Order book – as on 30/9/24 – 942 crs

Order book – as on 30/6/24 – 939 crs

Order intake during Q2FY24 – 200 crs

Thus Execution during the quarter – 203 crs

Implying solid >100% YOY revenue growth during the quarter. This should also help in improving margins during the quarter

Posts tagged Value Pickr

Jash Engineering – Is it a multibagger (10-10-2024)

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (10-10-2024)

If you see my reply, all I am saying is, company looks good and the promoters don’t look like a Chor (Cuz they have Blusmart running) but I feel this company has to burn a lot of cash as their EV Manufacturing and Leasing business is yet to be profitable, and will not be profitable (EV Manufacturing) till FY29-30. Leasing business will be profitable (Bottom-line) only in FY26-27. I feel they will be profitable and will do well for one more years.

Also their valuation is cheapest among their peers for FY25 (Trading at 20x times) while their peers are trading at 70-100x.

So if you ask me, in Gensol all I care is their EPC Business, other businesses are just an addition to the cashcow business (Solar EPC). So if they deliver in other businesses just like their Solar EPC business then we are seeing a 20,000-30,000 crores Market Cap company.

My only problem is their EV Manufacturing and Leasing business (mostly leasing to Blusmart).

Why leasing business is a problem to me? – Cuz lets say they want to go for an IPO (First Indian taxi or ride-hailing company to go for an IPO, correct me if I am wrong). They have to show profits so that investor will pour money, normally if you are leasing a car for the taxi business, rent will eat at least 30-40% of their revenue, depreciation will eat 10% (maybe 5%), petrol cost will eat another 35-45%, so the margin will be less than 10% and PAT margin will be in the range of 5-7%. If I am a promoter, I will reduce my rent cost to less than 10 or 20%, I feel this is what they will do when the IPO time comes, if thats the case, then Gensol will yield less than 10-20% on their investment in Leasing business

So I don’t care about the Leasing or EV Business (Though I plan to ask this question to the management in the current quarter call). Still, if they don’t eat the profits of Solar EPC and run on their own. And Solar EPC business gets at least 50% more order to the previous year, I am very much comfortable in owing this or even increasing my allocation.

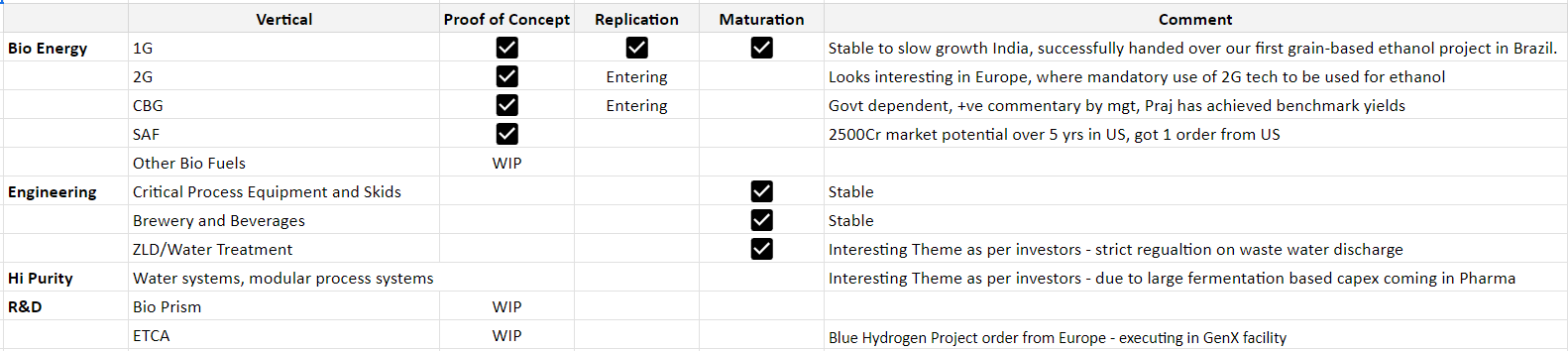

Praj Industries (10-10-2024)

Although dated, but pretty helpful video on Praj – especially the business cycle analysis part.

NPST – Technology Provider for UPI Tech (10-10-2024)

the management has already clarified in their notification to BSE that they are launching / migrating to Evok3.0 and that may cause some issues ( not sure what are the exact wordings ) so not something which is a surprise.

Ola Electric – Full Stack EV play? (10-10-2024)

Good reports, covers both negative and positive.

Disc: Baised and invested as indicated in past post.

My Portfolio (Updates and Suggestions) (10-10-2024)

Liquid funds are more or less the same.

A correction will happen or not is another question in itself.

What I personally did when I had a lumpsum a year back, I found a Mutual Fund I wanted to invest in but didnt want to risk all capital at the same valuation. So I put all the lumpsum money into the Liquid Fund of the same Fund House and Started an STP from the liquid fund into the Fund I wanted.

That helped me flatten out the short term buying prices a bit.

Companies with 20%+ growth guidance for next few years (10-10-2024)

These need to be clearly mentioned. A company that blind sides you on 60% of their current customers and only mentions the 40% they are going after who also happen to be some of the largest fortune 500 companies is suspect.

Dreamfolks services limited( DFS) (10-10-2024)

It is a platform which is bringing together issuers and asset owner for easy transactions for a small fee. Replicating the network at low cost would be a challenge. Why would anyone switch for a marginal benefit, with each passing year it would become more difficult to replace the platform.

DFS is adding more services every few months to strengthen the platform – how much does it take for them to expand into highway lounges (already have issuers, card holders, technology) – they have more bargaining power than the new players – more to offer at lower cost

Shakti Pumps – solar shakti (power)! (10-10-2024)

It is good initiative by the government and it is going to benefit Shakti Pump as technologically it is the strongest player in this segment. This will create entry barrier for existing and new entrants.

Disclosure: No holding.