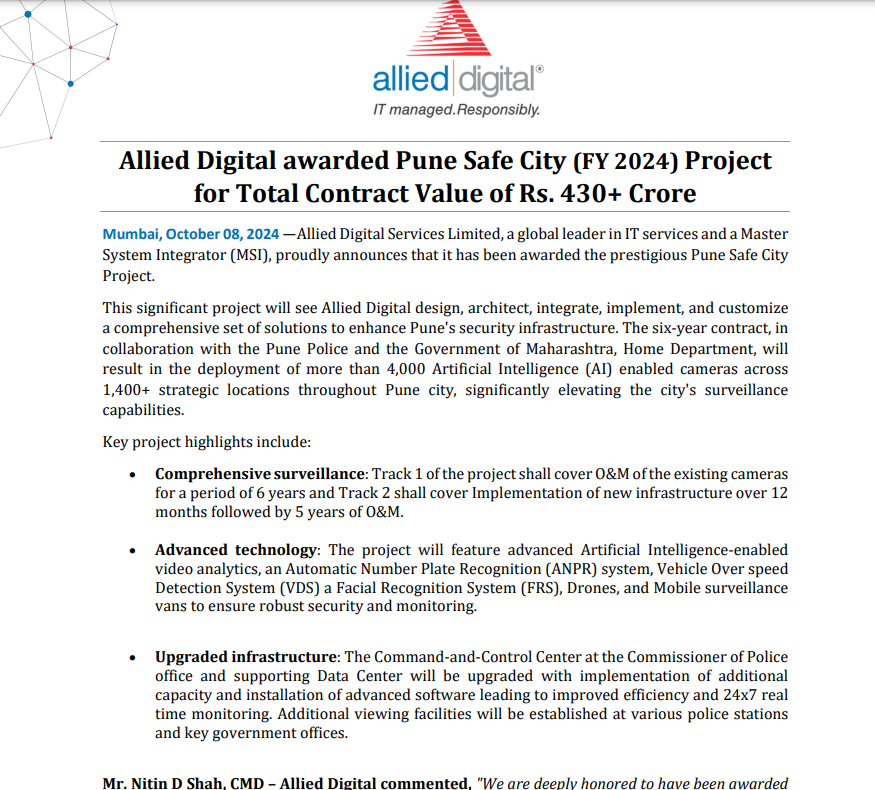

Recent order update

Recent order update

(post deleted by author)

Hedging is a common practice among organized jewelers, especially in India, where gold price volatility significantly impacts profit margins. Most large, organized players like PNG Jewellers, Kalyan Jewellers, and Tanishq use hedging strategies to manage gold price risks and protect their margins. Here’s why it’s widespread in the organized jewelry sector:

Why Hedging is Common:

Common Hedging Instruments:

• Gold Forward Contracts: Jewelers often enter into forward contracts to purchase gold at a fixed price for future delivery, thus locking in costs.

• Futures and Options: These are more sophisticated instruments that allow jewelers to hedge against adverse price movements, offering flexibility in managing gold procurement.

Risks of Hedging:

While hedging is crucial for risk management, it does carry potential downsides. Over-hedging or poor timing in the use of derivative instruments can lead to financial losses, especially in scenarios where gold prices fall. This can hurt profitability and lead to mark-to-market losses, impacting profit after tax (PAT) and return ratios.

Overall, hedging is an essential risk management tool for organized jewelers, providing them with the ability to manage input cost volatility while offering price stability to their customers. So volatility in gold price will effect majority of organised players in same manner depending upon how much of their portfolio is hedged

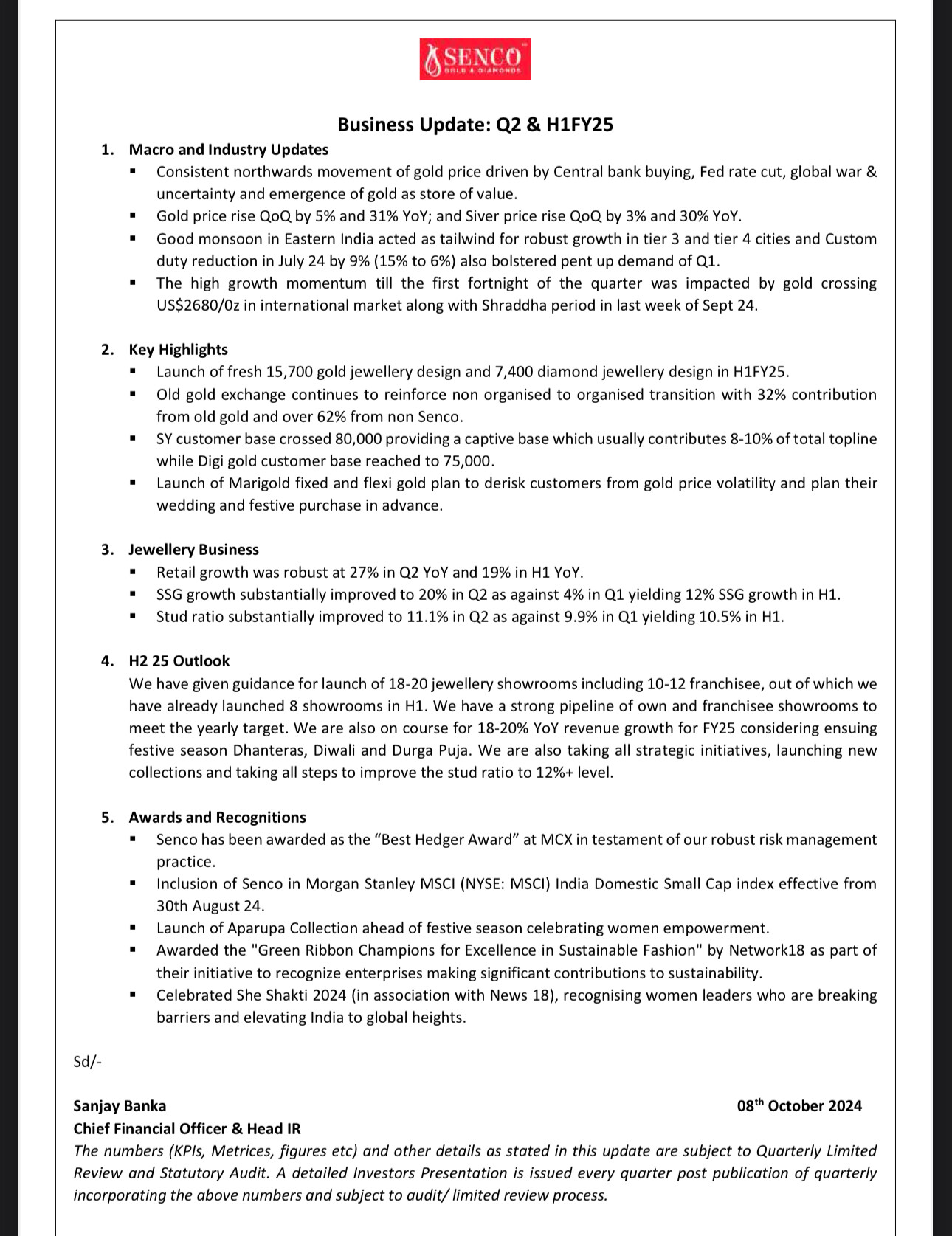

Business Update: Q2 & H1FY25

SSSG Growth 20 %

•H1 SSSG Growth 12 %

•Retail Growth 27 %

•H1 Growth 19 %

Studded ratio improved to 11.1 % against 99.9% in q1

On Track to achieve guidance

•18-20 Showrooms

•18-20 % REV growth

This is an interesting appointment that warranted a press release. It shows the importance the company places on the position( a proxy for future growth?). However, a cursory look at the LinkedIn profile shows instability with constant job hopping, with an approximate tenure of less than two years in the last five jobs.

D: Interested, but not invested.

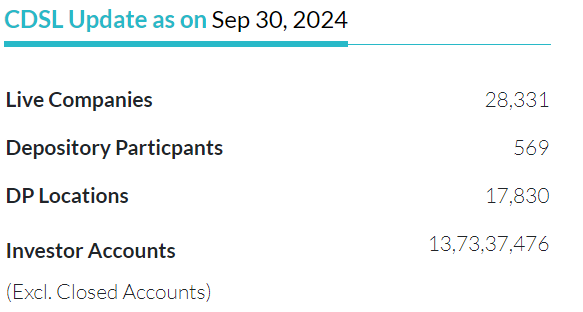

Quarterly update:

New invester and companies addition pace is accelerating with nearly 1.2 Crore investor accounts and almost 3500 new companies added during the quarter.

Expect reasonable growth in revenue and profits as compared to Q1.

AJ

Disclosure: Remain invested. Vews are biased.

Important thing to watch out is what are the terms of agreement between mylan and novo nordisk? By when (which year) natco can start selling ozempic? Natco still will have to get fda approval

Last time in dec 2015 when there was a out of court settlement by natco with bristol & myers for revlimid natco started selling revlimid in 2022 as the patent was expiring in jan 2026 natco got last 3 years of restricted volume exclusivity which means almost after 6 years natco started selling this drug post there mutual agreement…so we dont want such longer wait period…really hope that this time natco starts selling ozempic in next 2 yrs so that it can compensate revlimids sale post jan 2026

If you are looking at financial statements then operating cash flow less interest is the most reliable number to assess the health of the co as good cos generate good cash flows. For reasons not very clear to me interest expense is part of cash flow from financing even though it’s a part of business operations so you will have to take that out from there and deduct it from CFO.

Book value is also a good proxy but some of the figures on the balance sheet are hard to understand so the simpler way is to rely on cash flows

Pre Sales number and average realisation in Rs per sqft that is disclosed in investor presentations is what everyone tracks and gives a good sense of what’s happening in the co

Could be the lingering effect on retrospective tax rule?

Premature. Also, isn’t Cohesion MK Best ideas also MKela? Appears under FII holdings.

Taking TRIL results + Q2concall into account – we are witnessing a mammoth turnaround and if the management continues to execute, FY27 could be mind-numbing.

Holding tight – once in a lifetime opportunity for the company, and shareholders.