brokers’ targets for UPL are always 800 to 1000 for years, but the stock reacts and falls well below various resistance points below 800… so we have to take these with a heap of salt. their debt levels are always the issue. they should focus on debt reduction and stop buybacks and dividends till they reduce to below USD 1 Bn at least

Posts tagged Value Pickr

Kirloskar Oil Engines Ltd – Generating Returns from Generators (29-09-2023)

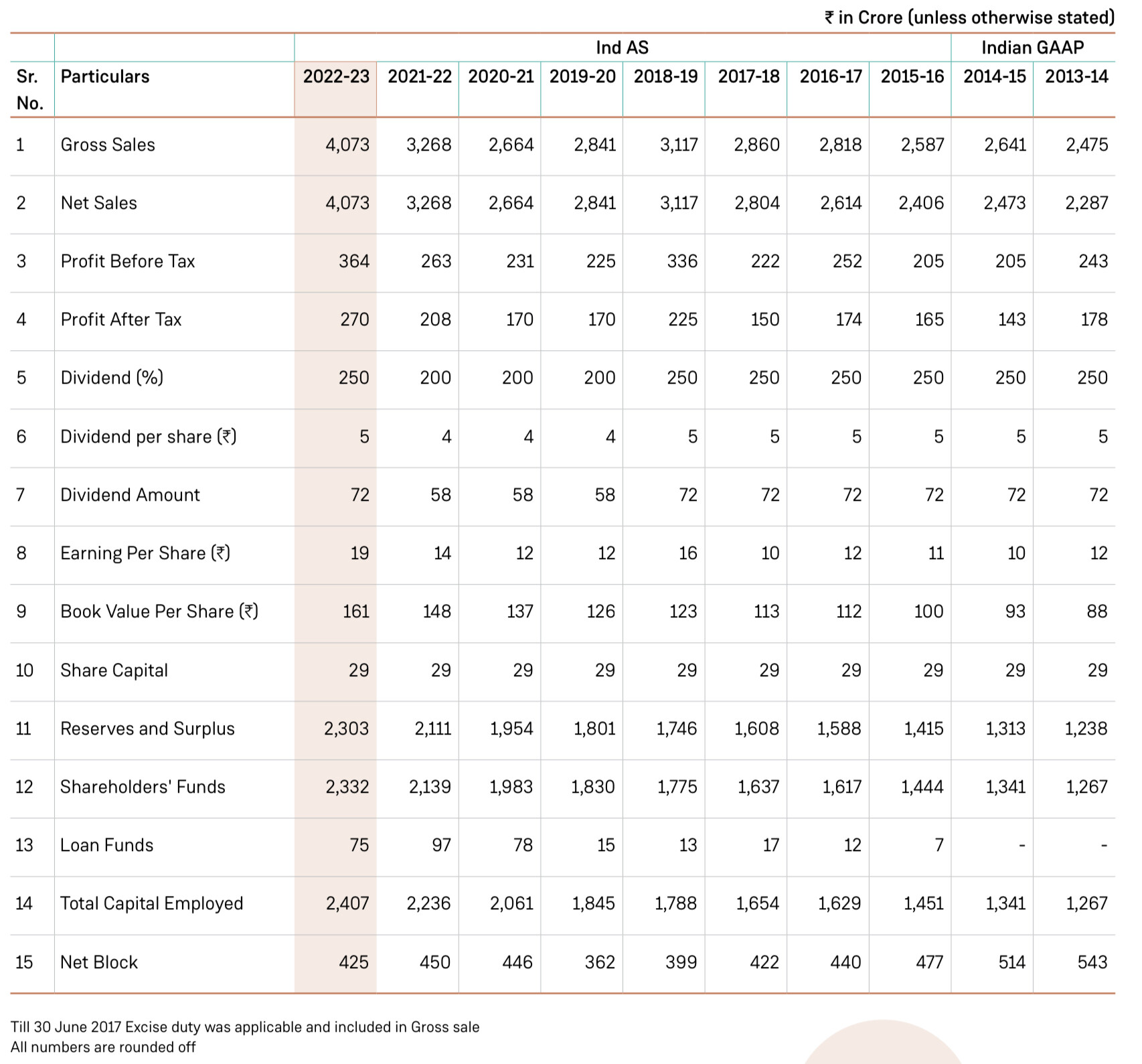

Decade at a glance

Kirloskar Oil Engines Ltd – Generating Returns from Generators (29-09-2023)

I hope I added value to this community

Kirloskar Oil Engines Ltd – Generating Returns from Generators (29-09-2023)

I stumbled across this business as a technical find, however ended up researching about it and thought of sharing my findings.

OVERVIEW:

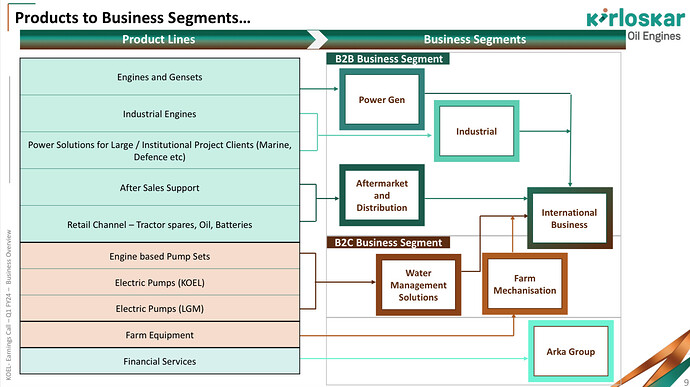

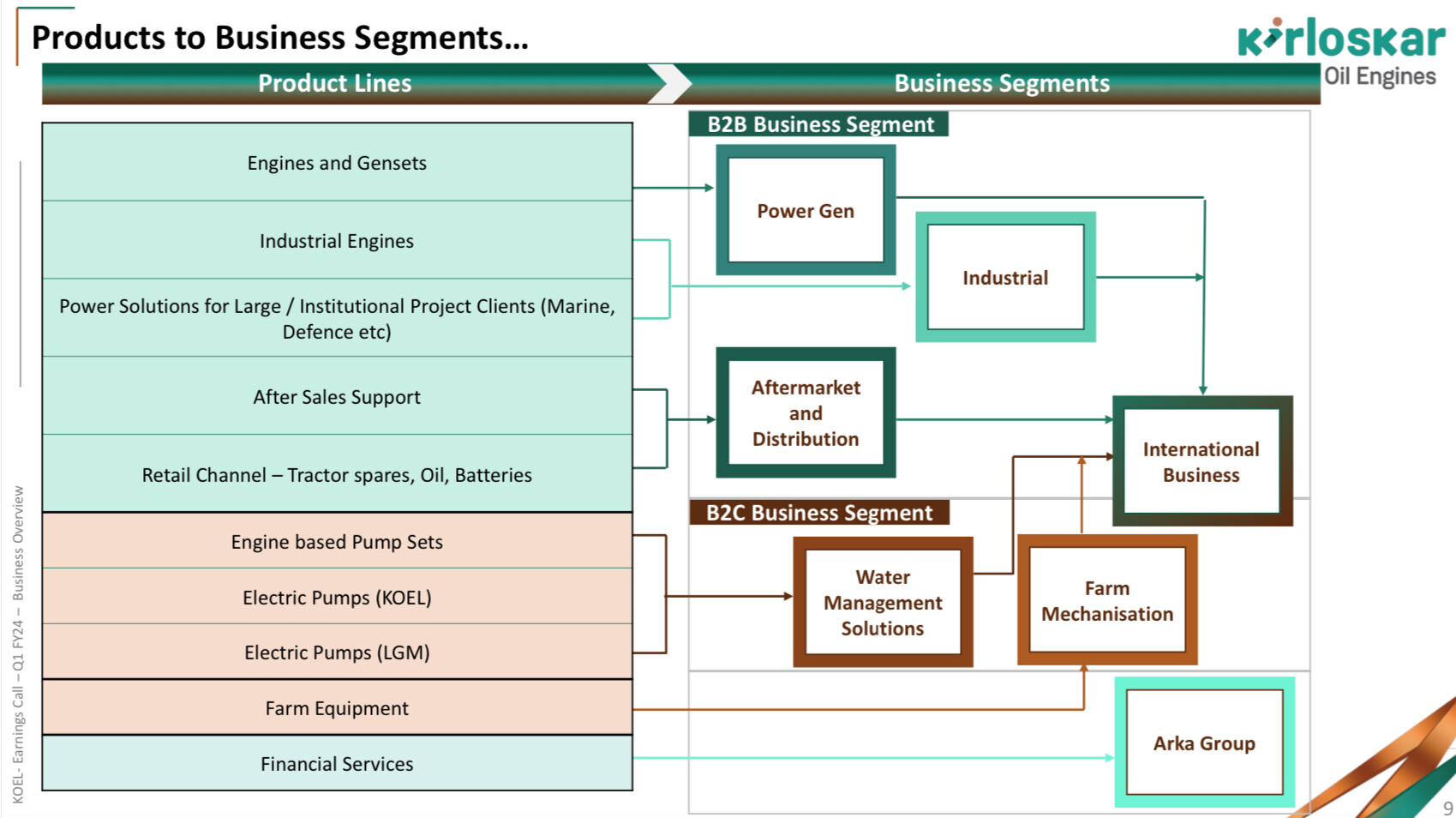

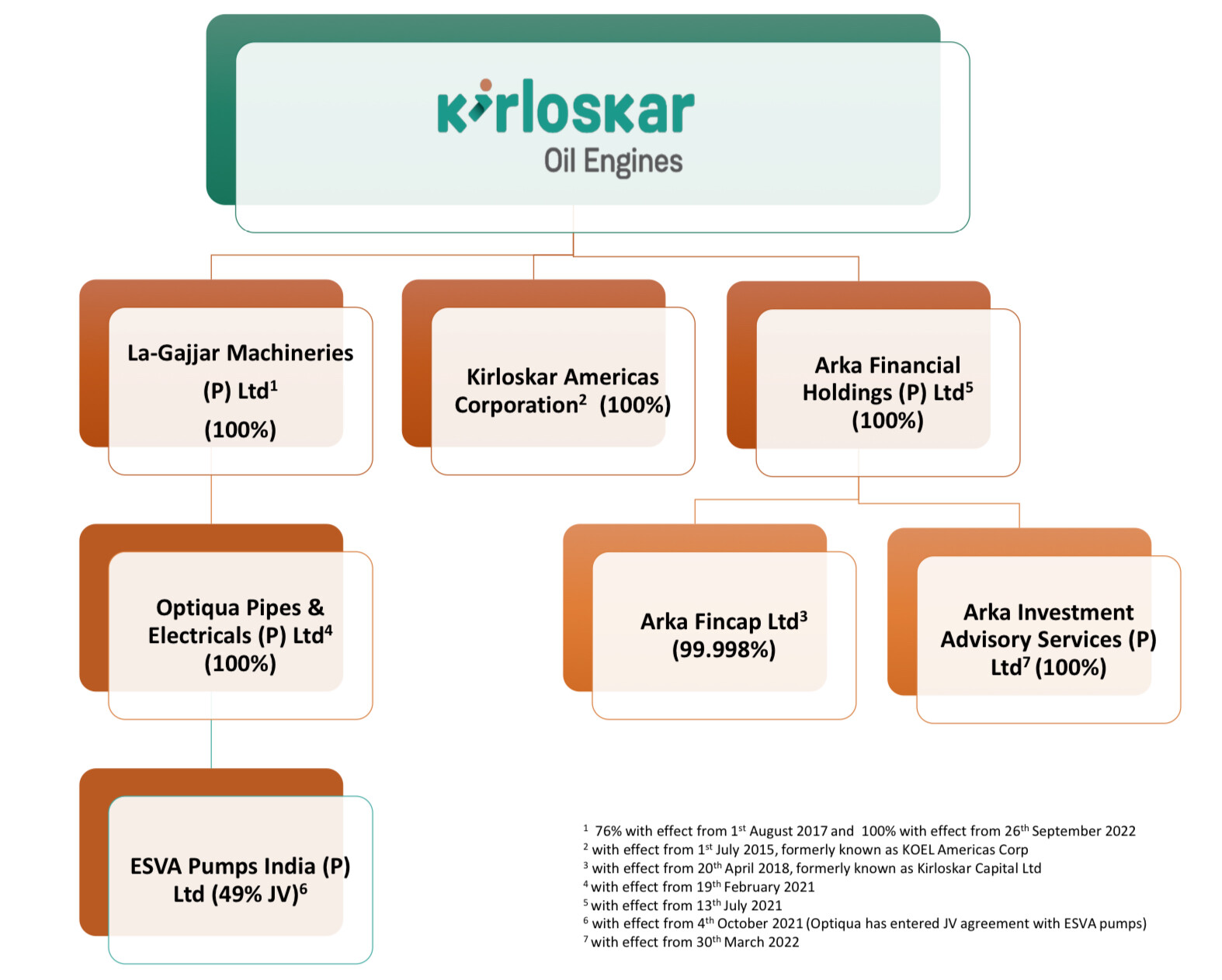

Kirloskar Oil Emgines Ltd’s business is divided into three segments

- B2C

- Engine based Pump Sets

- Electric Pumps (KOEL)

- Electric Pumps (LGM)

- Farm Equipment

- B2B

- Engines and Gensets

- Industrial Engines

- Power Solutions for Large / Institutional Project Clients (Marine, Defence etc)

- After Sales Support

- Retail Channel – Tractor spares, Oil, Batteries

- Arka Group – Financial Services

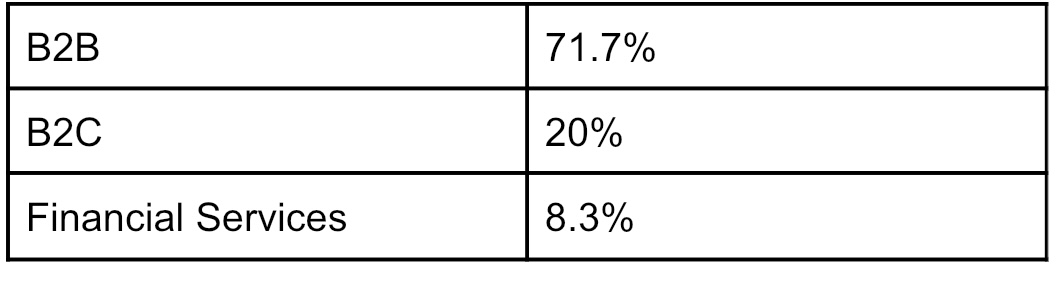

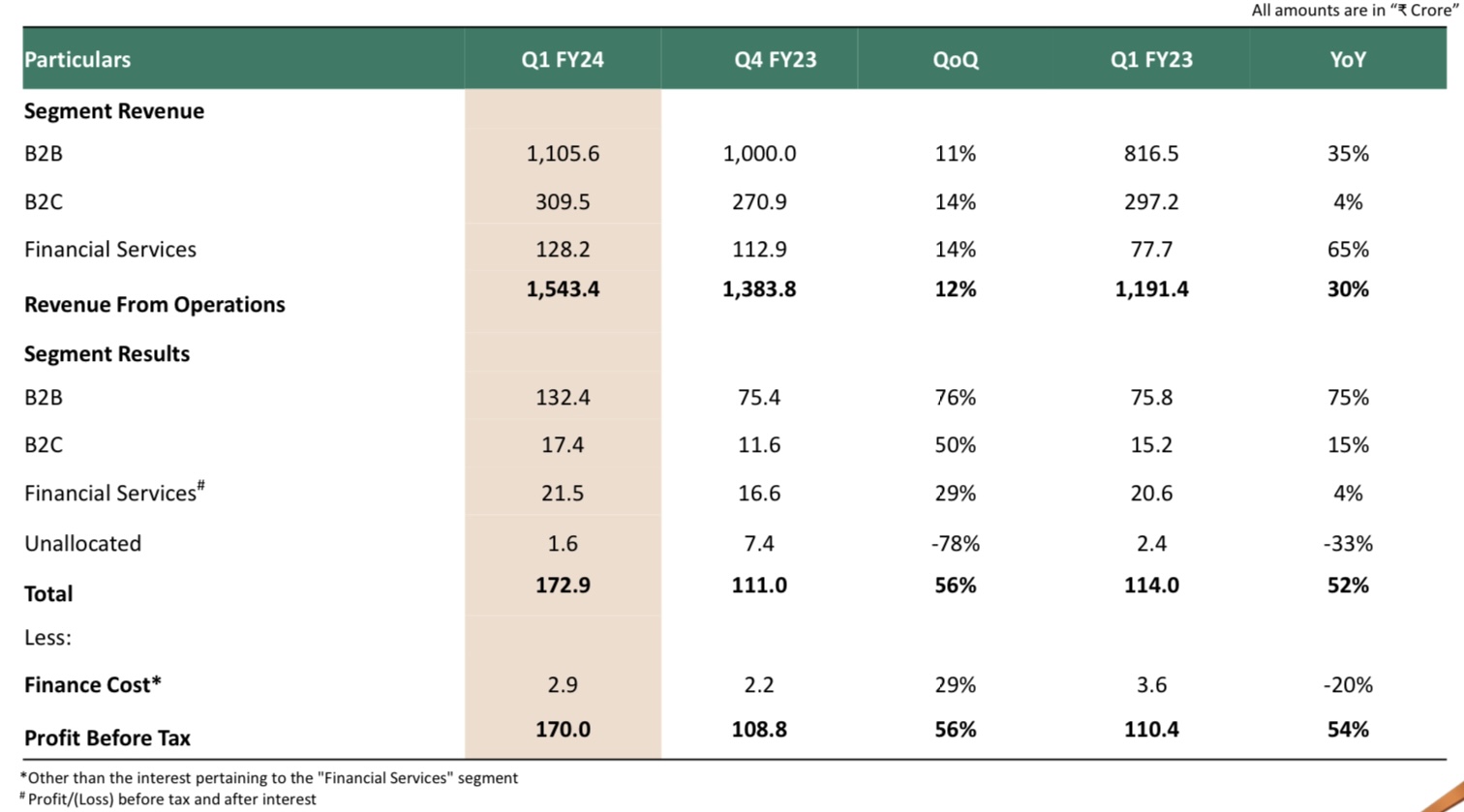

As per the recent Quarterly results; Q1 FY2024, the revenue % breakup for each segment:

-

It’s customers in the B2B business are predominantly from industries like Power, Telecom, Railway, Infra, Railway, Defence and also Data centres

-

B2C customers include ones from Agro and Irrigation

-

Arka Group is a NBFC with focused lending in sectors like real estate, Coporate lending and SME lending (initially started with 500 crores, to diversify business; had very strong and robust balance sheet, and maintained healthy cash positions)

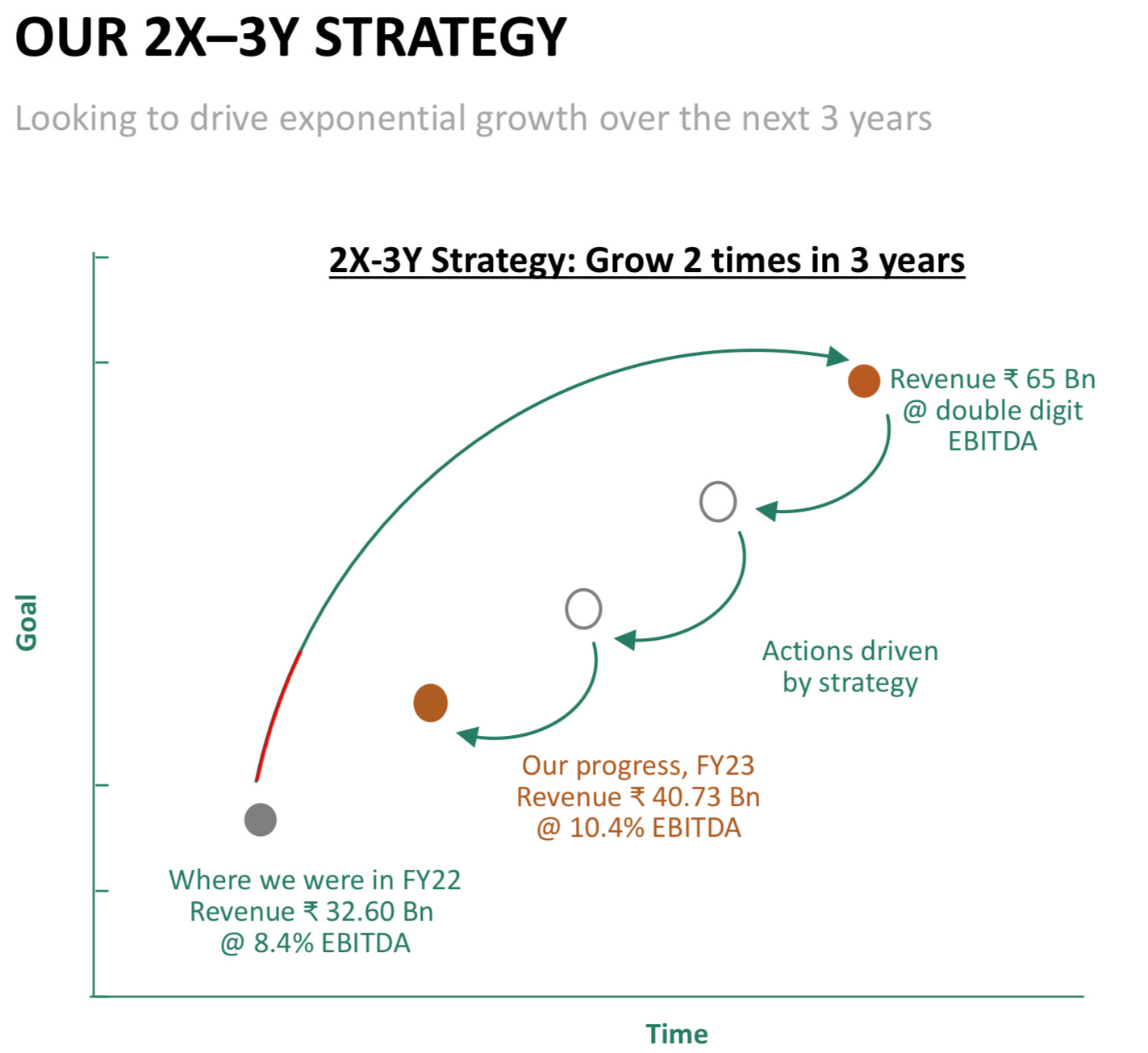

The management had planned for 2X-3Y Strategy; Double the topline in course of three years(indicating an avg revenue CAGR of 24%)

Concall Learnings:

-

It’s part of a legacy conglomerate – Kirloskar Group

-

Not interested in white labelled products

-

Management has shown decent control over fixed costs during volatile times

-

Management is very defensive in terms of its lending business

-

Managements focus on cashing out on the Value added Products

-

OEM’s usually place repeat orders

-

Acquisition of Optiqua (management is keen on water solution segment of its portfolio)

-

Focus on African Continent – delivering good growth in overall exports

-

A growing sales (also focus) in Ultra High Horse power Genset segment

-

The company is benefitted from both power deficit in the country and growing power needs due to infra capex and general population needs

-

Outlook for Q2 FY24 is cautious but optimistic, with potential for growth in new geographies and expanded product portfolio.

-

Commitment to 2X-3Y strategy to double topline in 3 years.

-

EBITDA margin of 12.1% is sustainable, with potential for improvement.

-

Strong performance in the financial services segment with a loan book of Rs. 3,656 crores.

-

Financial services segment experienced a slight decline in AUM, but expected to rebound

-

The company’s Financial arm earns a decent Fee income from Syndication as a third party participant

-

The management is not in a hurry to lend, wants to play a Calibrated move and play defensively for few years before becoming aggressive

-

the management has divided itself into parts, as in the case of different heads for each division

I’ll add a few more interesting concall excerpts below:

Challenges and Risks:

-

Decrease in profitability due to

-

Raw material price fluctuations

-

Decrease in order inflow

-

Mess ups in financial segment of the company

-

Decrease in demand for the Gensets

-

Competition from Chinese Players

-

The company also has a compliance burden; which results in the management to update many of its products accordingly

-

this compliance is Due to the Emmissiom Stamdards set by the government from time to time

-

Also in case of Fuel efficiency standards

Personal take:

Valuations are reasonable, although P/B is high. Personally invested in it. I’ll hold until there’s a constant tailwind environment

- This is my first time preparing a note like this, and I could have made mistakes(will correct if I find any)

- I hope to see some critical suggestions on the timeline

- My observations are not so redundant amd sought after as other professionals

- I’ve not not gone in detail for each product category (as in case of various Categories of engines like Low to Untra High Horsepower ones)

Cochin Shipyard – No more Cheap (29-09-2023)

I have nothing much to comment on 2022-23 Annual report.

The key parameters as mentioned keep varing from time time ,Quarter to quarter as other economic conditions change. That is true for most sectors.

For Cochin shipyard quarterly performance in the past has been quite lumpy with poor performance for 1-2 quarters followed by excellent perfomance , which perhaps could even out the overall performance.

Market is valuing it due to bulging order book and expected further orders keep flowing due to Atma nirbhar Bharat scheme and the other geopolitical situation. Also, these companies could benefit as India can be a base for shop repair maintenance for US Navy and other countries

I had invested as high dividend yield stock some 18 months back. I find now the stock is moving because of industry tailwind.

Discl…Not a buy or sell recommendation. please do your own assessment before investment

RACL Geartech Limited (29-09-2023)

(post deleted by author)

BEW Engineering- A proxy play on pharma and chemical sector (29-09-2023)

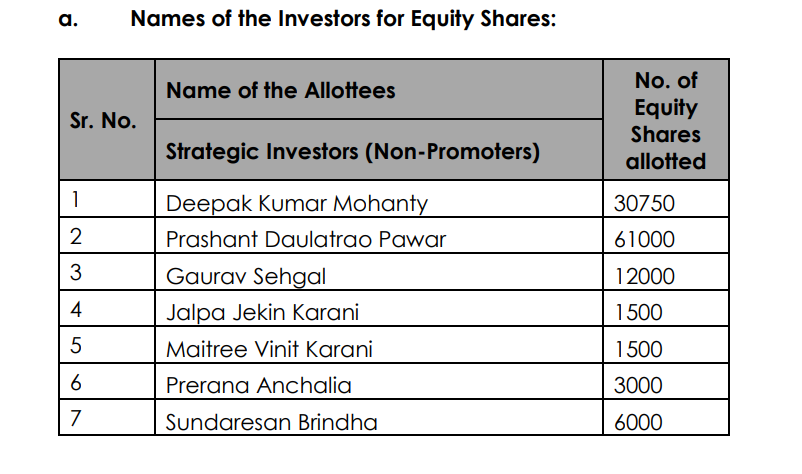

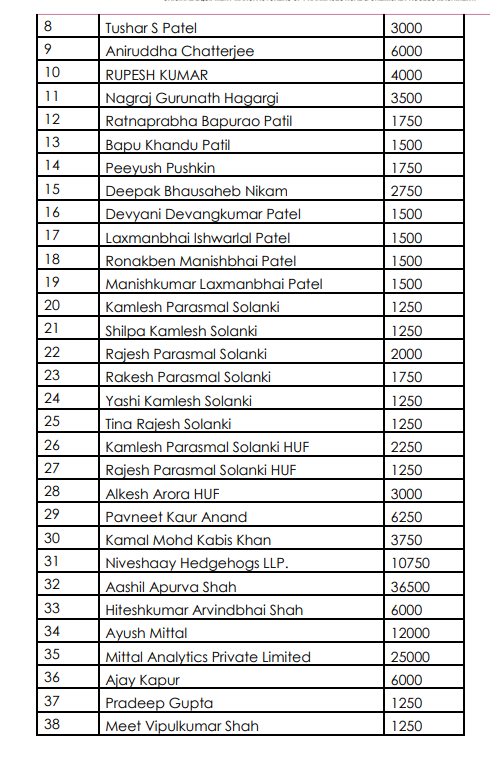

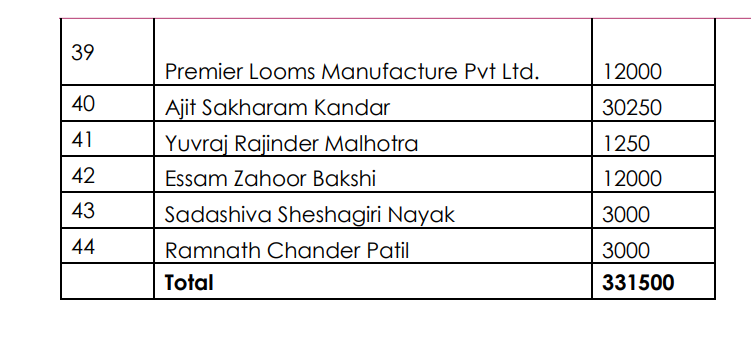

Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“SEBI Listing Regulations”) we hereby apprise you that Company BEW Engineering Limited has made an application regarding In-principal approval for issue of 331500 Equity shares of Rs.10/- each to be allotted under Preferential Basis in terms of Regulation 28(1) of the SEBI (Listing Obligation and Disclosure Requirements) Regulations, 2015.

The above table mentions many know investors like Ayushi Mittal Ji (Founder of Screener.in) and Arvind Kothari Ji from Niveshaay. The preferential allotment was done on 12th June 2023

BEW Engineering- A proxy play on pharma and chemical sector (29-09-2023)

Market Cap of this company is ~ 436 Cr. as on 29th Sept 2023. Liquidity is very low in this stock as the average volume of last 1 year is ~ 4300. My question here is why is the liquidity so low in this stock as other recently listed SME IPO’s in last 1 year have way higher volume as compared to BEW. For example, MOS utility, Drone destination and many other similar companies with the same market cap. Any insights on this from experienced people on this forum will be helpful. @hitesh2710 @ayushmit @Worldlywiseinvestors

Arrow Greentech (Old name: Arrow Coated Products) – Anybody tracking (29-09-2023)

Hi Shahid

Thanks for the kind words.

Avery pharma is a 99% owned subsidiary of Arrow. As per AR notes in 2023 they have generated just 36 lakhs revenue and 5.3 cr loss .

Ranvir’s Portfolio (29-09-2023)

IMHO : Wonderla, Neuland, RPG Lifesciences & Syngene have strong moats & long runway. Have potential for multi decade growth

Disc.: Invested from low levels for very long term