Posts tagged Value Pickr

Deepak Nitrite (07-10-2024)

Would request someone tracking the company to give a quick recap if possible, since i cannot understand regarding the nitric acid capex along with flourination. and also regarding the raw products nd end products… seems rm prices for deepak would increase since increase in crude prices. isn’t it?

Himadri Specialty Chemicals (07-10-2024)

Since the threat has been not active since long, I thought of putting up some summarised notes of my here, much of it derived from the links and discussions shared above and the investor ppts of HSCL.

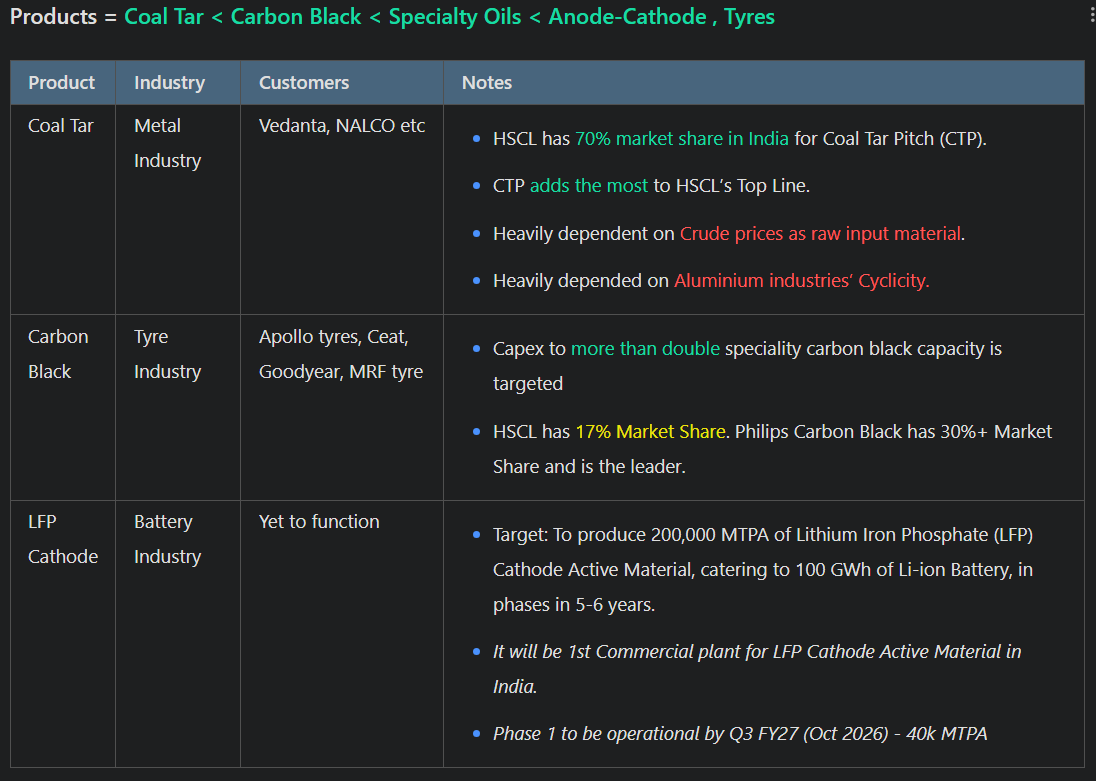

Products

Products Analysis

Peer Comparison

Management:

- Promoter increased stake by 5% this year.

- MD says will continue the earnings momentum.

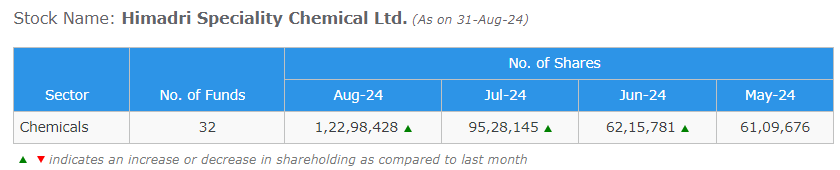

Shareholding Trends:

- Mutual Funds increased stake by 29% in the month of August.

- Currently, retail holding is close to 42% (which is very high).

Thats it. I am looking forward to sharing more as I keep tracking the stock. I remain invested in the stock since a month or two at 490 Levels. Looking forward also to get more insights from fellow folks who are tracking it!

Himadri Specialty Chemicals (07-10-2024)

29% Increase in MF Holding in August Month. I’ll be awaiting September disclosures too.

- Many Active funds hold it.

- Shriram Flexi Cap fund did new entry in Aug.

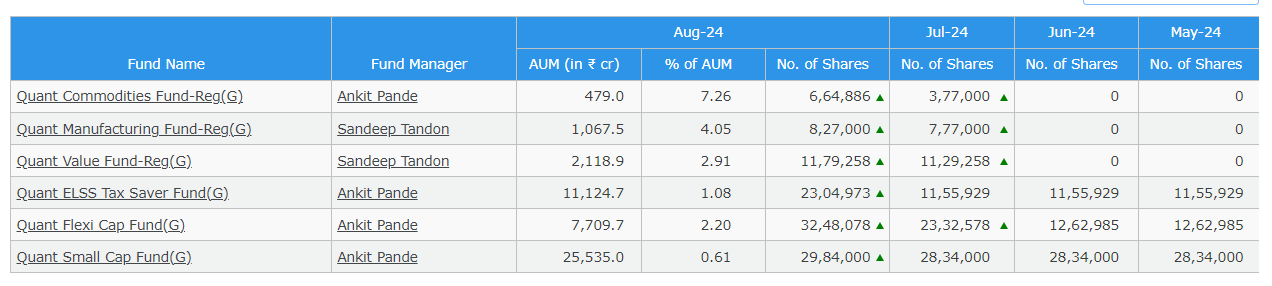

Additionally, Many Quant funds hold position in HSCL and all of them increased the stake in August.

Discl: Remain Invested. Invested @490 Levels.

Titan Company Ltd : a three decade old company (07-10-2024)

Both Titan and Kalyan have shared their business updates. I have compared Tanishq Jewellery(Tanishq, Mia and Caratlane) with Kalyan(Kalyan, Candere)

Tanishq & Kalyan: Q2FY25 Business Highlights

Tanishq Jewellery (Titan Company Limited) and Kalyan Jewellers both reported strong Q2FY25 results. Let’s examine their performance, focusing on revenue growth and expansion strategies.

Revenue Growth Sparkles ![]()

Both companies thrived in Q2FY25, capitalizing on increased consumer spending after India reduced the custom duty on gold imports. Here’s a closer look:

| Metric | Tanishq Jewellery (Titan) | Kalyan Jewellers | |

|---|---|---|---|

| Consolidated Revenue Growth (YoY) | 26% | 37% | |

| India Jewellery Revenue Growth (YoY) | 25% | 39% | |

| SSSG | Mid Teens | 23% |

- Kalyan Jewellers achieved higher overall revenue and same-store-sales growth than Tanishq Jewellery.

- The reduction in gold import duty significantly boosted demand for both companies, highlighting the sensitivity of the jewellery market to gold pricing.

Expanding their Footprint ![]()

Both companies strategically expanded their store networks in Q2FY25, primarily in India:

| Detail | Tanishq Jewellery (Titan) | Kalyan Jewellers |

|---|---|---|

| Total New Stores (Jewellery, net) | 34 | 27 |

| Breakdown | 11 Tanishq, 11 Mia (India), 1 Mia (Abu Dhabi), 11 CaratLane | 15 Kalyan, 12 Candere |

| Strategy | Multi-brand approach targeting diverse demographics and price points. | Focus on the Kalyan brand with a growing franchise-owned-company-operated (“FOCO”) model. |

| Total Stores (as of Sept 2024) | 1,009 (723 Tanishq & Mia, 286 CaratLane) | 303 (231 Kalyan India, 36 Kalyan Middle East, 36 Candere) |

- Titan’s multi-brand strategy allows them to capture a wider customer base.

- Kalyan’s FOCO model could enable faster expansion with potentially lower capital investment.

Digital Dominance ![]()

Both companies experienced considerable growth in their digital first platforms:

- CaratLane (Titan): Recorded c. 28% YoY growth.

- Candere (Kalyan): Achieved approximately 30% YoY growth.

.

Conclusion:

This quarter has been good for both the companies. With festive season coming Q3 is generally best quarter for jewellery market.

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (07-10-2024)

Typically Q4 is where the company gets almost 40-60% of their Revenue. And according to the calculation I did (based on their orders) they can achieve this 2000 crores Revenue.

I feel they will achieve this 2000 crores target based on the order they have

Even though I have invested in this company (1%), still I don’t get the confidence in the promoters as I feel they aren’t able to deliver what they have promised (EV Vehicle) on time (2022). Also, I feel recently there is no new announcement of orders which is What worrying me the most as their competitors are getting some order every month

SBFC Finance – a stable lender? (07-10-2024)

Hello,

I am new to this website and am writing to start a discussion on SBFC Finance.

Started by bankers who have worked across many private sector banks (Kotak, HDFC etc.) the company seems to be tapping into a need in India – Finance to manage cash flows/ start a business. (Ticket size for loans: 7-20Lakhs)

This seems very stable as the loan is to facilitate business cash flows and backed by the lendees home as a collateral.

Moreover, the company has a wide spread distribution network and is currently focussing on sweating the current assets to increase loans/ center. (could possibly lead to increased RoE over the next few years).

In comparison to Five start business, SBFC is targeting slightly higher ticket size of loans. (Possibly more stable and secure target market).

There seems to be a long runway for this company considering that in India : rural, semi-urban areas have self-employed business, self-employed agriculture as a great proportion of the sources of income. Moreover, consistent NPAs (low) are also promising (Loans are backed by the lendees home as collateral; Wife/husband is a co-signee).

My question is regarding the very volatile nature of this stock in the last couple of months. Any ideas as to what are others seeing which we may be missing? Why are bulls and bears having a n intense go at this one?

Thank you

Bhansali Engineering Polymers – An Import Substitution Story! (07-10-2024)

I actually have a very basic question wrt oversupply.

- Total import substitution demand is 175 kTPA and say, the market will grow by 7-8% and the demand will reach 200 kT by 2026

- Now, the new facilities coming online are 300kTPA – 100k (Styrenex), 80k (Supreme), 125k (Bhansali eng). Basically, a 100k oversupply

- Another factor is threat of imports. Custom duty on ABS is just 6-6.5% and there’re low cost producers in nearby countries. Also, China’s demand is 5 mil T (14x), meaning even a small drop in demand there could lead to dumping in India. The situation is too predicated on things going exactly right for sales improvement.

Also, the company’s margins significantly higher Styrenix since FY24, which wasn’t the case in FY23. If someone can shed some light on this.

Rural Elect Corp (07-10-2024)

No absolutely agree on that Sunil.

The challenge is that as per revised norms RBI reuires 5% upfront provisioning – the the point of disbursement. That on a perfectly fine/healthy loan. See ECL model is based on “Expected credit loss” – so you make sufficient provision on the day any loan gets delayed or gets pushed into SMA 2. But the revised norms earlier suggested by RBI are beyond onerous.

The disclosures historically have been quite good as the management has always shared specific project details on NPAs etc. Also under no circumstances can a company keep classifiying a project as an NPA if it stops paying given all this is now much closely monitored by RBI.

To you earlier point reversal of provisions – these loans are of longer duration – 5/10Y – introducing such lumpiness creates a situation wherethese companies will start reporting EV/VNB like metrics in growth phase which doesnt make sense per my view.