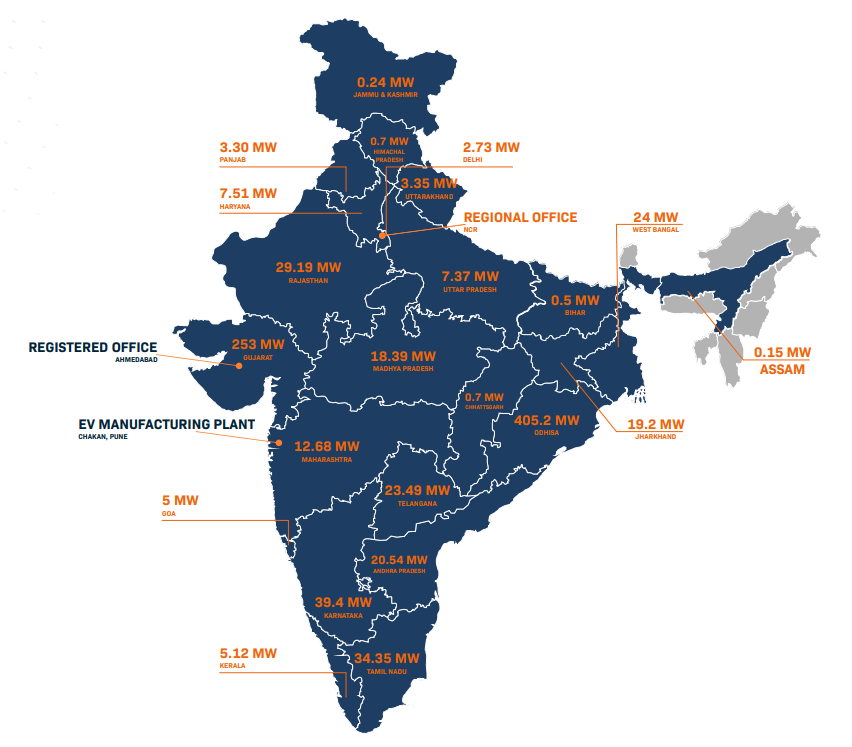

Geographical Presence:

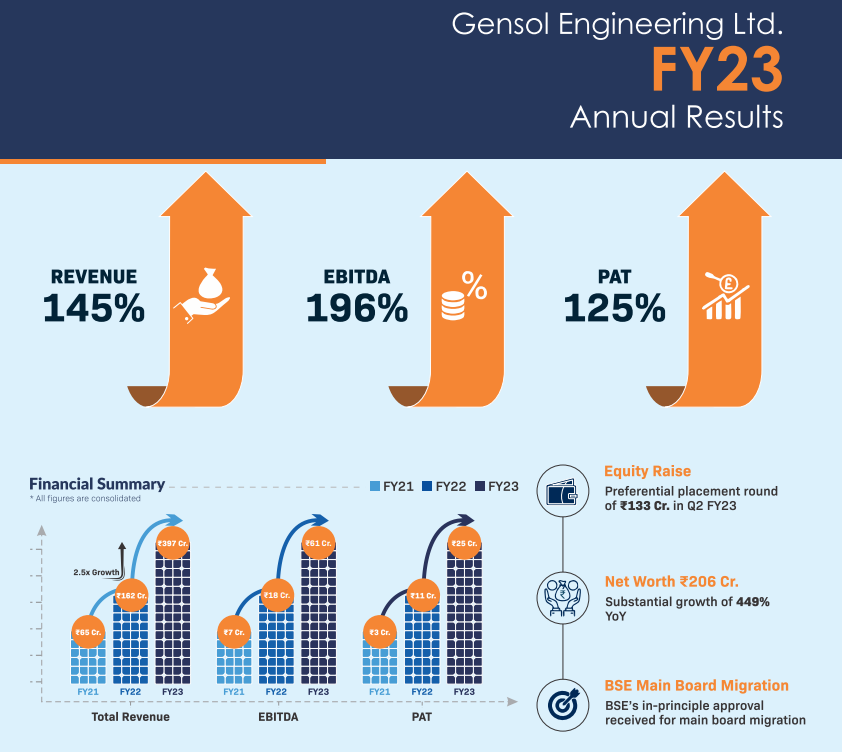

Strong YoY Growth in Business Performance:

Decent Order Book and Assets:

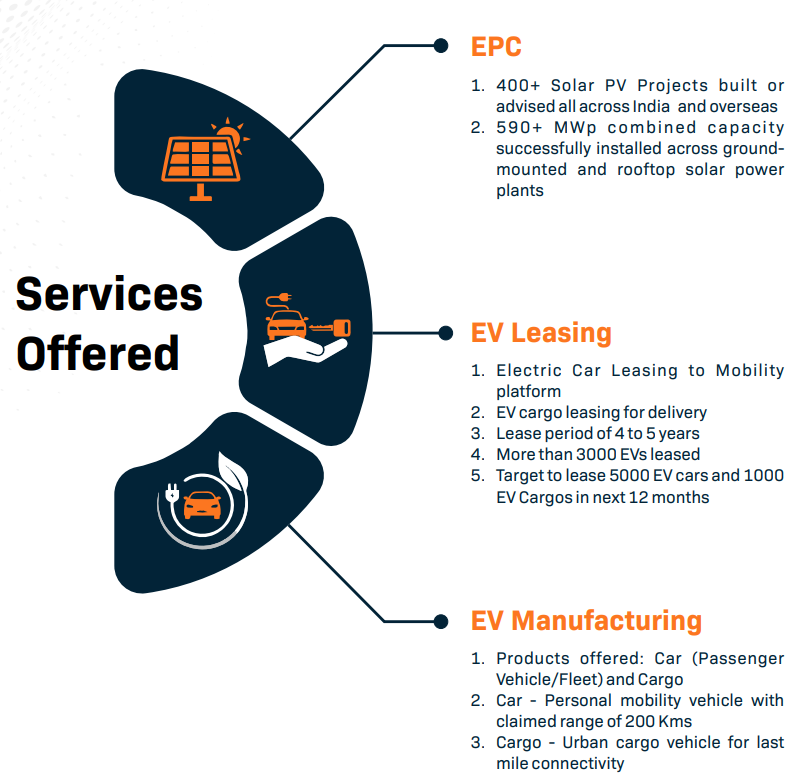

Business Segments:

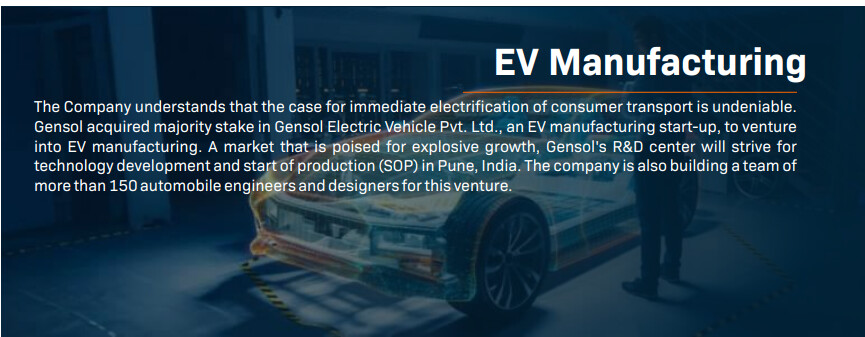

The company has been building upon its ambitions in EV manufacturing and has set up a comprehensive EV manufacturing plant in plant in Chakan, Pune.

Here is a recently released video of their EV plant – Breaking Ground: Gensol Electric Vehicles’ Futuristic Manufacturing Facility – YouTube

Alongside, it has been consistently winning Solar EPC Orders in India and Abroad

Link – Gensol secures Solar EPC Projects in Dubai, shares rise – The Hindu BusinessLine

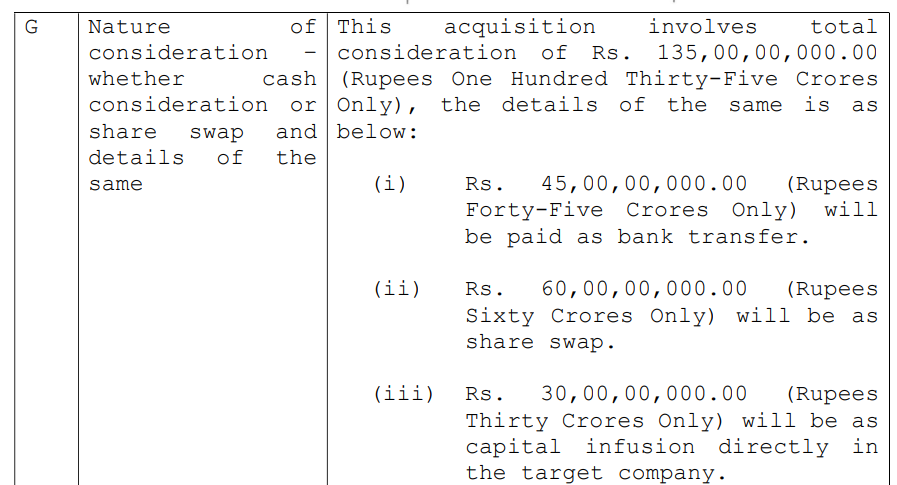

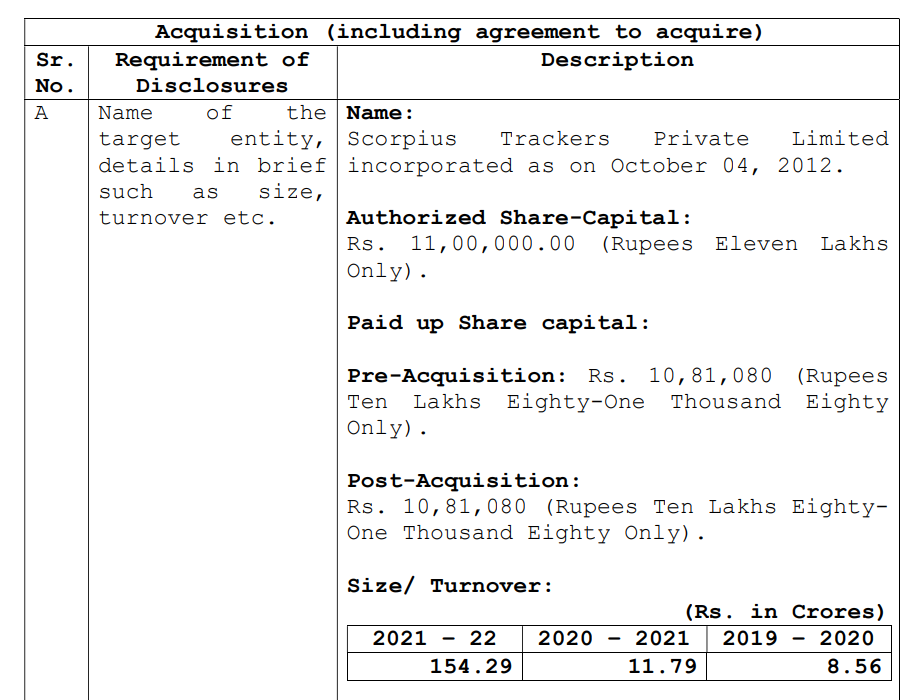

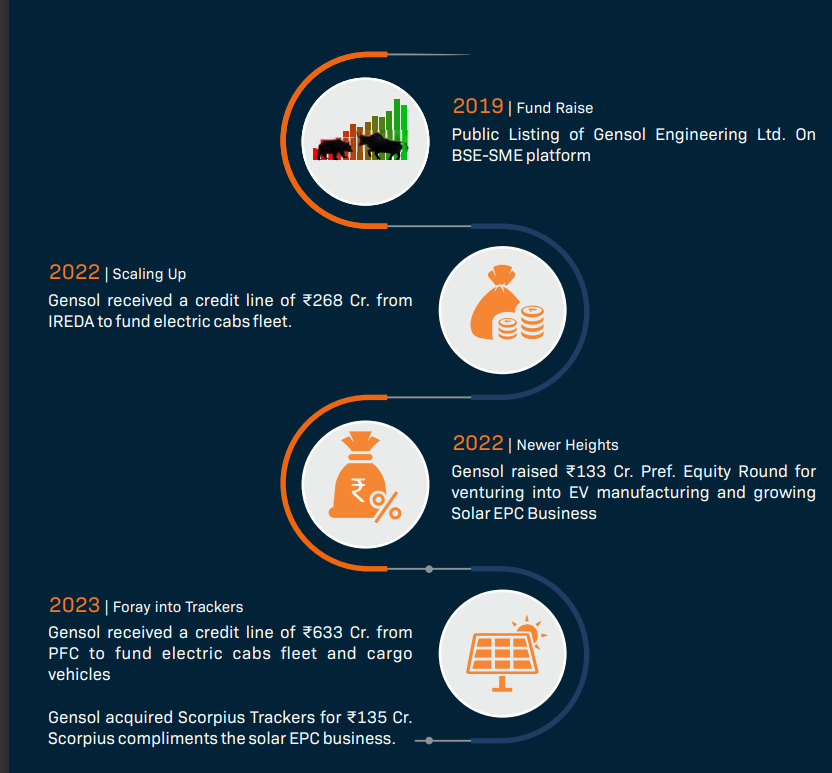

Earlier this year the promoters acquired a Solar EPC tracking company, Scorpius Trackers for price of 135 Cr.

Below are the details of how this acquisition was funded:

As per company disclosures made on acquisition, Scorpius trackers had a topline of 154 Cr. in FY 21-22.

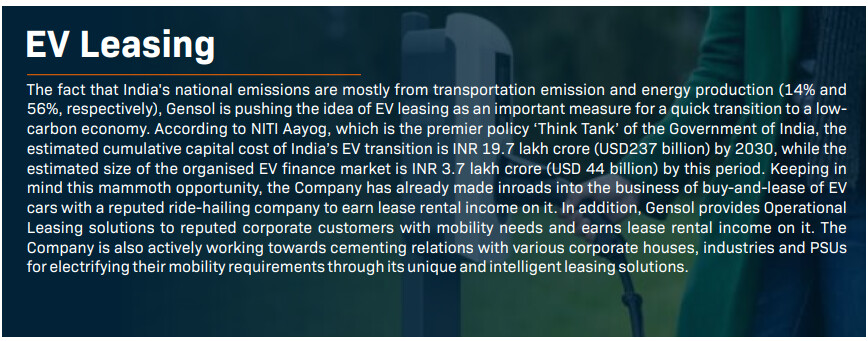

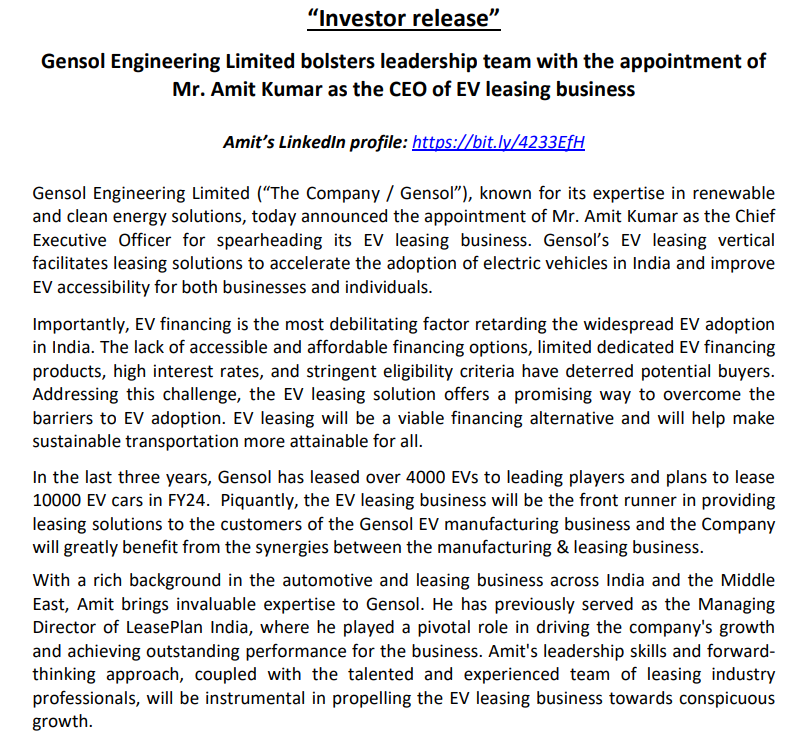

On the EV Leasing side, the company is growing its leasing contracts at a decent pace and has also hired a CEO to support this business vertical:

EV Business CEO Profile: Amit Kumarr | LinkedIn

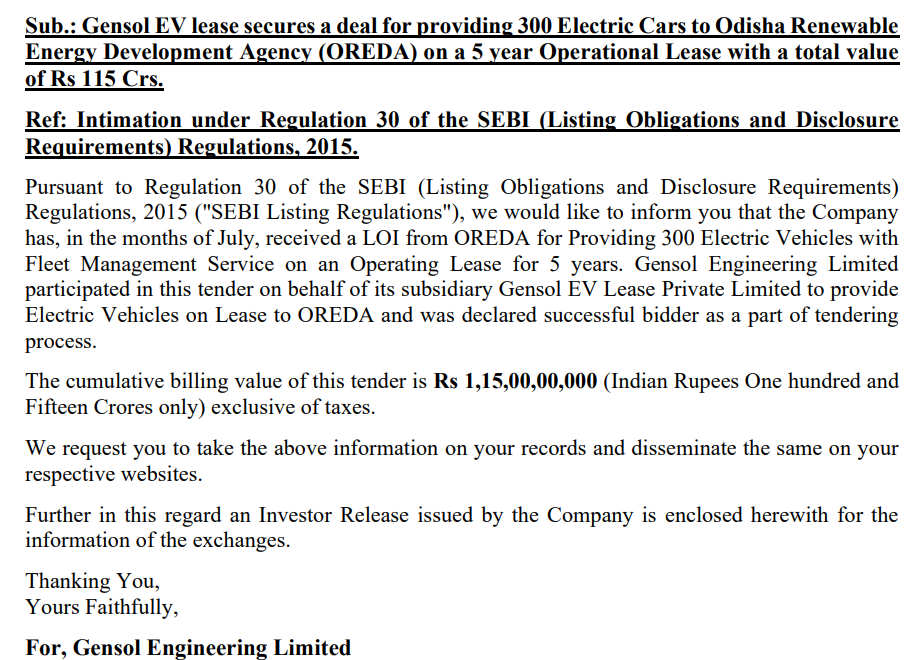

Recently they had a big win in EV leasing business:

The company has been pulling all levers to keep them lush with liquidity

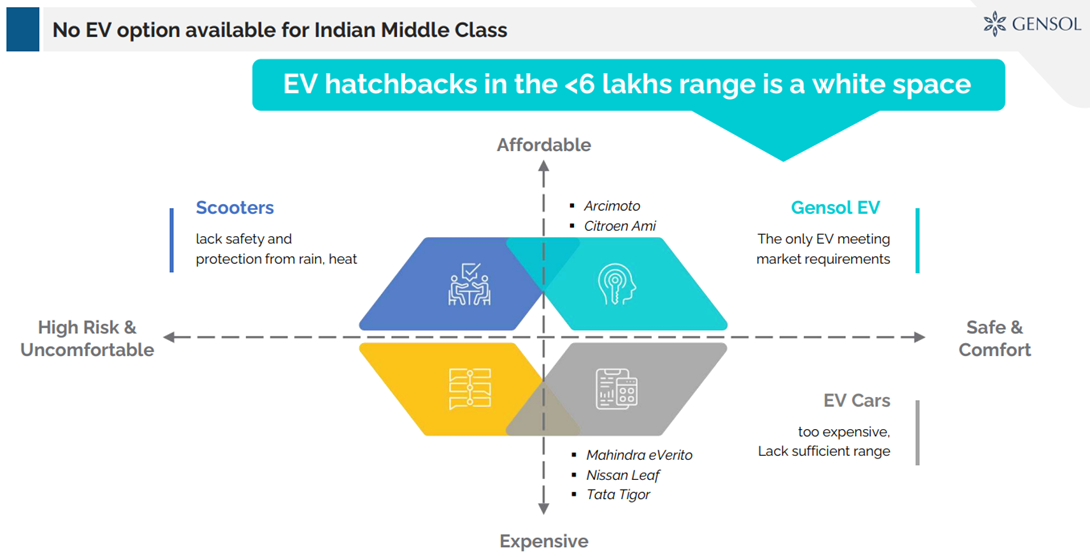

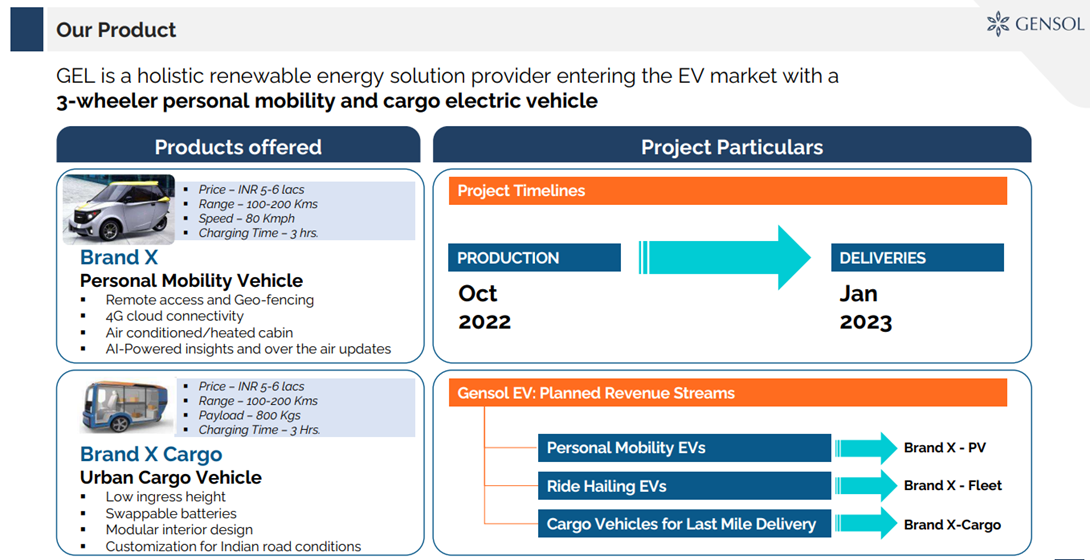

Some more details of their EV brand positioning, which they want to target in the affordable segment:

Also, they have plans for manufactoring Cargo and fleet EVs

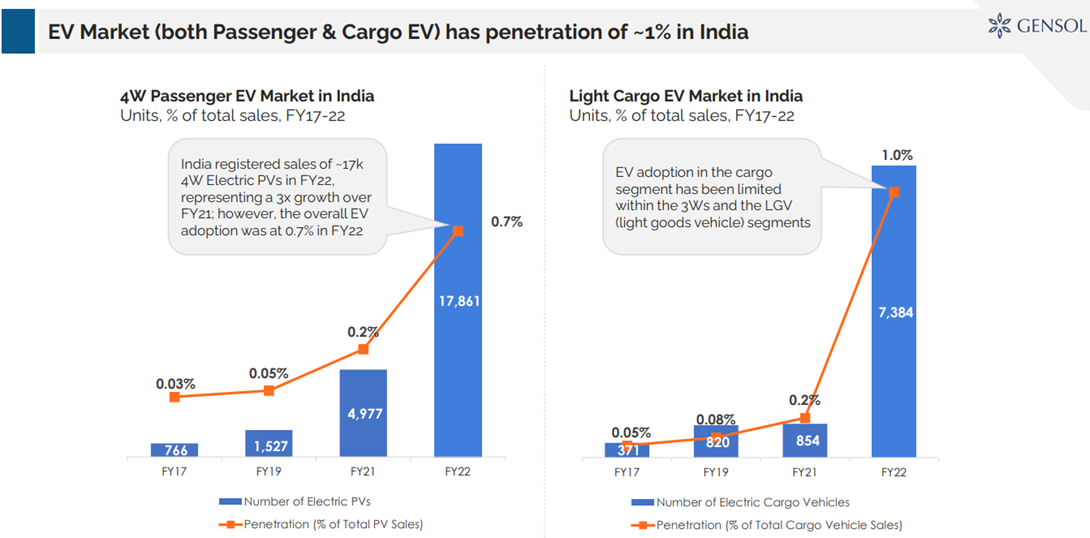

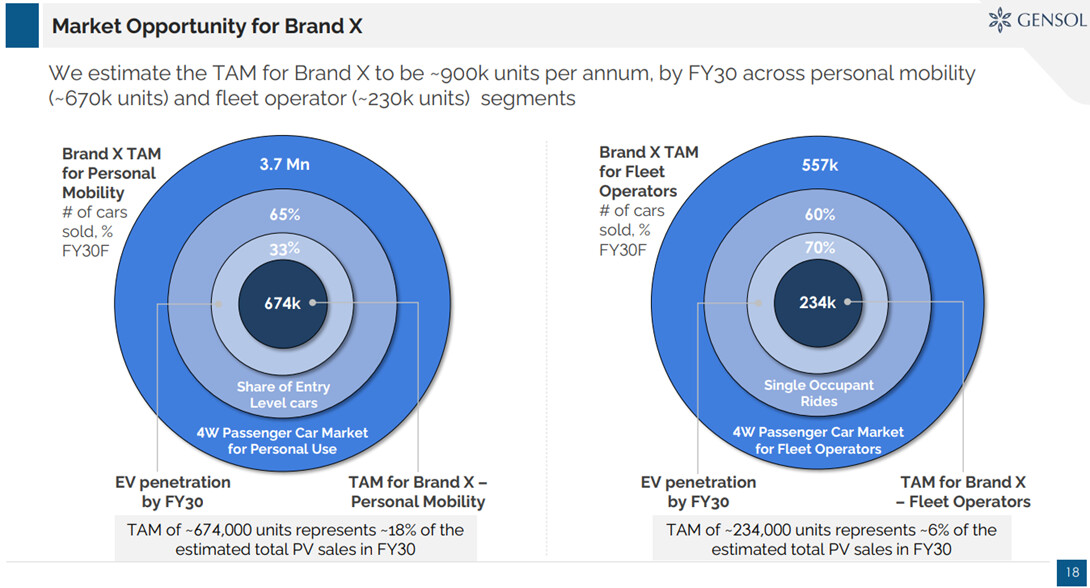

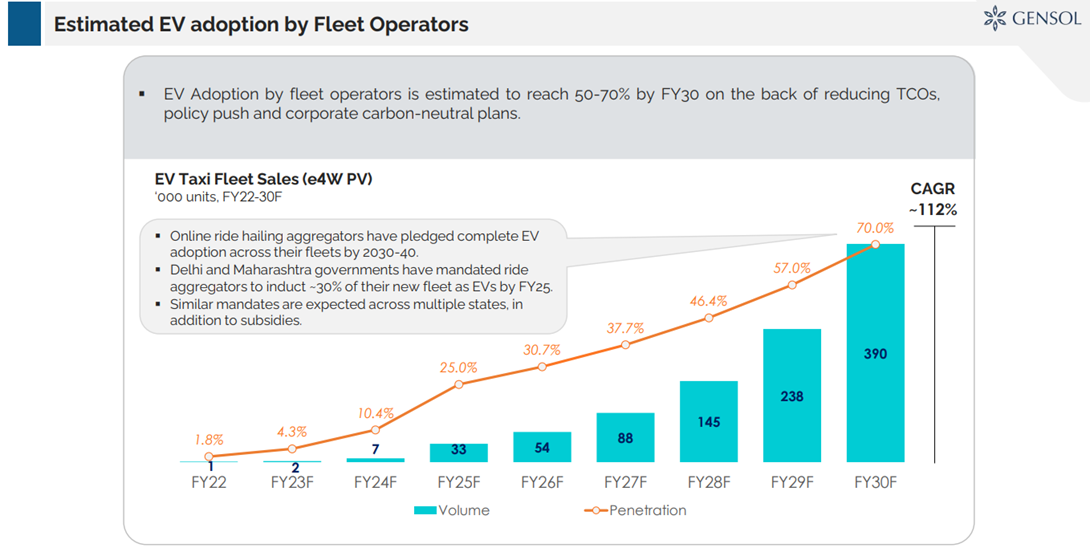

Market opportunity for their EV brand positioning: (We’ve all seen a lot of these charts and projections before, but bear with me)

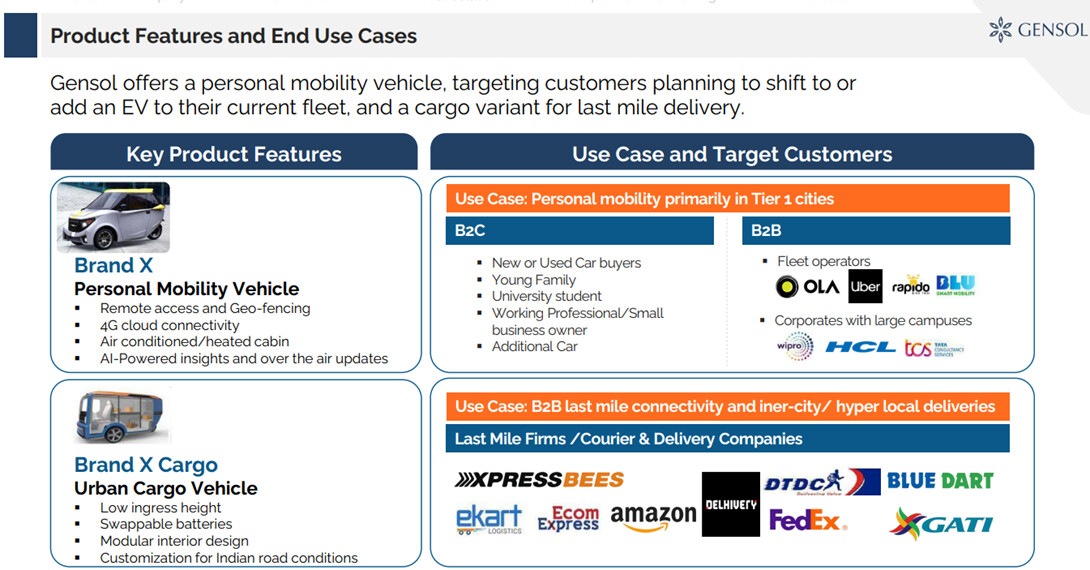

Some more insights into their EV products:

Some more end-use case of their EV products:

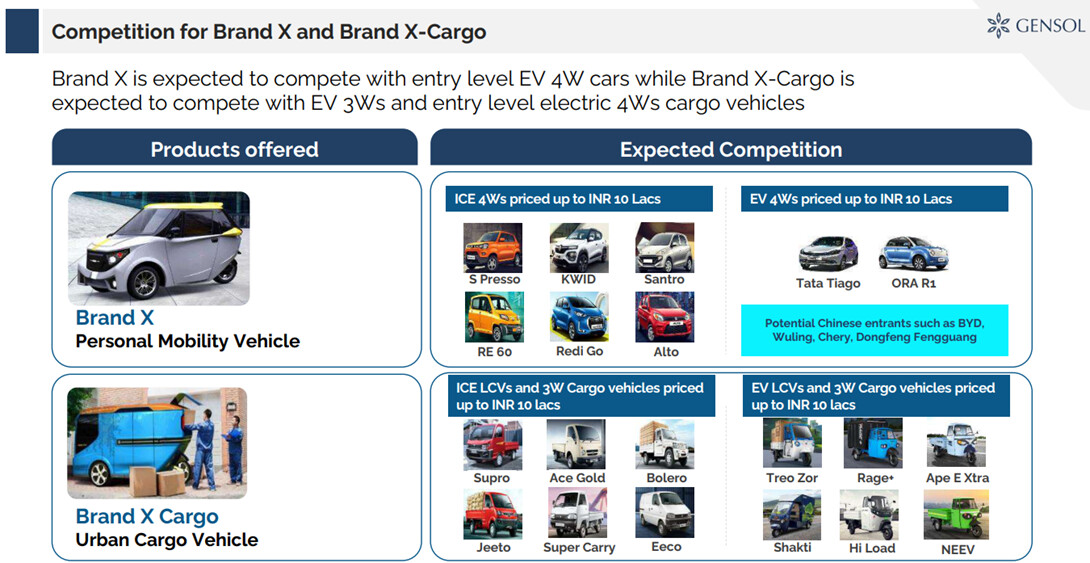

Competitive landscape for their EV products:

Coming back to the overall Business, the metrics look decent:

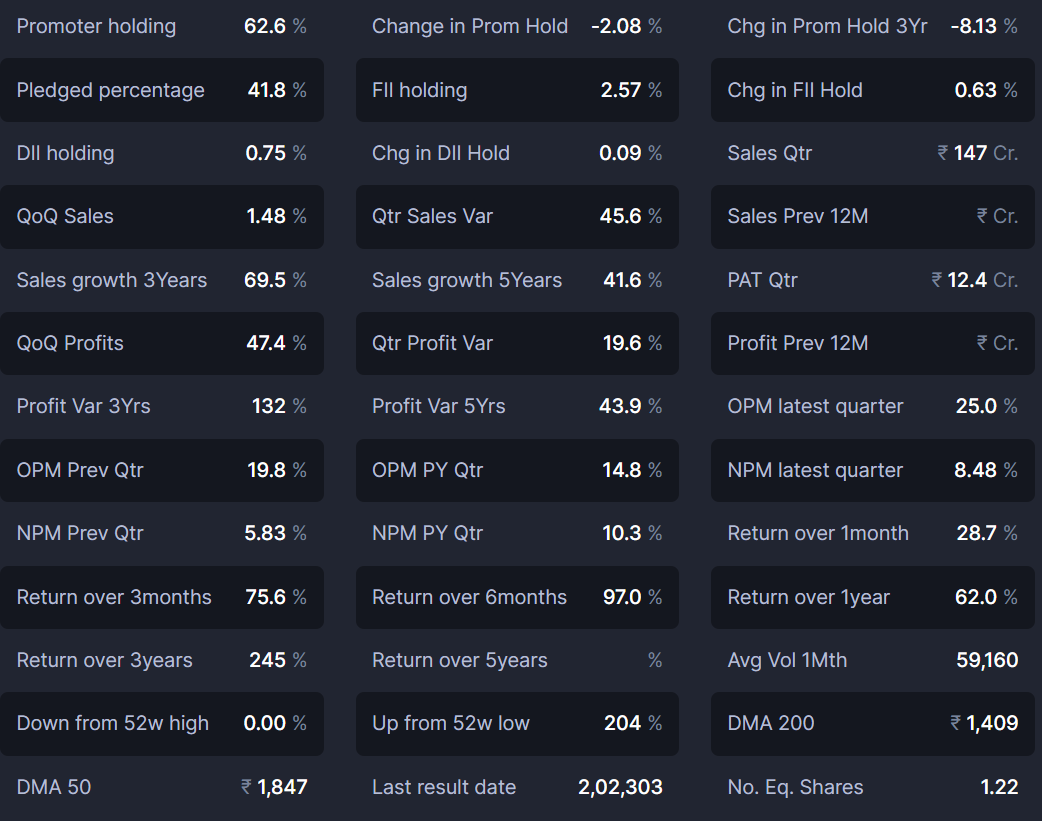

21% ROE and 12.4% ROCE

2.5 times Debt to Equity with 3.22 times Interest coverage

285 cr cash and 194 cr reserves

Sales growing at a 3Y CAGR of 69% and PAT growing at a 3Y CAGR of 132%

Operating margin is expanding – 14.8% one year back > 19.8% one quarter back > 25% in latest quarter (which shows the company has some operating leverage playing out).

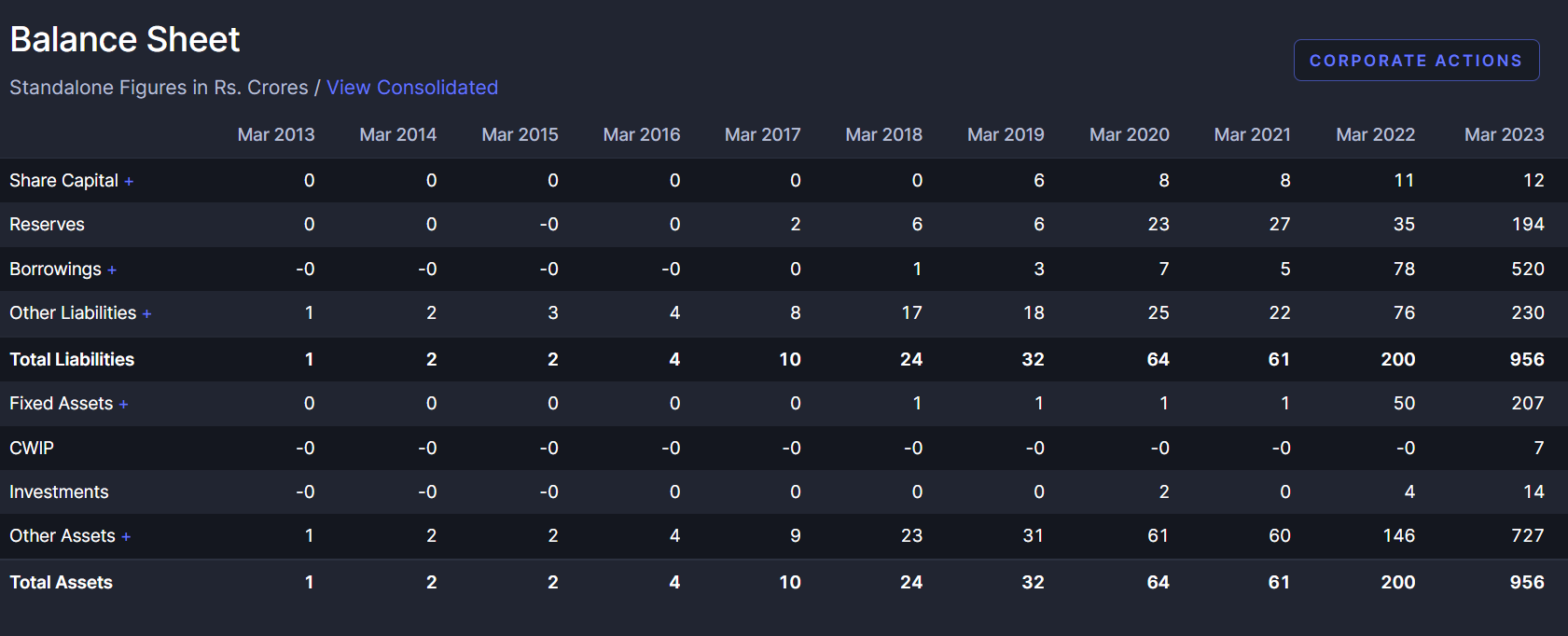

Company has recently taken a lot of debt on balance sheet to fuel its ambitious plans. (This is a key risk)

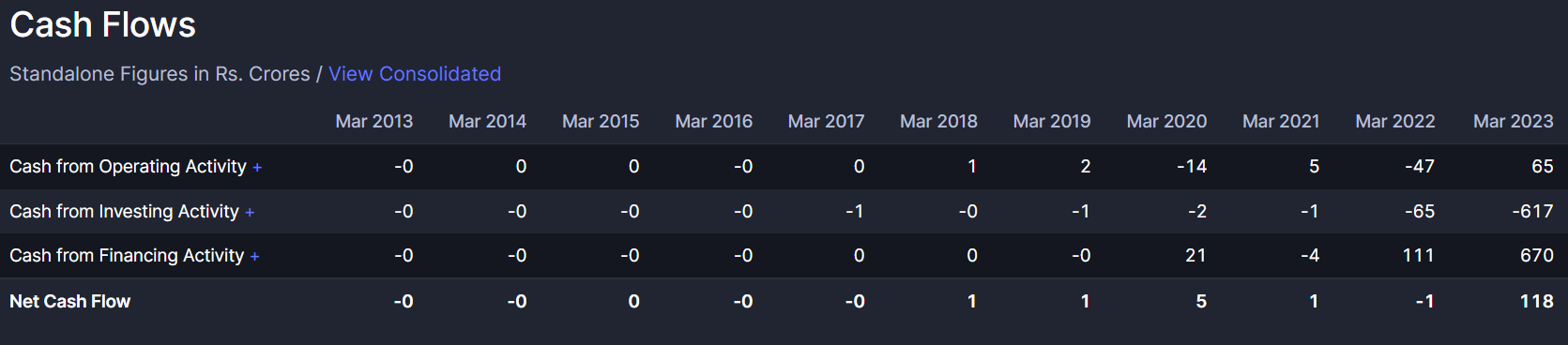

Company has decent and positive cash flows compared to reported PAT.

Promoter holding is decent and the dilution is because of QIP last year:

Coming to the last point in the analysis. Price and Valuation:

The stock has taken a liking for stratosphere and has been going up parabolically which makes it look expensive for entry.

I have personally invested in this company when listed in SME board and managed to hold on for multi-bagger returns. However, I strongly feel this company has a long road ahead and Im not cashing out yet.

Here are the triggers which can work well for the company:

- Acquisitions of Scorpius tracker leading to immediate topline growth as well as strategic advantage of Maintenance billing in EPC contracts (Solar Panel maintenance)

- EV leasing business growing multi-fold guided by huge market opportunity for cab fleets which are migrating from ICE to EV, along with arm’s length requirement of BluSmart mobility.

- EV Manufacturing striking a product market fit (both in PV and CV), leading to huge upside potential.

- Global expansion of EPC business (Dubai EPC order was an example of EPC opportunities outside the country).

Let’s talk about risks:

- The company competes in a crowded market, be it EPC, EV leasing or EV manufacturing where everyone wants to take a piece of the cake in India’s energy transition story.

- The current valuations fully price the euphoria and growth potential of this sunrise industry and any disappointments, delays, regulatory or Govt led dampeners (PLI scheme withdrawal, etc.) can significantly de-rate the company’s valuations.

- The company has leveraged (taken debt) to the point that its execution does not have much room for mistakes. Manufacturing EVs is capital-intensive and in a world where the technology and consumer demand is rapidly evolving, a product market mis-fit may quickly suck the liquidity out of the company.

Happy to hear if others are tracking this company and any feedback is welcome.

Disclosure: Invested. Will add on dips.

Mazda Ltd – Sheer Undervaluation? (11-10-2023)

FIIs again entering into the business

Zoom webinar on stage investing (11-10-2023)

please add me… kubssk@gmail.com

Pratik’s Portfolio – Review (11-10-2023)

Hi Pratik , I am not pro into valuation but do have some basic knowledge. I have posted one query in KPI Green energy thread that company Free Cash flow has been negative since last 5 years. I like the sales and profit they making but just because negative free cash flow I would like to monitor it further. Also no guidance on that given by management. I am also not sure if I am over concern about FCF.

Kirloskar brothers – 100 years old fluid engineering gorilla (11-10-2023)

Very nice detailed information on every business jn differnt sector nd different countries.