All Banking Awards.

Vaidyanathan got Banker of the year. (At 44 mins in video)

Posts tagged Value Pickr

IDFC First Bank Limited (08-10-2024)

Transformer & Rectifier India Limited (08-10-2024)

Profit booking I reckon, he entered sub 200 and it was a substantial stake. I remember him mentioning it on an interview after the first time he trimmed his holding, something along the lines of I believe in the company but its run up a lot so I booked some profit to invest elsewhere.

Jubilant Pharmova (Previously Jubilant Life Sciences) (08-10-2024)

Latest report on Pharmova by Nuvama

I hope you find it useful

dr.vikas

P N Gadgil Jewellers Ltd (08-10-2024)

Do you find the valuation to be comfortable?

Personally, I think it is bit on a higher side given it’s operating margins.

Max India – Demerger, Will sum of parts be greater than single entity (08-10-2024)

• Seek to draw parallels between the merger application of Shriram LI Holdings and Shriram Life Insurance Company with Max Financial and Max Life

• NCLT is of the opinion that a holding company can get merged into its subsidiary life insurance company

• Shriram merger is yet to be approved by IRDAI

• If Shriram merger gets concluded, then it sets a precedent for Max Financial to get merged into Max Life Insurance and thus simplify the structure

Natco Pharma: Focusing On Complex Products (08-10-2024)

Natco has delivered in style… Pockets bulging with cash, plenty more Para IV products filed and lined up relative to 2016-17 and a confirmed potential blockbuster drug launch just when the incumbent lenalidomide would have peaked in sales… The question to what after 2026 has been firmly answered…

The icing on the cake would be the domestic approval for Ozempic!

The cherry on top of it would be the much anticipated acquisition,

and there are atleast 2 more drugs which they would be launching around 2026 from their existing para iv pipeline…

The net profit should not be lumpy as feared for the next 5 years atleast as Ozempic patent in US is till March 2031… That is the bullish thesis, bear in mind that there remains a possibility of price erosion in the near future for a patent protected drug…

Anshul’s investing journey (08-10-2024)

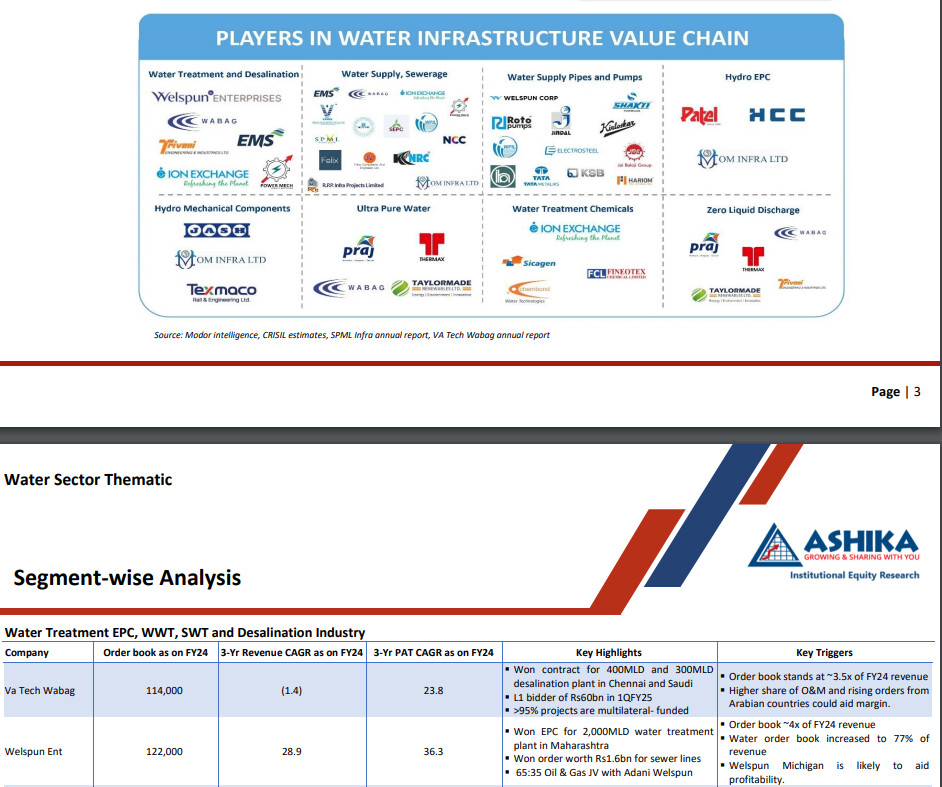

Welspun enterprises – Water theme

P N Gadgil Jewellers Ltd (08-10-2024)

Reasons for PNG Jewellers’ Lower Margins Compared to Listed Peers:

- Geographic Concentration: PNG Jewellers’ primary market is concentrated in Maharashtra. While this region is lucrative, it limits their ability to benefit from economies of scale compared to peers like Kalyan Jewellers, which has a broader geographic footprint. As a result, PNG may face higher relative fixed costs, reducing margins .

- Smaller Operational Scale: Compared to larger players like Kalyan Jewellers, PNG Jewellers has fewer stores and a smaller operational scale. Lower scale typically means higher per-unit costs for procurement, marketing, and operational overhead, negatively impacting margins .

- Higher Making Charges: PNG Jewellers is known for its handcrafted jewelry, which often comes with higher making charges. These higher costs, while appealing to a specific customer base, can limit margin flexibility compared to more mass-market products .

- IPO Costs and Expansion: Recent IPO expenses and ongoing expansion efforts, such as the opening of 12 new stores, could be contributing to lower margins in the short term as the company focuses on growth rather than immediate profitability .

- Lower studded PF .

Future Margin Improvement Drivers for PNG Jewellers:

- Economies of Scale Through Expansion: With the capital raised from the IPO, PNG Jewellers plans to open 12 new stores. As the company increases its store count and expands beyond Maharashtra, it can achieve better economies of scale, reducing per-unit costs for procurement and marketing, thereby improving margins .

- Optimized Supply Chain: PNG has the opportunity to streamline its supply chain to reduce costs and improve operational efficiency. As the company scales, it can negotiate better terms with suppliers and reduce costs in raw materials procurement .

- Digital Transformation: The company’s push toward e-commerce can drive higher-margin sales. E-commerce generally has lower overhead costs compared to physical stores, and by improving its digital presence, PNG can reach a wider audience with less investment in physical infrastructure .

- Product Diversification: Moving beyond traditional gold and handcrafted jewelry to more modern, lower-cost designs could help PNG cater to a broader audience and drive higher margins through product diversification. Offering more diamond and platinum jewelry can also increase margins .

- Focus on Higher Value-Added Services: PNG could focus more on value-added services such as customization, exclusive collections, and loyalty programs, which can allow for higher pricing power and margin improvement .

- As they are guiding for >15% studded PF, margin will improve with it.

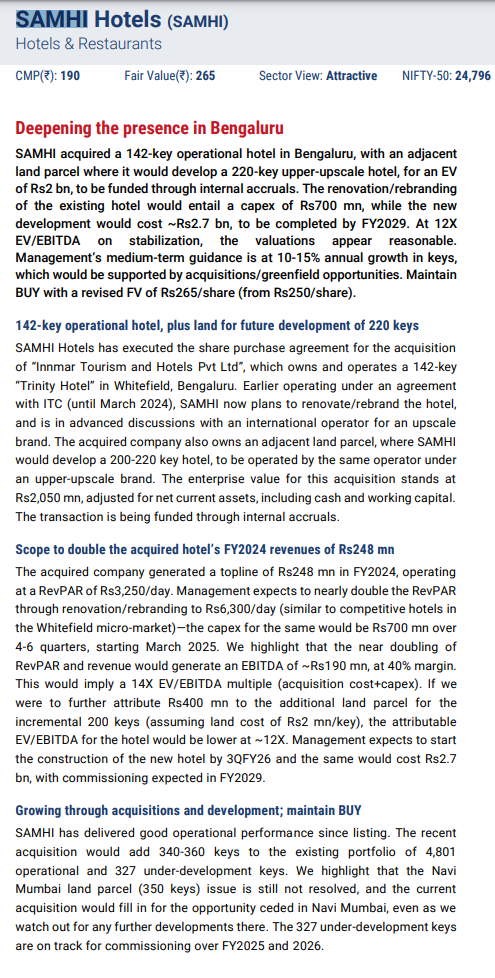

Samhi Hotels – Turnaround with Tailwinds (08-10-2024)

Samhi Kotak’s report

E2E Networks Ltd – Listed small Cloud computing player (08-10-2024)

Nvidia H200 GPU getting added to E2E networks kitty. H200 GPU is 45% higher computing speed as compared to H100 GPU.