Hi Mudit

May be you can find answers in the link i am attaching.

I found it useful to understand some other aspects

Chemical Sector: Pessimism An Opportunity?? | Aditya Shah, Sekhar, Jiten Parmar & Ravikant

Hi Mudit

May be you can find answers in the link i am attaching.

I found it useful to understand some other aspects

Chemical Sector: Pessimism An Opportunity?? | Aditya Shah, Sekhar, Jiten Parmar & Ravikant

ACC and Ambuja Cements, the cement and building material companies of the diversified Adani Group, have been recognised as ‘Iconic Brands’ at the 6th edition of ‘The Iconic Brands of India’ by The Economic Times. ACC and Ambuja Cements were commemorated for their remarkable journey as brands and stalwarts of the cement industry. This recognition stems from their unwavering commitment to quality, innovation, and customer satisfaction that have not only stood the test of time but have also become integral to the Indian identity.

In a country as diverse and dynamic as India, these brands have not only provided excellence but have also mirrored the aspirations of a nation on the rise. The ‘Iconic Brands of India Conclave’ celebrates and acknowledges the remarkable journey of ACC and Ambuja Cements, brands that have set new standards in their respective domains. The companies have cultivated unparalleled loyalty among their users and admirers, making them a true cultural phenomenon. They have also etched a distinctive identity in the hearts and minds of consumers, and their stories are nothing short of inspiring.

Mr. Ajay Kapur, CEO, Cement Business, said, “The recognition of ACC and Ambuja Cements as ‘The Iconic Brands of India’ is a testament to our unwavering dedication towards our customers. We are honored to be a part of India’s rich tapestry of iconic brands, and we view this as both a privilege and a responsibility. Throughout our journey at ACC and Ambuja, we have always strived to set new standards in the cement industry. Our journey has been marked by relentless pursuit of excellence and commitment to sustainable practices. This recognition reaffirms our core belief in prioritising quality and customer-centricity. We take pride in our heritage and our commitment to deliver the highest quality products and services to our consumers remains resolute. This recognition strengthens our resolve to continue this pursuit in the years to come.”

ACC and Ambuja Cements have been trailblazers in the cement industry and their tireless pursuit of excellence, innovation in sustainable practices, and unwavering focus on customer satisfaction have earned them a special place in the hearts of millions.

ACC and Ambuja Cements, the cement and building material companies of the diversified Adani Group, have been recognised as ‘Iconic Brands’ at the 6th edition of ‘The Iconic Brands of India’ by The Economic Times. ACC and Ambuja Cements were commemorated for their remarkable journey as brands and stalwarts of the cement industry. This recognition stems from their unwavering commitment to quality, innovation, and customer satisfaction that have not only stood the test of time but have also become integral to the Indian identity.

In a country as diverse and dynamic as India, these brands have not only provided excellence but have also mirrored the aspirations of a nation on the rise. The ‘Iconic Brands of India Conclave’ celebrates and acknowledges the remarkable journey of ACC and Ambuja Cements, brands that have set new standards in their respective domains. The companies have cultivated unparalleled loyalty among their users and admirers, making them a true cultural phenomenon. They have also etched a distinctive identity in the hearts and minds of consumers, and their stories are nothing short of inspiring.

Mr. Ajay Kapur, CEO, Cement Business, said, “The recognition of ACC and Ambuja Cements as ‘The Iconic Brands of India’ is a testament to our unwavering dedication towards our customers. We are honored to be a part of India’s rich tapestry of iconic brands, and we view this as both a privilege and a responsibility. Throughout our journey at ACC and Ambuja, we have always strived to set new standards in the cement industry. Our journey has been marked by relentless pursuit of excellence and commitment to sustainable practices. This recognition reaffirms our core belief in prioritising quality and customer-centricity. We take pride in our heritage and our commitment to deliver the highest quality products and services to our consumers remains resolute. This recognition strengthens our resolve to continue this pursuit in the years to come.”

ACC and Ambuja Cements have been trailblazers in the cement industry and their tireless pursuit of excellence, innovation in sustainable practices, and unwavering focus on customer satisfaction have earned them a special place in the hearts of millions.

Management is demonstrating their drive for growth, acquistion + preferential, promoters infusing own capital. Nos coming and guidance of doubling topline in 2 years. Valuation looks ok.

Management is demonstrating their drive for growth, acquistion + preferential, promoters infusing own capital. Nos coming and guidance of doubling topline in 2 years. Valuation looks ok.

RHP has good enough data to go through for SMEs (I have no knowledge of the industry and I have no healthcare stocks in my PF)

Fundamentally looks decent and does constitute value (I feel), although value isn’t equal to stock performance. The mentioned peers in RHP showcase that it is cheaper than others.

In RHP again, “management of the company” and “promoters and promoters’ group” section shows all basic information. Age, experience, education, other directorships of promoters and financials of group companies.

I just viewed it when IPO was open and assumed that it could be a good pick since it is reasonably valued. Also, it is posting good results from last 3 Financial Years, hence it appears less window dressed.

Note: SMEs are risky. Promoters may or may not be a positive point but lack of good promoters/ absence of business centric promoters/ promoters with no succession plan can be a big issue in long term. In big market caps, generally some basic level management is often automated to lower managements but in SMEs promoters are everything and if promoters decide to exit or any other reason, the company is done. I primarily invest in SMEs and reached 100% allocation. Now bit by bit I am going towards small/mid-caps and Mutual funds and so exiting SMEs wherever possible.

RHP has good enough data to go through for SMEs (I have no knowledge of the industry and I have no healthcare stocks in my PF)

Fundamentally looks decent and does constitute value (I feel), although value isn’t equal to stock performance. The mentioned peers in RHP showcase that it is cheaper than others.

In RHP again, “management of the company” and “promoters and promoters’ group” section shows all basic information. Age, experience, education, other directorships of promoters and financials of group companies.

I just viewed it when IPO was open and assumed that it could be a good pick since it is reasonably valued. Also, it is posting good results from last 3 Financial Years, hence it appears less window dressed.

Note: SMEs are risky. Promoters may or may not be a positive point but lack of good promoters/ absence of business centric promoters/ promoters with no succession plan can be a big issue in long term. In big market caps, generally some basic level management is often automated to lower managements but in SMEs promoters are everything and if promoters decide to exit or any other reason, the company is done. I primarily invest in SMEs and reached 100% allocation. Now bit by bit I am going towards small/mid-caps and Mutual funds and so exiting SMEs wherever possible.

a) If a stock is undervalued, its price may rise before results. At that time, the PE was around 25. Particuarly in microcaps, it is a sad state of affairs that insiders almost always have more information about the actual value of the company.

Also, one of the long-term PE investors exited at this time and new investors took their place. The next quarter shareholding pattern will reveal more on this.

Correction was when the stock went into the ESM, similar to several other microcaps. Several microcaps have similarly recovered by now.

b) No idea. My guess is that older hardware was fully retired by this time.

c) Yes, this is a valid concern.

The corporate governance of the company does not seem to be the best. Earlier, they seem to have revealed to Valorem Advisors a lot of information that was not in the public domain. Hope they get their acts together soon.

Disclosure: Invested

a) If a stock is undervalued, its price may rise before results. At that time, the PE was around 25. Particuarly in microcaps, it is a sad state of affairs that insiders almost always have more information about the actual value of the company.

Also, one of the long-term PE investors exited at this time and new investors took their place. The next quarter shareholding pattern will reveal more on this.

Correction was when the stock went into the ESM, similar to several other microcaps. Several microcaps have similarly recovered by now.

b) No idea. My guess is that older hardware was fully retired by this time.

c) Yes, this is a valid concern.

The corporate governance of the company does not seem to be the best. Earlier, they seem to have revealed to Valorem Advisors a lot of information that was not in the public domain. Hope they get their acts together soon.

Disclosure: Invested

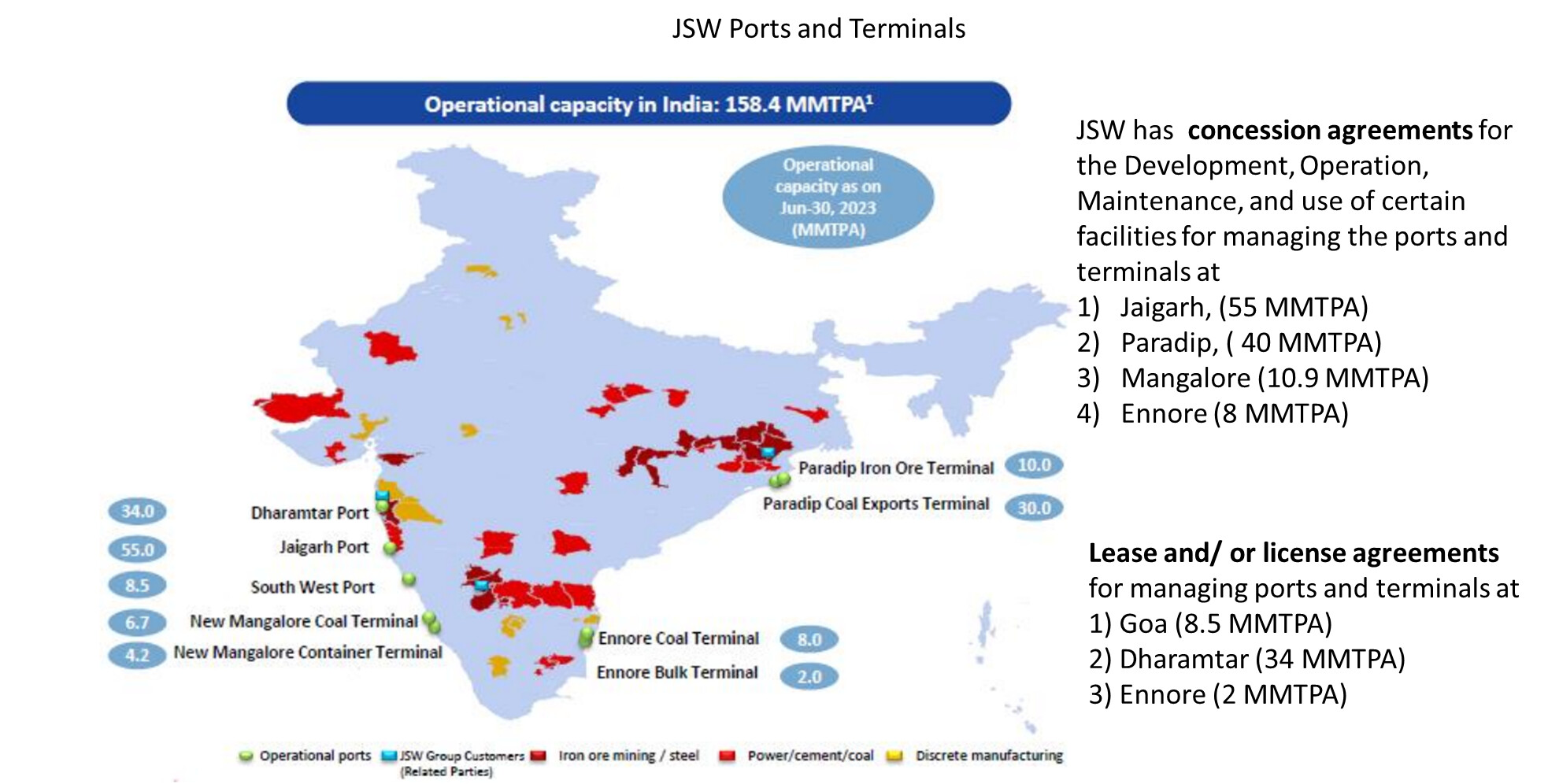

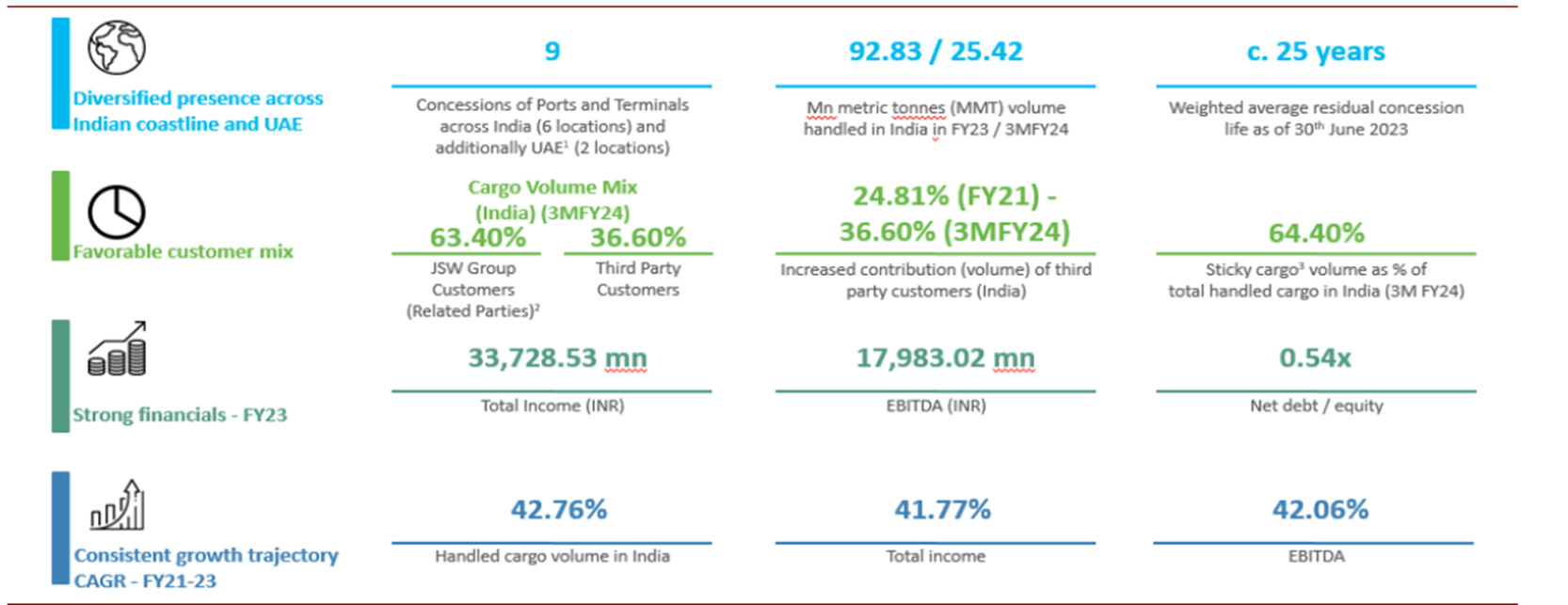

Incorporated in 2006, JSW Infrastructure Limited provides maritime-related services including, cargo handling, storage solutions and logistics services. The company develop and operates ports and port terminals under Port Concessions.

JSW Infrastructure is the 2nd largest commercial port operator in the country in terms of cargo handling capacity in Fiscal 2022.

The company currently handle various types of cargo, including dry bulk, break bulk, liquid bulk, gases and containers. The company currently handling cargo also include thermal coal, coal (other than thermal coal), iron ore, sugar, urea, steel products, rock phosphate, molasses, gypsum, barites, laterites, edible oil, LNG, LPG, and containers.

JSW Infrastructure ports and port terminals typically have long concession periods ranging between 30 to 50 years, providing the company with long-term visibility of revenue streams.

The company has a presence across India with Non-Major Ports located in Maharashtra and port terminals located at Major Ports across the industrial regions of Goa and Karnataka on the west coast, and Odisha and Tamil Nadu on the east coast.

JSW Infrastructure’s international presence includes 2 terminals at Fujairah and Dibba in the UAE.

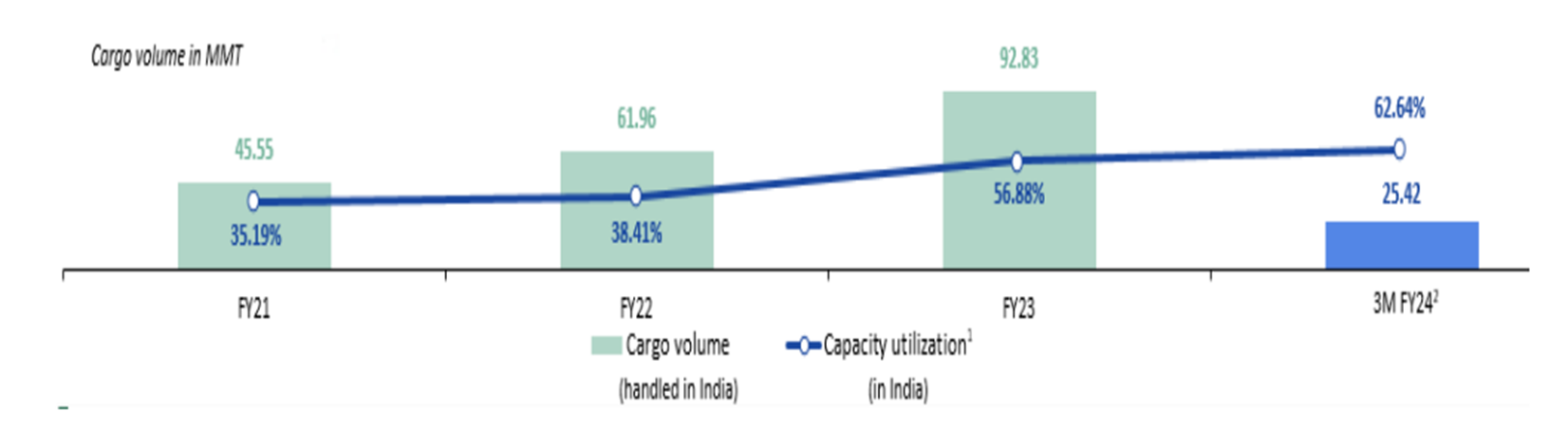

JSW Infrastructure Limited operates nine Port Concessions in India with an installed cargo handling capacity of 158.43 MTPA as of June 30, 2023. The company’s installed cargo handling capacity in India has grown at a CAGR of 15.27% from March 31, 2021 to March 31, 2023.

JSW infra relies on concession and license agreements from government and quasi-governmental organizations. Any breach of the terms could lead to termination and could severely impact its operations.

65% of the total volume handled comprises of coal and iron ore. A significant reduction or the elimination of such cargo could adversely affect the business.

63% of business comes from JSW group customers. Any default or decline in demand could impact the business

3rd Party customers has grown by 47.5% from FY21 to FY23

Its Port Concessions are strategically located in close proximity to JSW Group Customers (Related Parties) and are well connected to cargo origination and consumption points. ~65% of business is coming from these sticky customer base.

~25 years of Concession period for its port. (Recovery of Investment period)

Post IPO company is Net Debt Free.

This enables JIL to serve the industrial hinterlands of Maharashtra, Goa, Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana, and mineral-rich belts of Chhattisgarh, Jharkhand, and Odisha (Source: CRISIL Report), making its ports a preferred option for customers.

In addition, it benefits from strong evacuation infrastructure at ports and port terminals that comprise multi-modal evacuation techniques, such as

Coastal movement through a dedicated fleet of mini-bulk carriers,

Rail Network

Road network

Conveyor systems

Disc: Not invested