Some of my observations, not posting my opinion

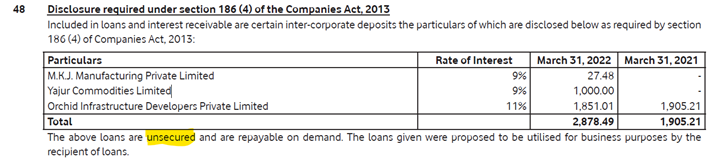

• Unsecured loans

• Promoter initiated Pledge again in March 2023:

• Salary of Key managerial personnel

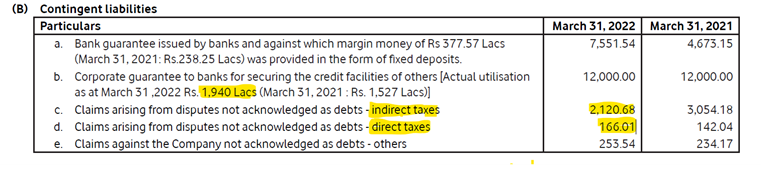

Corporate guarantee

Cash conversion cycle

Disclosure: not invested

Some of my observations, not posting my opinion

• Unsecured loans

• Promoter initiated Pledge again in March 2023:

• Salary of Key managerial personnel

Corporate guarantee

Cash conversion cycle

Disclosure: not invested

Products and Services [ source – screener]

The Co. is engaged in manufacturing and sale of all types of marine and industrial electrical & electronic components like switch-gears, control-gears etc. It is also engaged in the renewable energy sector, specifically solar. It also provides services like designing, fabricating etc. for all types of electrical & electronic installations in India and abroad and undertake annual maintenance contracts. [1]

Revenue Split

Electricals & Electronics– 99% in FY22 vs 74% in FY18

Solar– 1% in FY22 vs 26% in FY18 [2] [3]

Geographic Split FY22

India – 82%

Outside India – 18% [2]

+ve points [ from credit report ICRA]

Healthy order book position – The company’s order book position improved to ~Rs. 500 crore as on December 27, 2022 from

~Rs. 407 crore as on November 30, 2021, aided by higher order inflows from the marine and industry segments. While orders

in the marine segment are primarily driven by the government’s focus on indigenous procurement, modernisation of Navy and

capacity expansion by shipyards, orders in the industry segment are driven by the company’s increasing customer base as well

as the increasing need to improve electrical infrastructure. The orders in the industry segment are completed within six months

and those in the marine segment require longer execution time of two to three years. However, any delay in execution of

projects from the customers’ end could delay revenue booking for the company, thereby impacting its profitability, and hence

remains a key monitorable.

Long experience of promoters; technical tie-ups with reputed companies – MEIL is promoted and managed by Mr. Venkatesh

Uchil and Mr. Vinay Uchil, who have an experience of around two decades in this business. Besides, MEIL has technical tie-ups

with various companies across the world for advanced systems required in the marine and industrial sectors, which improve

the growth prospects as well as operational diversification of the company.

Reputed and diversified client base limits counterparty risk – MEIL has reputed national and international clients in the marine

industry including the Indian Navy, the Indian Cost Guard, Goa Shipyard Limited, Cochin Shipyard, Mazagon Dock Shipbuilders

Limited, Garden Reach Shipbuilders and Engineers Limited, among others. Besides, MEIL has a strong customer base in the

industrial sector, which includes reputed corporates across various sectors like data centers, banking, pharmaceutical

companies, information technology, automobile, oil and gas, among others. Its reputed and diversified clientele reduces the

counterparty risk to an extent.

Comfortable capital structure; satisfactory coverage indicators – The company’s capital structure remains comfortable, as

evident from a gearing of 0.3 times as on September 30, 2022, given its healthy net worth position as well as low debt levels

due to reliance on non-fund based facilities. ICRA notes that the company’s gross debt levels increased to Rs. 59.5 crore as on

September 30, 2022 from Rs. 36.6 crore as on March 31, 2022. The incremental debt was utilised to provide cash collateral to

the bank, invest in a subsidiary, and partly fund the capital expenditure (capex) requirement. Nevertheless, the net debt

continues to be in line with FY2022 levels.ICRA rating

please share +ve, -ve comments about company

Disc : Recently baught few quantities

Products and Services [ source – screener]

The Co. is engaged in manufacturing and sale of all types of marine and industrial electrical & electronic components like switch-gears, control-gears etc. It is also engaged in the renewable energy sector, specifically solar. It also provides services like designing, fabricating etc. for all types of electrical & electronic installations in India and abroad and undertake annual maintenance contracts. [1]

Revenue Split

Electricals & Electronics– 99% in FY22 vs 74% in FY18

Solar– 1% in FY22 vs 26% in FY18 [2] [3]

Geographic Split FY22

India – 82%

Outside India – 18% [2]

+ve points [ from credit report ICRA]

Healthy order book position – The company’s order book position improved to ~Rs. 500 crore as on December 27, 2022 from

~Rs. 407 crore as on November 30, 2021, aided by higher order inflows from the marine and industry segments. While orders

in the marine segment are primarily driven by the government’s focus on indigenous procurement, modernisation of Navy and

capacity expansion by shipyards, orders in the industry segment are driven by the company’s increasing customer base as well

as the increasing need to improve electrical infrastructure. The orders in the industry segment are completed within six months

and those in the marine segment require longer execution time of two to three years. However, any delay in execution of

projects from the customers’ end could delay revenue booking for the company, thereby impacting its profitability, and hence

remains a key monitorable.

Long experience of promoters; technical tie-ups with reputed companies – MEIL is promoted and managed by Mr. Venkatesh

Uchil and Mr. Vinay Uchil, who have an experience of around two decades in this business. Besides, MEIL has technical tie-ups

with various companies across the world for advanced systems required in the marine and industrial sectors, which improve

the growth prospects as well as operational diversification of the company.

Reputed and diversified client base limits counterparty risk – MEIL has reputed national and international clients in the marine

industry including the Indian Navy, the Indian Cost Guard, Goa Shipyard Limited, Cochin Shipyard, Mazagon Dock Shipbuilders

Limited, Garden Reach Shipbuilders and Engineers Limited, among others. Besides, MEIL has a strong customer base in the

industrial sector, which includes reputed corporates across various sectors like data centers, banking, pharmaceutical

companies, information technology, automobile, oil and gas, among others. Its reputed and diversified clientele reduces the

counterparty risk to an extent.

Comfortable capital structure; satisfactory coverage indicators – The company’s capital structure remains comfortable, as

evident from a gearing of 0.3 times as on September 30, 2022, given its healthy net worth position as well as low debt levels

due to reliance on non-fund based facilities. ICRA notes that the company’s gross debt levels increased to Rs. 59.5 crore as on

September 30, 2022 from Rs. 36.6 crore as on March 31, 2022. The incremental debt was utilised to provide cash collateral to

the bank, invest in a subsidiary, and partly fund the capital expenditure (capex) requirement. Nevertheless, the net debt

continues to be in line with FY2022 levels.ICRA rating

please share +ve, -ve comments about company

Disc : Recently baught few quantities

@ Vikasbargale Agree with your point but i think two wrongs dont make right ![]()

Looking at the current chain of events, looks like wadia group are on the verge of restructuring . They are trying to restructure less complex things ,my hunch is major restructrung is on the cards and these are all precursor to the same .

1.NPL demerger

2.Bombay dyeing land bank monetization

My hunch is next course of action would be merge all holding companies .

Anybody with 2 years time frame will have good risk reward ratio.

Disclosure : Invested very small amount for tracking purpose.

@ Vikasbargale Agree with your point but i think two wrongs dont make right ![]()

Looking at the current chain of events, looks like wadia group are on the verge of restructuring . They are trying to restructure less complex things ,my hunch is major restructrung is on the cards and these are all precursor to the same .

1.NPL demerger

2.Bombay dyeing land bank monetization

My hunch is next course of action would be merge all holding companies .

Anybody with 2 years time frame will have good risk reward ratio.

Disclosure : Invested very small amount for tracking purpose.

I am interested in knowing if some one has done similar studies about AMC and CAMS like stocks in Developed Nations?

Are there any examples where individual AMC may have done better than CAMS in USA or other Developed Nations?

I think, since those Nations are growing their GDP at much lower rate than India, ideally Indian AMC and CAMS should grow at least 2-3 times faster than Developed Nations. Since it is claimed that Indian GDP growth is the fastest in the world. Can we say that, Indian AMC should grow at much faster rate than Developed Nations and also their Valuations should remain high or grow even further.

Also, since Indian Digital economy is growing much faster than Developed Nations, due to large adoption of UPI, Net Banking, and other Digital channels, Is it possible that, AUM growth will be much faster in India. (Personally I do not believe so, but I can see that, lot of big claims are made by some financial experts hence curious…)

I am curious to have these perspectives.

I am interested in knowing if some one has done similar studies about AMC and CAMS like stocks in Developed Nations?

Are there any examples where individual AMC may have done better than CAMS in USA or other Developed Nations?

I think, since those Nations are growing their GDP at much lower rate than India, ideally Indian AMC and CAMS should grow at least 2-3 times faster than Developed Nations. Since it is claimed that Indian GDP growth is the fastest in the world. Can we say that, Indian AMC should grow at much faster rate than Developed Nations and also their Valuations should remain high or grow even further.

Also, since Indian Digital economy is growing much faster than Developed Nations, due to large adoption of UPI, Net Banking, and other Digital channels, Is it possible that, AUM growth will be much faster in India. (Personally I do not believe so, but I can see that, lot of big claims are made by some financial experts hence curious…)

I am curious to have these perspectives.

Attaching the transcript of the proceedings of the AGM. The MD Mr. Shuja Mirza has shed some meaningful insights on the working of the Co.

For starters, not only is the market for sports shoes as a whole growing rapidly organically, the even bigger growth is coming in the shift from the unorganized to the organized sector. Further, the Co. currently is concentrated in the northern part of the country & the scope for geographic growth to newer markets in different states is immense. The Co. is gradually increasing its reach. The coming 3-4 years could be years of high growth. The Co. is also looking to add to its ever increasing range of products by looking to enter the luggage industry once the turbulence in the retail industry settles down in the next year or so.

As regards the perception of Redtape being a discount brand, the MD clarified that the Co. is working on very decent & industry leading operating margins & giving discounts on MRP is only a strategy as it appeals to the Indian consumer’s psyche who enjoys the whole shopping experience more because of the discount, thereby making it a win-win for both the Co. as well as the consumer!!

There has been a lot of debate as to how Redtape should be valued. Investors are not clear as to whether it should be valued as a footware or a garment manufacturer. The fact is that Redtape is neither, but a fashion company & needs to be valued as such, given both, the potential as well as the visibility for growth.

No stock goes in one direction & there will be corrections periodically, but investors need to track both the growth as well as the margins & take a call based on this reality. We are already into the second half of the year & soon we will start extrapolating numbers in 24-25. As of now the stock is under owned with only a couple of mutual funds invested in the Co. Fund managers typically have a longer time horizon & if a few more take a fancy to the story, then the journey could become interesting!

Can anyone Explain why outsourcing CSM in India is better to the innovator companies as compared to the other countries?

Thanks and Regards,

Naman

Decoding IndiGo’s Mega Global Flight Plan

IndiGo, India’s largest airline, is shifting its focus to international expansion as it has already achieved a 60%+ market share in the domestic market.

The airline is targeting international routes to less common destinations, where it can establish an early lead as many Indians seek new tourist spots.

Starting in 2024, IndiGo will receive a fleet of 49 Airbus A321XLR planes, enabling it to offer long-haul international flights to destinations in Europe, Asia, and more.

This strategic expansion aims to position IndiGo as a major global player in the aviation industry.