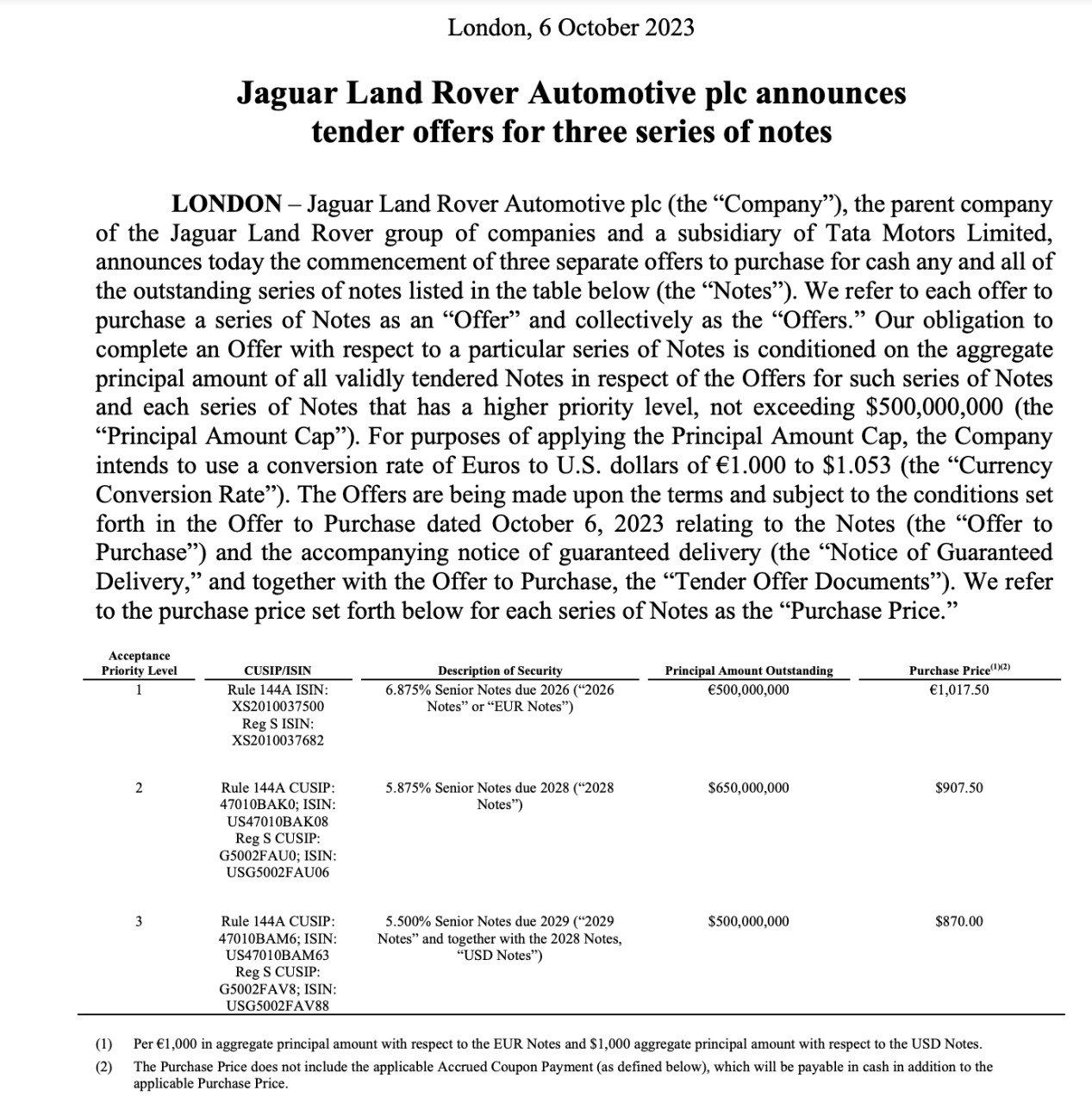

Bond buyback. Wow

Bond buyback. Wow

Teahwa Techno JV is a reflection that they do some global standards which is meeting already and this could lead to other JVs in the future too. As World moves away from china.

India may kaun si company ko solutions provide karti hai?

AGM

Highlights ![]()

Business Revenue constrated on America. Most of the subsidiaries in lose.

Thanks, Hiteshbhai,

I’m not sure if I should ask or not, so it’s okay if you choose not to reply. I’m curious about a few things:

I’m asking because I’m in a dilemma about what to choose, it will surely help me to make my mind. Thanks.

Thanks, Hiteshbhai,

I’m not sure if I should ask or not, so it’s okay if you choose not to reply. I’m curious about a few things:

I’m asking because I’m in a dilemma about what to choose, it will surely help me to make my mind. Thanks.

I am posting on this forum after a long time. Bank has been performing better than my expectations on all fronts except C/I and next parameter in line which the management will address is C/I for which the bank’s target is 65% by Q4FY25. This target itself indicates that huge operating leverage is going to play out in the next 18 months.

Regarding whether the valuation is expensive or not, I would say it depends on how far you are looking into the future and your confidence on the management to deliver. My own estimates indicate that the bank is going to post a core PPOP of 9600-10000 crs in FY25 and an EPS of Rs 7.7-7.8 in FY25. It might sound optimistic to some people but then these are my estimates based on my estimates and I reserve the right to be wrong.

IDFC First and IDFC Merger offers a good arbitrage of 15-16% to IDFC First investors to sell the bank shares and buy IDFC Ltd. There will be tax implications but then eventually you have to pay the tax whenever you sell the stock at a later date too. I have converted my IDFC First stock to IDFC Ltd. So with the transaction, which yielded me 15%, I used 7% to pay my taxes(making the gains till Rs 87 tax free) and the rest 8% to buy more of the bank via IDFC Ltd.

If one is buying IDFC Ltd at 124 today, he/she is effectively buying IDFC First Bank @ 80 which in my view is not expensive at a P/E of 10.4 FY25 earnings( For a bank targeting 18% RoE by FY26) or P/B of 1.43 FY25 Book Value.

I am posting on this forum after a long time. Bank has been performing better than my expectations on all fronts except C/I and next parameter in line which the management will address is C/I for which the bank’s target is 65% by Q4FY25. This target itself indicates that huge operating leverage is going to play out in the next 18 months.

Regarding whether the valuation is expensive or not, I would say it depends on how far you are looking into the future and your confidence on the management to deliver. My own estimates indicate that the bank is going to post a core PPOP of 9600-10000 crs in FY25 and an EPS of Rs 7.7-7.8 in FY25. It might sound optimistic to some people but then these are my estimates based on my estimates and I reserve the right to be wrong.

IDFC First and IDFC Merger offers a good arbitrage of 15-16% to IDFC First investors to sell the bank shares and buy IDFC Ltd. There will be tax implications but then eventually you have to pay the tax whenever you sell the stock at a later date too. I have converted my IDFC First stock to IDFC Ltd. So with the transaction, which yielded me 15%, I used 7% to pay my taxes(making the gains till Rs 87 tax free) and the rest 8% to buy more of the bank via IDFC Ltd.

If one is buying IDFC Ltd at 124 today, he/she is effectively buying IDFC First Bank @ 80 which in my view is not expensive at a P/E of 10.4 FY25 earnings( For a bank targeting 18% RoE by FY26) or P/B of 1.43 FY25 Book Value.

(post deleted by author)