(post deleted by author)

Posts tagged Value Pickr

Vedanta Limited – Future Natural Resource Leader (06-10-2023)

Vedanta’s Anil Agarwal is ambitious. Wait to be seen if his gamble pays off. Inspiring to read.

How a United Spirits insider probably got away with insider trading (05-10-2023)

These laws are obviously stupid as you mentioned, and should be changed

The simple definition of insider trading should be (as you also mentioned)

Trading based on Unpublished price sensitive data.

Should not matter if the person is relative of the insider or not.

Here is one of the famous case from the USA

In 2009, the director Rajat Gupta (director of Goldman Sachs) gave Raj Rajaratnam insider information about a potential investment being made by Berkshire Hathway

Based on investigation the SEC established that Raj Rajaratnam had traded based on Unpublished price sensitive data, and was later penalised.

How a United Spirits insider probably got away with insider trading (05-10-2023)

How a United Spirits insider probably got away with insider trading

If you work at a publicly listed company and are aware of some inside information because, well, you work at this company, you can’t trade the company’s shares based on this information. If you do, it’s insider trading, which is illegal.

The general idea of insider trading is straightforward but it gets complicated in practice. What if you’re a company insider, you have some valuable company inside information, but instead of trading its shares yourself, your wife does? This is, of course, still insider trading. You gave her this information, you’re an insider, she’s your wife, so she’s an insider too.

What if instead of giving your wife this valuable inside information, you scribbled this information on a piece of paper, put the paper inside a bottle, and dumped the bottle into the sea. And someone found this bottle, read the piece of paper, traded the shares of your company, and made a quick, big profit? Is that insider trading?

I don’t know! Trading shares based on random information you find on a piece of paper isn’t illegal. But trading based on inside information is. If there was some realistic connection between the insider and the person that makes the trade, yes that would be insider trading. Without it, probably not.

In a way, if you muddy the waters between yourself (the insider) and this person (who trades the shares) enough… you could get away with insider trading. But just how muddy are we talking? Late in August, SEBI released an order which pretty much tells us how muddy is muddy enough. Turns out, not very!

Just ask your in-laws

Back in 2014, Nishat Gupte was an executive at Diageo, a big multinational alcohol company. [1] One of the things that big companies do is acquire smaller companies, and Nishat was part of the mergers and acquisitions team which oversaw these acquisitions.

One of the companies that Diageo acquired nearly 10 years back was United Spirits, you know, the company that owns the McDowell’s brand. In March 2014, Diageo was owning about 25% of United Spirits by buying out the founders’ stake. In April 2014, Diageo announced that it was making an open offer [2] to buy 25% more of the company at ₹3,030 per share, a nice 18% over the market price at the time.

Nishat Gupte, who was at Diageo at the time, obviously knew about the open offer before everyone else. He did not trade any shares. But his in-laws did! His father-in-law, mother-in-law, and brother-in-law bought United Spirits stock options in March and April 2014, just before the company announced its open offer.

The in-laws, the Jashnanis, bought extremely risky deep out-of-the-money call options. These were bets that the United Spirits’ share price would go up a lot in a short amount of time. In its order, SEBI does a neat calculation of the probability of these options making money:

We have also seen that the probability of a substantial rise in the USL stock price over a short time during that period was about 5.75%. If these were independent events, the probability of them coinciding once is about 0.29%. The probability that the two events (one of large risk taking by the noticees, and of a large move in the underlying scrip) would coincide and overlap not just once, but twice within the period, is 0.0008%. In other words, the odds against something like this happening is 99.9992%. And yet, this is indeed what we have witnessed in this case.

Assuming SEBI doesn’t mess up the maths here, and I have no reason to suspect that they do, the probability of success for the Jashnanis was 0.0008%! In March and April, they spent a total of ₹58 lakh ($70,000) buying these options. By the end of April, they made ₹1.56 crore ($185,000). [3]

The Jashnanis weren’t full-time stock market traders who happened to make a lucky trade that particular day. In fact, SEBI said that the last time they had traded in United Spirits was more than a year ago, and a very small quantity. One can imagine SEBI’s monitoring system pretty easily flagging these, umm, extremely lucky trades.

Whoever from within SEBI first caught these trades probably saw that the Jashnanis were the in-laws of an executive at Diageo and thought that this would be an open-and-shut case of insider trading. Well… the Jashnanis didn’t think so! Here’s one of the arguments they made in their response to a notice from SEBI:

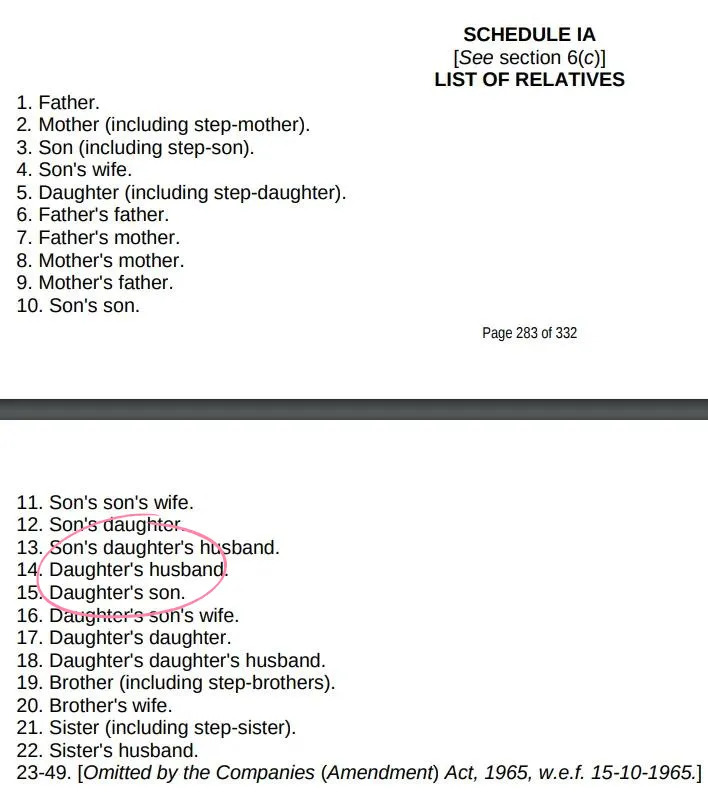

Furthermore, Noticees are not ‘relatives’ of Shri Nishat as alleged. Upon perusal of Section 6 of Companies Act, 1956 read with Schedule IA, it becomes evident that the term father-in-law, mother-in-law and brother-in-law is not used anywhere to depict a relative. A person is deemed relative under Section 6 if and only if they fall in the list of relatives in Schedule IA.

The Jashnanis say here that they’re not relatives of Nishat Gupte, the actual company insider. They aren’t disowning him or denying that they’re his in-laws. But they say that they’re not relatives going by a definition in some Schedule IA of the Companies Act. Let’s look at this Schedule IA:

Okay, first things first. Would you in your wildest dreams have thought that relationships would be defined in the Companies Act?

Anyway so the Companies Act says that if you have a daughter and your daughter has a husband, this person is your relative. In common parlance we would call him your son-in-law. Surely this would mean that you would be your son-in-law’s relative too?

Apparently not! From SEBI’s order:

the relationships have to be construed in only one manner and cannot be reciprocal. Therefore, in order to satisfy the conditions of PIT Regulations, the relationship has to be considered in only one direction and cannot be considered in reverse/ reciprocal manner to establish the charges against the Noticees.

Going by whoever drafted the Companies Act, your son-in-law is your relative but you are not your son-in-law’s relative. Honestly, I could sense the disdain in SEBI’s writing in this entire order. For SEBI to bring someone in for insider trading, they have to prove that someone received insider information. If the trader and the insider are relatives, that makes their job easier.

But SEBI had to go by the nonsense definition in the Companies Act, and we ended up with the nonsense SEBI order which after years of investigation concluded that the Jashnanis didn’t do any insider trading.

This is definitely not financial, legal or relationship advice, but if you’re a company insider frequently in possession of valuable unpublished price sensitive information, treating your in-laws well can be quite profitable.

Footnotes

[1] Yes, SEBI released a final order about something that happened in 2014, in 2023! One of the arguments that the Jashnanis, who were alleged to have insider traded, made was that this was a big delay and the investigation was not valid because of the delayed timeline. But SEBI began their investigation in 2017, published a couple of orders, waited for the Jashnanis to respond to their allegations, went to Court, etc. which took time.

[2] The open offer, by itself, wasn’t a surprise. If someone is buying out a company’s founders, they are required by law to also make an offer to the company’s public shareholders. The idea is that the shareholders deserve a chance to sell their shares since the owners changing means that the company is itself a new one. What was unknown here is the timing of the open offer, as well as the offered price.

[3] The Jashnanis more than doubled their money in less than 60 days. Impressive, sure. But by buying deep out-of-the-money options, they risked their entire capital! They risked ₹58 lakh for a 0.0008% chance of merely doubling their money?

Robust Hotels Hyatt Chennai – undervalued asset play? (05-10-2023)

Hi VPs – I recently got onboarded on the platform, have been reading a lot till the time my registration got approved. Absolutely mesmerized with the depth of content here.

I am taking a shot at sharing my analysis of a company and posting for the first time here, please bear with me in case of any amateur mistakes.

Incorporated in 2007 and promoted by Late Mr Saraf. Robust operates a five-star hotel property under the Hyatt Regency brand in Chennai. RHL was demerged from Asian Hotels (East) Ltd (which now accounts only for the Hyatt Hotel in Kolkata).

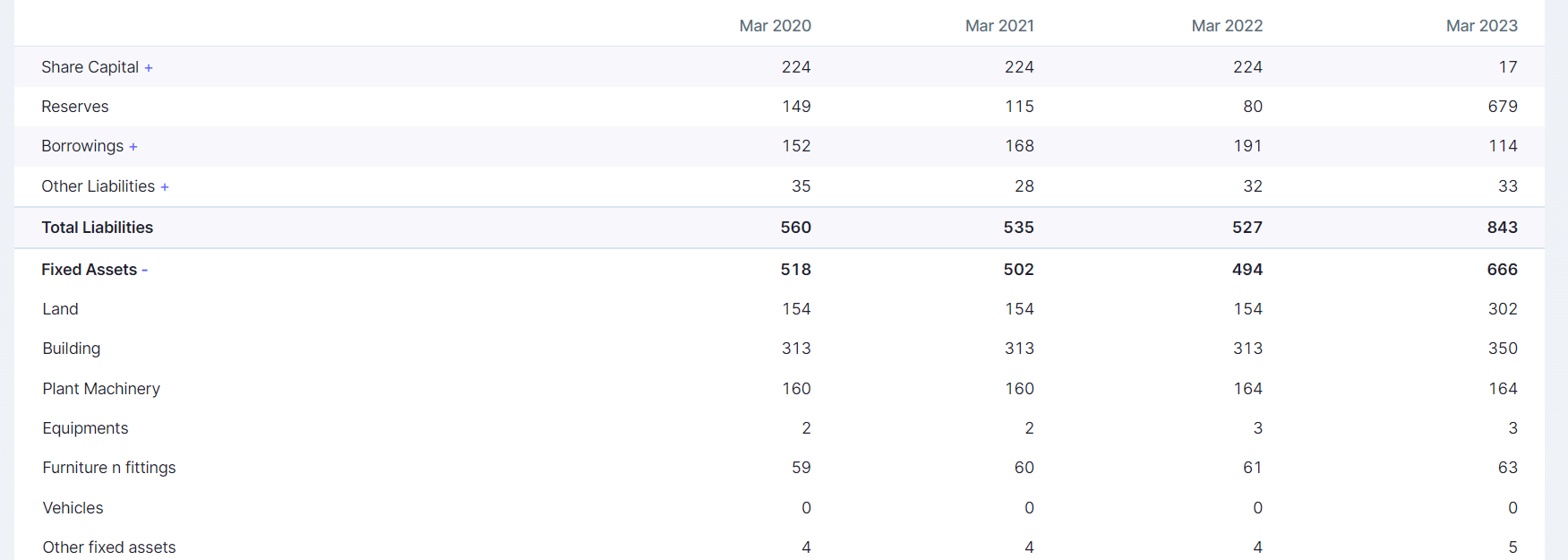

The company recently had a re-evaluation of its land and building value.

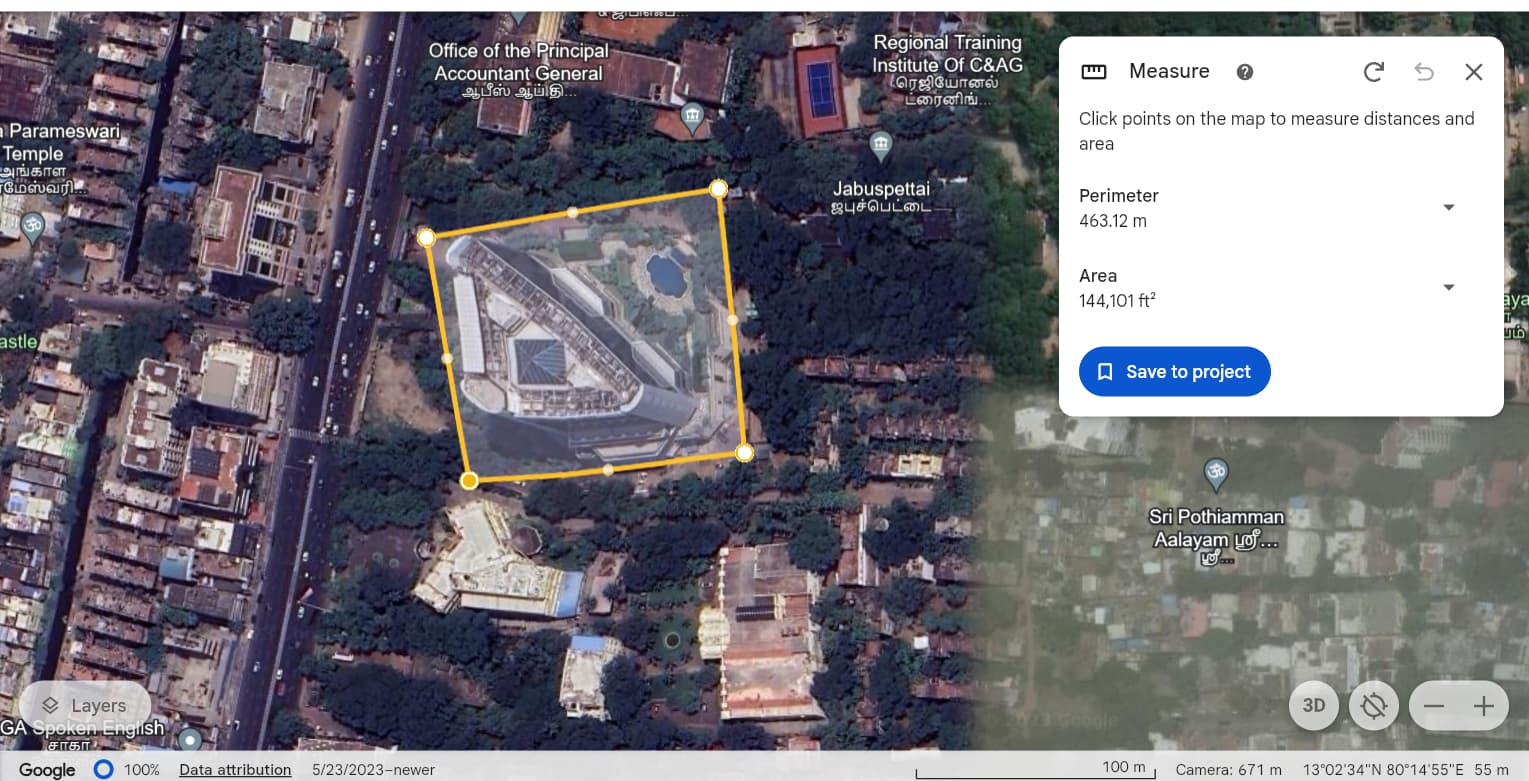

I also did a back of the hand calculation using Google Earth and land price rates in Anna Salai, Chennai.

The re-valuation seems okay on the back of the hand calculations.

The land area comes to around 150k sq feet as shown in the image below.

Residential plot rates in Anna Salai, Chennai as per simple google estimates is nearly 20k/ sq feet (would welcome comments if someone would have a better sense)

Using these 2 numbers – the land value comes to roughly 300 cr as mentioned in the re-valuation exercise undertaken by the company.

If I were to look at company value from an asset replacement method, land value is 300 cr,

Building and PPE even at a 60% haircut comes to around 200 cr. Long term borrowings is 80cr.

So net assets – long term borrowings comes to around (300+200-80) = 420 cr.

Current market cap is around 180cr.

Company has no contingent liabilities ( Hyatt Kolkata has a contingent liability base of around ~ 160cr)

Basis my understanding, Hyatt Chennai also has a few long term negotiations with 1 or 2 corporates. A leading consulting company has their satellite office in one of the floors.

Please let me know your views on this analysis, happy to receive feedback as this is my first analysis of a company.

Direct Plans – Mutual Funds – Online platforms for seamless investing (05-10-2023)

Investing via Zerodha or via the AMC’s own platform does not make a difference in terms of safety. You get the same units. AMC companies make returns out of management fees. They have no incentives to do bogus transactions. I don’t think there is any case where such a thing has happened since the inception of the mutual fund industry in India.

There are cases where fund manager/dealers working for AMCs front run for their own benefit. So the fund holders suffer due to an increased impact cost. A lot of these people have got caught. The loss to unit holder in this case is marginal See How Axis MF fraud case was executed | Mint

Your biggest risk is underperformance or the fund manager not generating enough alpha.

52 week highs and all time highs strategy (05-10-2023)

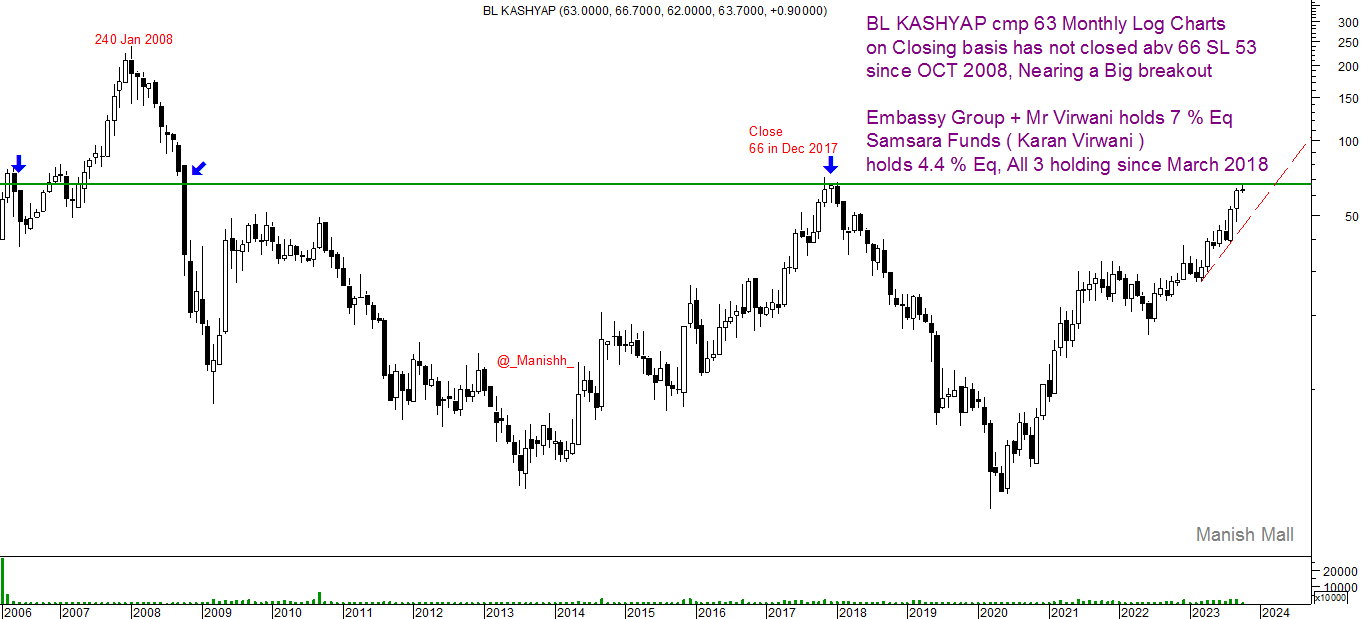

BL KASHYAP cmp 63 Monthly Log Charts

on Closing basis has not closed abv 66 SL 53

since OCT 2008, Nearing a Big 15 Year breakout

with good delivery based buying observed

Promoter 61.6 % Eq was Nibbling Small insider buying last qtr

Embassy Group + Mr Virwani holds 7 % Eq

Samsara Funds ( Karan Virwani )

holds 4.4 % Eq, All 3 holding since March 2018

Mcap 1400 Cr : order book 3000 Cr

last month Order win was from Delhi International Airport

Piccadily Agro Industries Ltd (05-10-2023)

I hear some chatter about promoter family’s one son being involved in a grave incident in the past. It has been discussed in this thread above some time back. It can indeed pose a moral dilemma for some when they are deciding to invest. But that’s just half the picture or shall we say less than ten percent of the picture given how much water has flown under the bridge since then.

And so to make the picture complete, I will throw some light on the other son who also own’s a direct stake (thru Piccadily hotels. His name is Kartikeya Sharma.

He is Rajya Sabha MP. He defeated Ajay Maken (RG’s right-hand man) with the help of BJP to get into RS.

His father Venod Sharma is a former Congress MLA but doesn’t do active politics anymore, but still wields a lot of influence in politics and local area. His mother is the Mayor of Ambala – won as an independent. He is married to the daughter of former Congress MLA & Haryana Assembly Speaker.

He is the founder of ITV media news channels which has 12 news channels including NewsX & India News along with a host of regional news channels. And Hindi & English newspapers such as Aaj Samaj, the Daily Guardian & the Sunday Guardian.

He is recipient of several awards:

Person of Year by BusinessWorld in 2022

Best CEO by eNBA in 2016

Champions of Change 2022

In a nutshell, extremely influential set of promoters who are courted by both the main political parties (you can google and find out more) and own a vast media empire built from nothing.

(A reminder – It is also a well known fact that Mallya senior (Vittal) built his vast alcohol empire based on his political connections )

Add to that an undeniable product & brand development capability. Ask anyone – from the people who have tasted and tried Indri, to the salesman at the airport, to the sales guy at any local alcohol shop in Delhi/NCR – and you will know there is something special about Indri.

Hitesh portfolio (05-10-2023)

@hitesh2710 – Would you be able to share your current bet-sizing strategy and how it has evolved over time?

Is it still about 8 to 10 stocks with 10 to 15% allocation – as in the past?