@Anna, I wanted to ask who the DLT partners are for Airtel and Jio, similar to Tanla for Vi. Do you think the URL whitelisting rule will help Tanla gain market share, especially with the rush to register URLs? Also, it seems like funding in the sector has dried up, which I think might be a good thing—what’s your take on that? Lastly, do you think Airtel will have an edge over OTT messaging, like they do with SMS? I feel the market is going to shift dramatically from SMS to OTT, and India seems like a massive opportunity—for instance, WhatsApp has the most active users here. Too many questions, I know ![]()

Posts tagged Value Pickr

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (05-10-2024)

SG Mart- Can it successfully create a marketplace? (05-10-2024)

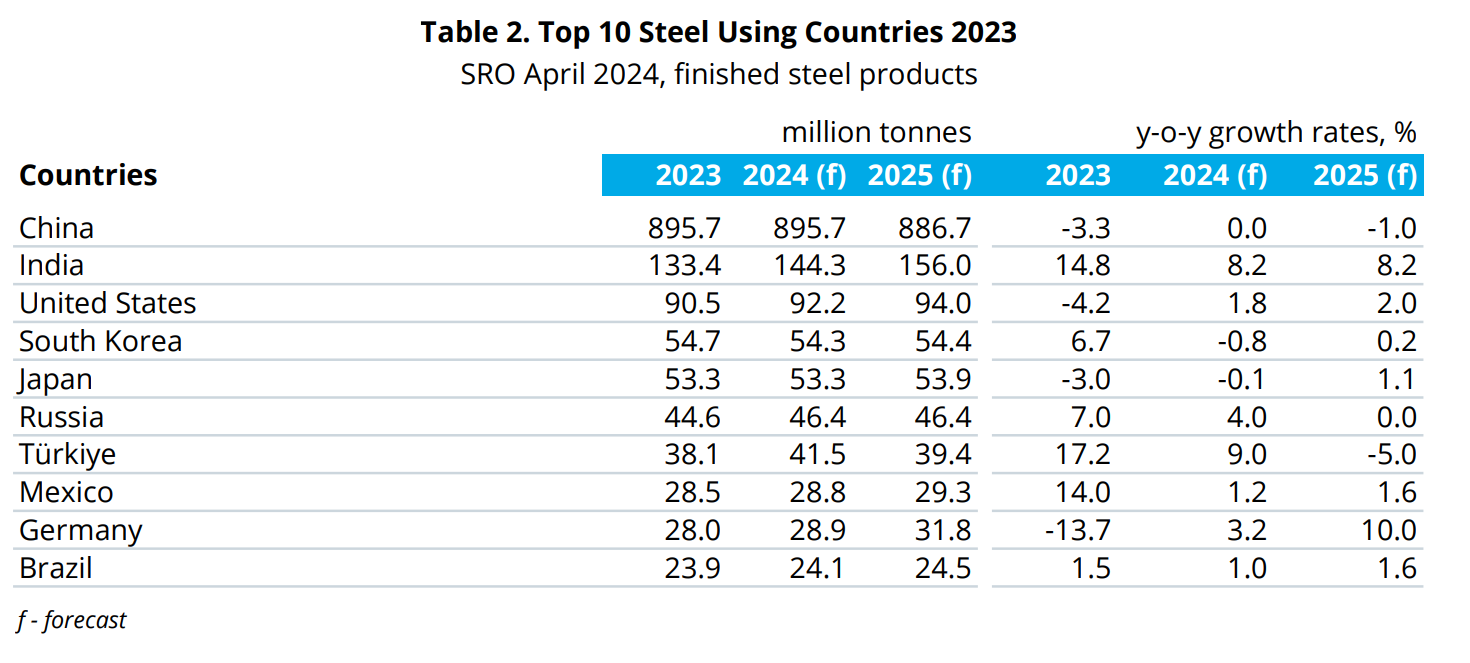

- To some extent I agree that Indian steel demand is greater than Japan and will outpace it easily. The core problem is that any company can enter into this sector and cause competitive margin erosion. I disagree with the company’s claim that there’s little to no competition – see Ofbusiness, Infra.market, Shankara, etc who have the money and can easily enter into this market

- Japan trading companies are the biggest customers for steel manufacturers. SG suddenly doesn’t become the biggest client. They’re hoping that being an Indian player would give them bargaining power since Marubeni (biggest steel trader) for example has the luxury to buy in 50 countries and buy from the lowest priced provider

- There’s no govt approval needed for trading in steel. I hope you’re not just copy pasting from chatGPT

- Even biggest steel manufacturers aren’t safe from steel fluctuations. Any issues in credit lines, working capital shortage will lead to inventory costs. India has become a net importer of steel, even with tariffs imports are cheaper – https://www.reuters.com/markets/commodities/indian-steelmakers-seek-higher-tariffs-chinese-imports-surge-2024-09-26/

- Demand is definitely there in India and SG can grab a huge chunk of the pie and I am bullish on their prospects. My major concern is valuations here → no margin of safety and no barriers to entry.

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

I Compared current Samhi valuation w.r.t. its turnover of the acquired entity.

Samhi: FY24/Market Cap= ~22%

FY24- 957

Market Cap: 4,308

New acquired Entity: FY24/Market Cap= ~12%

FY24- 24.7

Market Cap: 205

Rooms: 142

Assuming, they can double the rooms the revenue/market cap will be in line with Samhi.

(I know it will involve further cost addition to construct rooms but significant cost is land , as Bangalore real estate prices skyrocketed in last 3 years, especially in Whitefield)

It’s fair valuation.

Hope it helps

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

MERGER & ACQUISITION

Acquiring 100% of Innmar-Tourism and Hotels Pvt Ltd for an EV of INR 205 Cr. Company owns an operating hotel with 142 rooms in Whitefield, Bangalore along with surplus land for development of an additional 200-220 rooms in the Upper Upscale segment. The company did a turnover of 24 Cr in Fy24 & Fy23.

Valuation: The acquisition has taken place at a EV/S of 8.5x. Currently SAMHI is trading at EV of 6300 with 957Cr sales in Fy24, hence implied EV/Sales is 6.6x.

The revenue per key for the Innmar in Fy24 is 17.5 lakhs. For an upper upscale segment it seems to be quite low for a hotel located at one of the major city. In contrast the upper upscale revenue per keys for SAMHI portfolio of same category is ~39 lakhs. One probability for low rev is maybe the hotel is upper mid scale category, in a similar case Samhi has ~20lakh rev per keys.

Antony Waste – Long Term (05-10-2024)

Yeah, its nice that they again won the contract. But, I’m not sure if there will be any incremental revenue since it was an ongoing contract. Its more like a renewal.

Shivalik Bimetal Controls Ltd (SBCL) (05-10-2024)

Assuming it is a customer ask, it is safe to assume there’ll be strict manufacturing/ testing requirements.

What are the typical approval timelines for such integration, does it go for years as most of these are design once and run without any change for atleast a decade kind of stuff.

As far as my very little knowledge goes, even an existing end-customer uses a similar/same current sensing PCB module across models, so what they use today was designed/integrated atleast a decade earlier and seldom if ever changes.

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

Hi Ayush

Would like to understand how do you mean ~2x valuation. Looking at screener PE or PEG is not available. Could you please explain that a bit?

Samhi Hotels – Turnaround with Tailwinds (05-10-2024)

It’s nearly ~2x valuation (if compared to current market cap).

But considering they plan to double the room count(of acquired entity) and Bangalore land prices increased significantly in past couple years. Seems fair valuation.

Burger King ~ Whopper of an Opportunity (05-10-2024)

Yeah I get that but

Considering the amount written off in P&l is way too high.

They have assets of 2300cr only and dep is 350 cr.

Where as jubilant has 6000cr of assets and dep exp is only around 170-200cr.

Compare it with other QSRs also its way too high!!