Posts tagged Value Pickr

Coastal Corp. ~2.5x capacity exp. 4x profits? Downcycle a risk (05-10-2024)

By ship only, it takes more than 30days for transist.

I heard in some concalls that US freight cost was not much impacted in the past few quarters due to containers unavailability.

Srestha Finvest Ltd: A Strategic Shift Towards Green Finance and Sustainable financing (05-10-2024)

The company is trying again for fund raise and the same will be discussed in the next board meeting on 9th Oct. Let’s support them in fund raise this time.

SG Mart- Can it successfully create a marketplace? (05-10-2024)

Nice points, but to compare a company’s potential in India (where no such big aggregator like SG Mart currently exists) to those of Japan and Eu where this has been a norm since a long-long time now in such a simple and straight-forward way would not be the most accurate thing to do, in my opinion.

Both the countries are at much different stages of growth and development in terms of infrastructure. Even the mere sizes of both countries are vastly different (both in terms of land area and population).

So to answer your 1st question: How come SG Mart would be able to achieve 30,000 Cr in sales when half of these giant companies barely reach that number?

1. Growth in India’s Infrastructure Market:

India’s infrastructure market is growing at a significant pace compared to developed nations like Japan and the EU. According to the National Infrastructure Pipeline (NIP), the Indian government plans to invest ₹111 lakh crore (~1.5 trillion USD) by 2025. This massive investment spans sectors such as energy, railways, roads, urban infrastructure, and water supply.

- Construction & Steel Industry Demand: India is expected to become the second-largest steel consumer in the world after China by 2025, thanks to rapid urbanization, industrialization, and government projects such as Bharatmala (road construction), Sagarmala (port development), and the Smart Cities Mission.

- GDP Growth & Market Potential: India’s GDP is projected to grow at a rate of 6-7% annually, while Japan and the EU are expected to have lower growth rates (Japan’s GDP growth has been stagnant at 1% or lower).

2. Scale of Indian Companies vs Global Competitors:

Indian companies, especially infrastructure-focused entities, have room for significant scale-up. For example, the Indian steel industry is growing steadily, with companies like JSW Steel and Tata Steel seeing substantial growth in production and exports. JSW Steel’s revenue crossed ₹1.46 lakh crore in FY23, showcasing that Indian firms can indeed achieve a scale of 30,000 Cr or more in sales.

- Japanese companies like Mitsubishi and Marubeni operate in mature, saturated markets, which explains their relatively lower growth rates. SG Mart, operating in a fast-growing market like India, has a competitive advantage in capitalizing on the infrastructure boom.

3. Competitive Landscape in India vs Japan:

While competition would inevitably enter the market, India’s infrastructure needs are massive and still evolving, offering much more headroom for growth compared to Japan, where growth is limited by market saturation. New entrants or competitors in India would face high barriers to entry, including large capital investments and government approvals. On the other hand, India’s infrastructure growth plans suggest that existing companies can still absorb significant growth before market saturation occurs.

Question 2: Sales realizations and fluctuating margins (especially with steel prices) – how can SG Mart sustain its working capital cycle?

1. Steel Price Fluctuations:

Steel prices are inherently volatile and are influenced by global supply-demand dynamics. In the case of India, though, this fluctuation can be mitigated by:

- India’s Hedging Mechanisms: Indian companies are increasingly adopting hedging strategies to protect against the volatility of steel prices and global market fluctuations. The Indian government has also been imposing tariffs and anti-dumping measures to stabilize the domestic market.

- Internal Market Demand: Domestic demand for steel and other raw materials is expected to grow substantially, driven by the urbanization and infrastructure boom. The internal consumption buffer means that Indian companies like SG Mart would not be solely dependent on export markets or fluctuating global prices.

2. Efficient Supply Chain Management & Capex Spending:

Many Indian infrastructure companies have optimized their working capital cycle by leveraging better supply chain management, cutting lead times, and improving logistics. SG Mart can also take advantage of this by streamlining its operations and reducing unnecessary costs. Moreover, as infrastructure projects get prioritized (e.g., dedicated freight corridors), companies will benefit from faster project completions, reducing the strain on working capital.

3. Infrastructure Improvement Opportunities in India:

India’s underdeveloped logistics and transportation sectors provide a strong case for improvements in efficiency. For example, investments in roadways, ports, and airports are expected to reduce transportation costs significantly, which is currently much higher in India than in developed countries.

Scope of Improvement in India vs Developed Nations:

- India: Huge opportunities exist in building new infrastructure (transportation, energy, etc.), creating room for significant sales growth in construction materials, including steel. With a younger population, economic growth, and substantial government support, India’s infrastructure needs are far from being met.

- Japan and EU: These regions are in a stage of infrastructure renewal and maintenance rather than new development. This leads to lower growth potential in the construction materials sector, which is why companies like Marubeni and Mitsubishi have slower revenue growth.

So, long story short:

- SG Mart’s 30,000 Cr target is achievable, given the growth trajectory of India’s infrastructure market and the increasing demand for materials like steel.

- Sustaining margins will require strong hedging strategies, improved supply chains, and benefiting from India’s internal market, which provides resilience against global price fluctuations.

India’s underdeveloped infrastructure presents far more opportunities for growth than the saturated markets in Japan and the EU, giving SG Mart a solid base for scaling up.

Praveen’s portfolio (Coffee Can) (05-10-2024)

Can you please let me know reason for taking “TALBROS ENGINEERING”? What is the current status, do you still hold or sold?

Megatherm – Mega Opportunity (05-10-2024)

Your understanding is exactly correct. I got IPO allotment in the company but wanted to research more for increasing the position size. I had a talk with their IR team, and they’re targeting 500cr revenue by 2030 I think.

The reason they’re expanding into transformers and other markets is bcz the size of Furnace market isn’t large. Most steel companies use BOF method bcz the quality produced is better. More importantly the entire steel industry is undergoing a CAPEX right now, which means this is the best time for the company but still most expansion is happening through BOF route. Tata Steel tried to get a plant in UK switch to EAFs but they’re facing huge protests.

Overall, I think the promoters are really honest and diligent so if they figure something out by cracking new product lines, that could be great. But the total market size of the business is extremely small. Infact, total size for EAFs is around 700cr out of which megatherm takes around 160cr, electrotherm takes 200cr and a few other players occupy the market and there isn’t much scope for expansion/growth.

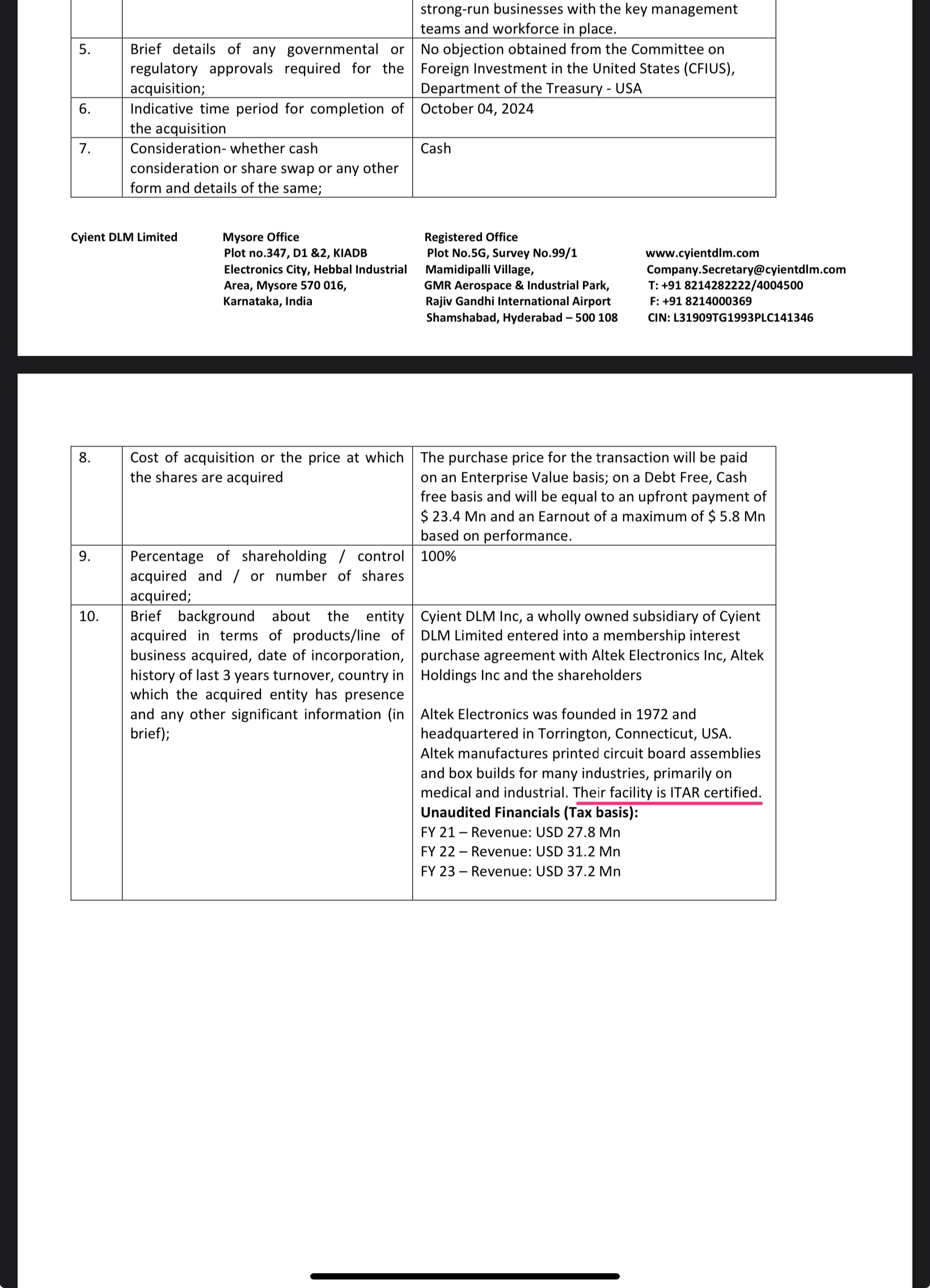

Cyient DLM Limited (05-10-2024)

Cyient DLM acquires a US based EMS company Altek Electronics. They are operational in the healthcare and industrial segments and more importantly has ITAR ( International traffic in Arms regulation) certification which enables Cyient to supply to the US military .

Disc: Invested.

SG Mart- Can it successfully create a marketplace? (05-10-2024)

I see SG Mart a bit differently, Infra market is getting ready for the IPO, during last round they raised funding at $2.5 billion in May’24, per the articles the IPO would be at higher valuations than last round. Infra Market had a revenue of ~12k crores in FY2023 and PAT of 155 crores which is expected to grow at 15% to 20% in FY2024 (~10k crores in first 9 months of FY2024), company’s working capital days are longer as it extends credit by itself(company’s net debt at the end of Dec’2024 was ~2.8k crores) and its liquidity was marked as weak during the latest rating by the rating agency. SG mart can generate ~6k crores of revenue in the current year with PAT crossing 100 crores and with better working capital management (because the credit days are extended through SG finserve just like in case of Off Market), SG Mart can have at least half of the market cap (~12k crores to ~15k crores) that Infra Market will demand. I may be wrong but risk reward seems reasonable from here.

X- @amitsinghpal

My Portfolio (Updates and Suggestions) (05-10-2024)

I am waiting for more correction to take entry! ![]()

![]()