And for “Resolution 5: To increase remuneration of Mr. Ritesh Arora, CEO- India & Far East Business, of the Company.” as well, 85% of institution voted against. And since promoter group’s vote is nil, the total vote against is ~40%.

Posts tagged Value Pickr

Zomato – Should you order? (09-10-2024)

It will obviously slowdown given the pace of new store openings. The fact that GOV per store per day is still growing QoQ suggests more mature stores are actually doing quite well.

Look at number of new stores opened in each quarter as a % of stores at the beginning of period. It is 21% in 1Q25 vs. just 2% in 1Q24.

Zomato – Should you order? (09-10-2024)

If you look closely, from the last few quarters the growth in average GOV per store is slowing.

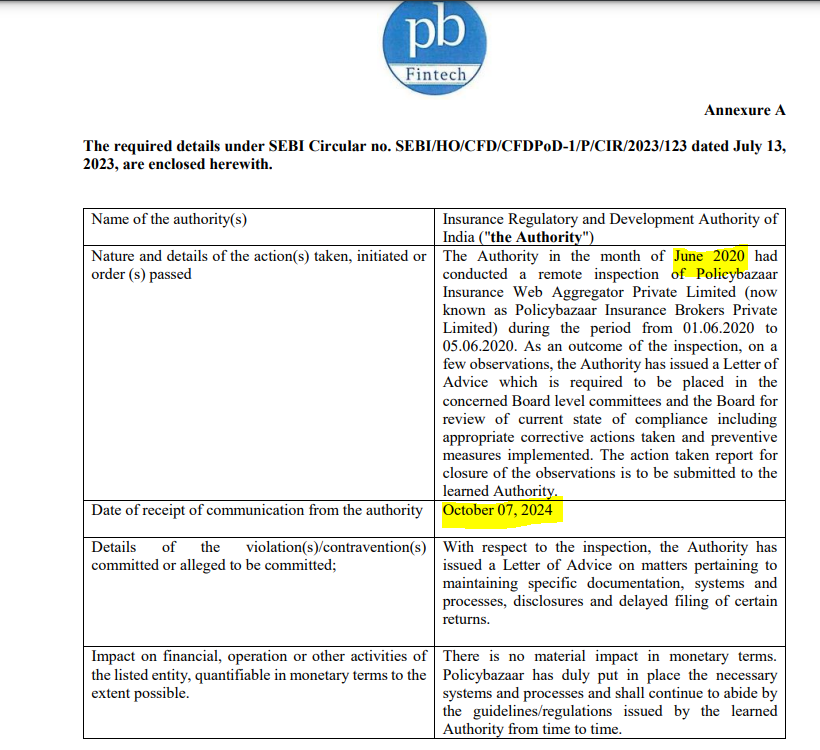

Policybazaar – Insurance Online (09-10-2024)

IRDAI isn’t too fast?

Inspection made in 2020 & Date of receipt of communication from the authority is 2024

Zomato – Should you order? (09-10-2024)

Further, Blinkit is expanding its SKU’s offerings to newer things which in turn leads to requirement of Bigger warehouse in congested urban areas as well as lower inventory turnover for many items, which can negative effects on Margins. Grocery is very difficult business but mixing grocery with Electronics as well as clothing is very difficult.

P N Gadgil Jewellers Ltd (09-10-2024)

Hi . Have you studied the hedging policy of the company. It can effect the return ratio and PAT both in good and bad ways depending on gold price movement.

It’s one of the risk for this company.

Praveen’s portfolio (Coffee Can) (09-10-2024)

It was a small position for me because their numbers looked good. I sold later though. If you search for talbros engineering in this website, you should come across some posts from me

Samhi Hotels – Turnaround with Tailwinds (09-10-2024)

Guilty of confirmation bias

A nice write-up, although I disagree with debt reduction level, here they have extrapolated first quarter debt reduction to all 4 quarter which 52 * 4 = 208, however in q3, q4, the debt was already 65cr only so I don’t think debt will reduce much higher or anywhere close to 50,

TLDR: IMO debt reduction should contribute to 120-140cr to bottom line as per this above article

Trent — A value unlocking story from the house of TATA (08-10-2024)

TRENT IN FOCUS

- Unveiled Lab Grown Diamonds Jewellery Line

Kotak Says:

- Co has launched a lab-grown diamond jewelry brand ‘Pome’ in Westside stores.

It has

- Disruptive pricing (1 carat solitaire engagement ring at Rs24-29k)

- Elegant designs with exquisite craftsmanship.

Kotak Believes:

- Pome has the potential to be Zudio of LGD jewelry market.

Remember,

Trent also announced its entry into the beauty products market at an entry value level

Also important to track what Trent’s entry in LGD does to the other group company – Titan.

Very, very interesting space this

Trent — A value unlocking story from the house of TATA (08-10-2024)

TRENT IN FOCUS

- Unveiled Lab Grown Diamonds Jewellery Line

Kotak Says:

- Co has launched a lab-grown diamond jewelry brand ‘Pome’ in Westside stores.

It has

- Disruptive pricing (1 carat solitaire engagement ring at Rs24-29k)

- Elegant designs with exquisite craftsmanship.

Kotak Believes:

- Pome has the potential to be Zudio of LGD jewelry market.

Remember,

Trent also announced its entry into the beauty products market at an entry value level

Also important to track what Trent’s entry in LGD does to the other group company – Titan.

Very, very interesting space this