(post deleted by author)

Posts tagged Value Pickr

Is Suzlon a turnaround story after FY16 (07-10-2023)

@manhar – thank you for your response with detailed inputs.

Some of your inputs are in sync with what I learnt from the two reports I posted earlier. Offshore wind power generation while having a lot of benefits is a completely different animal compared to onshore. It needs different EPC skills to setup, power evacuation infrastructure, higher maintenance that is constrained by location (has to be done at near by ports which has the infra for it)…tariff rate is of course higher, but it falls over period of time.

In summary, as of now offshore wind energy is at a very nascent stage of development. While the potential is huge, people looking to profit from such opportunity will have to take it slow and let some actual progress happen on ground before taking a bet. I would let Indian players demonstrate their capabilities in this area before adding this point to my investment thesis pointers

Is Suzlon a turnaround story after FY16 (07-10-2023)

@manhar – thank you for your response with detailed inputs.

Some of your inputs are in sync with what I learnt from the two reports I posted earlier. Offshore wind power generation while having a lot of benefits is a completely different animal compared to onshore. It needs different EPC skills to setup, power evacuation infrastructure, higher maintenance that is constrained by location (has to be done at near by ports which has the infra for it)…tariff rate is of course higher, but it falls over period of time.

In summary, as of now offshore wind energy is at a very nascent stage of development. While the potential is huge, people looking to profit from such opportunity will have to take it slow and let some actual progress happen on ground before taking a bet. I would let Indian players demonstrate their capabilities in this area before adding this point to my investment thesis pointers

Rategain – Fast Growing SaaS Leader (07-10-2023)

Few points I want to highlight about Rategain:

-

TAM by FY25 – 70,125cr (Huge Opportunity)

-

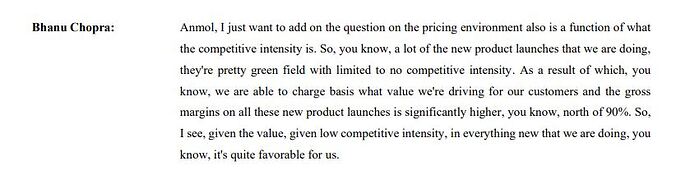

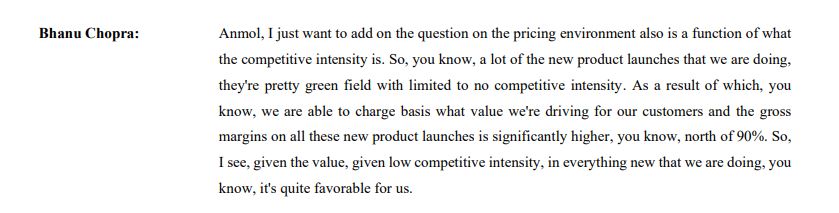

Many of their new product launches are higher in value chain and have limited to no competitive intensity. Gross margins are north of 90%. Good lever for margin expansion along with operating leverage on matured products.

-

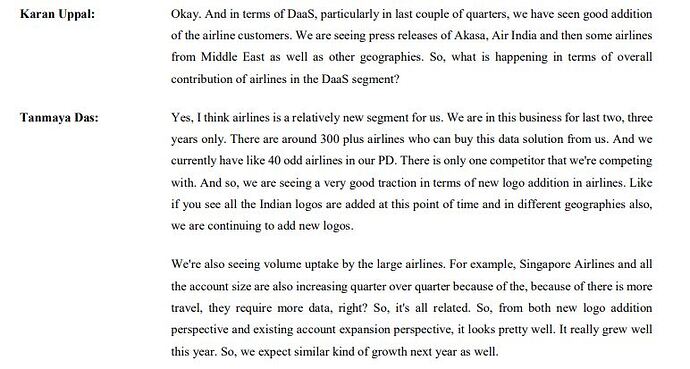

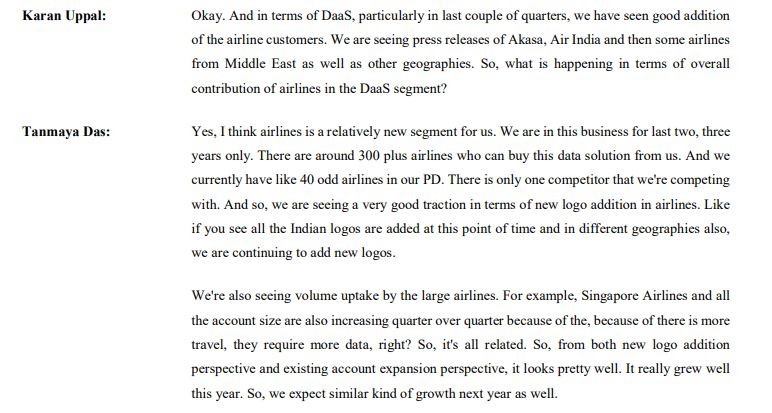

Airlines is a relatively new segment and they are competing with only one player in this.

-

Cyclicality of the travel and hospitality industry is definitely a risk. Cycle is in favor now and just reaching pre-covid levels.

-

Management guiding to double the revenues on FY24 base by FY27. FY24 revenue should be around 875cr. So FY27 revenue comes around 1750cr. You can model with PAT margin expectation.

If mgmt walks the talk, PAT margin can be 20%, which comes to around 350cr.

In base case scenario, giving 40x PE multiple comes to 14000cr Mcap (around 21% CAGR)

Disclosure: Invested, Not a reco.

IDFC First Bank Limited (07-10-2023)

Setting tough goals and then rewarding the concerned employees is (IMHO) one of the best and a very inexpensive way to grow business. Unlike increments, foreign trips are one time expense and enable employees to have greater exposure, social/ cultural education, broader world view and higher self confidence. It makes the high performance employees more motivated. Shareholders should welcome such a policy as long as it is well designed and correctly targeted.

Amararaja Batteries Limited: Powering Ahead (07-10-2023)

Hi everyone, how does one make sense of the related party transaction the promotors have?

I am talking more specifically about fixed assets purchased from related party, & then eventual outright buying of the company/ division.

Like Purchase of FA of 242Crs from Amara Raja Power systems in FY22, followed by 40Crs in FY23 & now buying the stake at seemingly reasonable valuations.

Same with Mangal Industries buying FA worth 57Crs & 45 Crs in FY22&23 respectively followed by now buying of the plastics division of Mangal Industries

Hitesh portfolio (07-10-2023)

Equity investing is a long and a lonely journey. And its filled with periods of emotional turmoil during sharp market crashes. So being a full time investor has its own set of problems.

Usually during bull markets a lot of people aspire to become full time investors, and start dreaming of financial freedom. Nothing wrong with this notion, but there are some factors to consider.

Personally I enjoy full time investing because I have a lot of other hobbies that keep me busy. But that may not be everyone’s situation.

Planning to retire at the age of 30 has its own set of problems. It’s the age when people get married and settled in life with kids and all. From that age onwards, expenses are expected to keep going up for many years to come. So all these factors have to be kept in mind while planning early retirement in the 30s.

Plus any occupation has its own honeymoon period which may last for different years for different people. So we also have to think about potential burnout even in fields of investing after a period of time.

And besides this the crux of the whole equation is about having a starting capital and generating enough returns to keep the life journey going at expected living standards which often are pre set.

I have ennumerated the various aspects to consider while planning early retirement and planning financial freedom. Hope it helps you.

Rategain – Fast Growing SaaS Leader (07-10-2023)

One comprehensive provider that does all doesn’t really exist. Individual segments have few competitors like Codi, Sabre, Amadeus that handle meta and Google. And as agencies like WPP and psPublicis that do social.

Kaveri seeds company limited — kscl (07-10-2023)

So I just did a quick research, Q1 is the summer season. Hence according to Google, almost half of the field crop seeds portfolio that Kaveri has is not suitable to grow in summers in India, hence summers may be more export-dependent. However, their vegetable portfolio has covered all major vegetables that grow in summer in India. This may be one reason for such skewed numbers.

NOT INVESTED, BUT LOOKING TO INVEST

Hitesh portfolio (07-10-2023)

Position sizing strategy remains as before. Anywhere from 6 to 10 stocks with starting allocations at around 10-15%. If position runs up due to sharp run ups, I allow it to run sometimes even to 30-35% of overall PF , but when I feel there is some chances of correction after sharp run up, I trim the position to bring it to comfort levels. If I find that the techno funda picture fits in perfectly and I have a clear idea about the company at the time of entry, I allocate high levels of 15-20% at entry levels itself, but these are rare instances.

This is a style and strategy that suits me as of now, so continuing with it.