Could you please share an updated Google Sheet of the microcap momentum portfolio? I have been trying to create a sheet, but I’m having difficulty. It would be a great help to us if you could share a sheet.

Posts tagged Value Pickr

VVIP Infratech LTD (02-10-2024)

VVIP Infratech Ltd

Mcap: 559cr

P/E: 27

ROCE: 22.6%

ROE: 21%

Debt to equity: 0.4

CMP:224

Promoter holding: ~68%

Introduction:

VVIP Infratech Limited, originally incorporated as Vibhor Builders Private Limited, is an infrastructure company established in 2001.

The company mainly works on projects in Uttar Pradesh, Uttarakhand, NCR Delhi, and other northern parts of India. It is a Class ‘A’ civil and electrical contractor with more than two decades of experience in the execution and construction of infrastructure projects like sewerage, sewage treatment plants, water tanks, water treatment plants, sector development works, power distribution and substations up to 33 kVA, Jal Jeewan Mission etc.

Water Treatment Business

Co. engages in sludge treatment and disposal. It forms a Joint Venture with other companies and bids for Government Projects.

As of FY24, Co. has 5 Joint Ventures which have 4 Ongoing Projects, and completed 9 Projects

Real Estate Business

Company owns 90.02% shareholding in its subsidiary, Vibhor Vaibhav Infrahome Private Limited (VVIHPL) which serves as the real estate arm of the group.

Co. has built 12 Residential/Commercial Projects with a total saleable area of 54,44,600 sq. ft.

** Standalone Revenue Bifurcation – Segment-wise

- Pipeline, Tube Well & Water Tank: 20.70%

- Sewer Work & Treatment Plant Work: 74.72%

- Electric Work: 2.60%

- Operation & Maintenance STP: 2.05%

- Pool & Boundary Wall Work: 0.01%

- Material & Scrap Sale:** 0.03%

Geographical Presence The company works on projects in Uttar Pradesh, Uttarakhand, NCR Delhi, and other northern parts of India

The company listed on 30th July 2024.

The company intends to utilize the proceeds of the Issue to meet the following objectives: ( ~61cr)

Capital Expenditure: ~10cr

Working Capital Requirement: ~40cr

General Corporate Purpose + Issue Expense: remaining proceeds

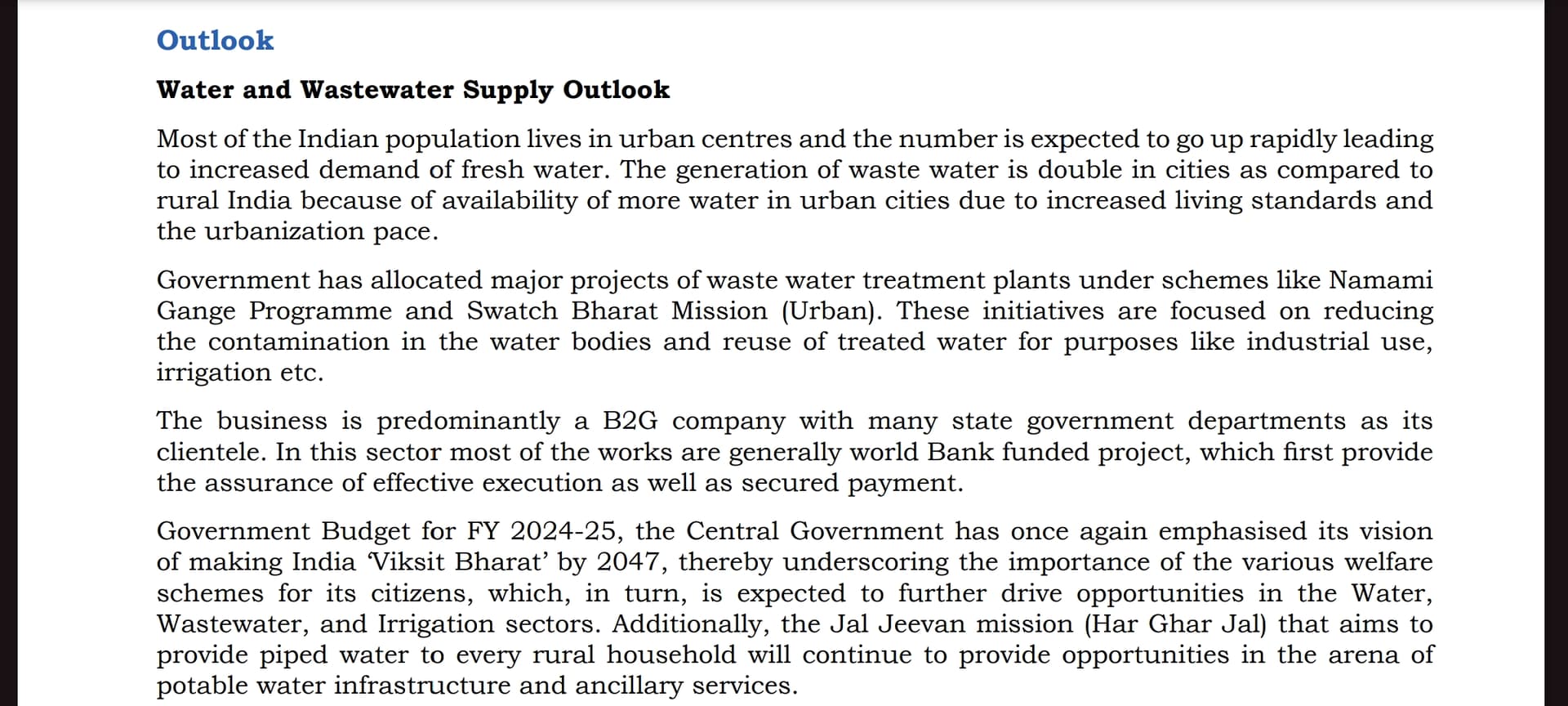

Sector and industry overview:

Wastewater treatment and recovery are critical to address water scarcity and environmental pollution.

While the country clearly needs to increase its treatment capacity, it also needs to upgrade the currently employed wastewater treatment processes for more efficient technologies.

Now, a new report by the Council on Energy, Environment and Water (CEEW), states that 80% of wastewater generated by urban India has the potential to be treated and reused for non-potable purposes like irrigation, which can relieve the immense pressure on water bodies, lower pollution levels and provide water security in the face of climate crisis-induced weather events that can render water bodies unreliable.

Pm Narendra Modi’s video on mission Amrit which focuses on water and sewage treatment:

PM Modi announces ‘Mission Amrit’, to setup water and sewage treatment plants in cities

From ems annual report:

From Vishnu Prakash R Punglia Ltd investor presentation:

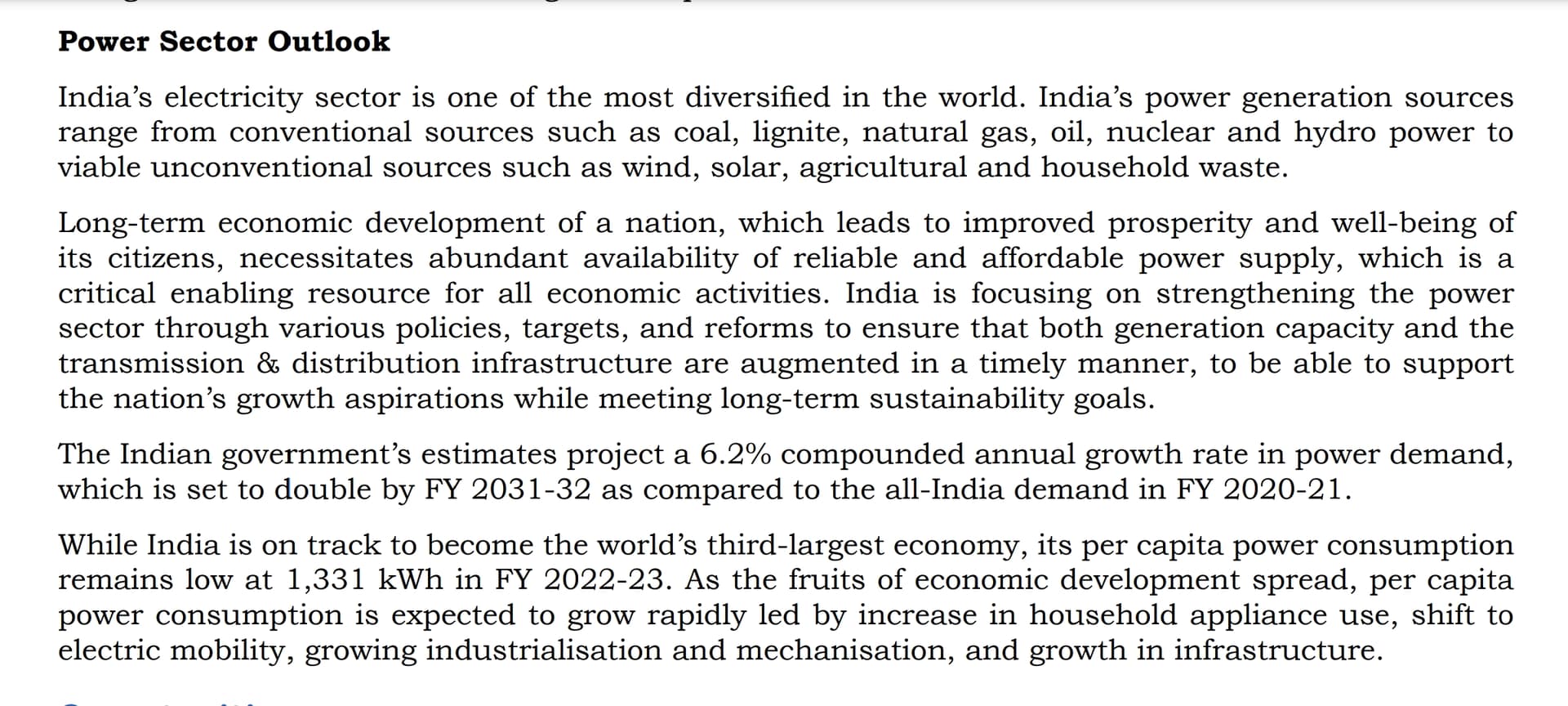

VVIP along with sewage and water treatment also does projects of electrical distribution, transmission

India’s transmission segment has undergone a significant transformation over the years, transitioning from a fragmented network to a well integrated and interconnected grid. The segment has taken significant strides in expanding the physical infrastructure of the grid and consolidating it into one of the largest synchronous grids globally. Looking ahead, as India aims to meet 50 per cent of its generation capacity from non-fossil fuel sources by 2030, and given the rising significance of electricity in the nation’s energy mix, substantial investments will be imperative in both the inter-state and intrastate transmission networks.

~taken from powerline website

One can go through the ministry of power website if he wants to deeply understand this sector.

Taken from ems annual report:

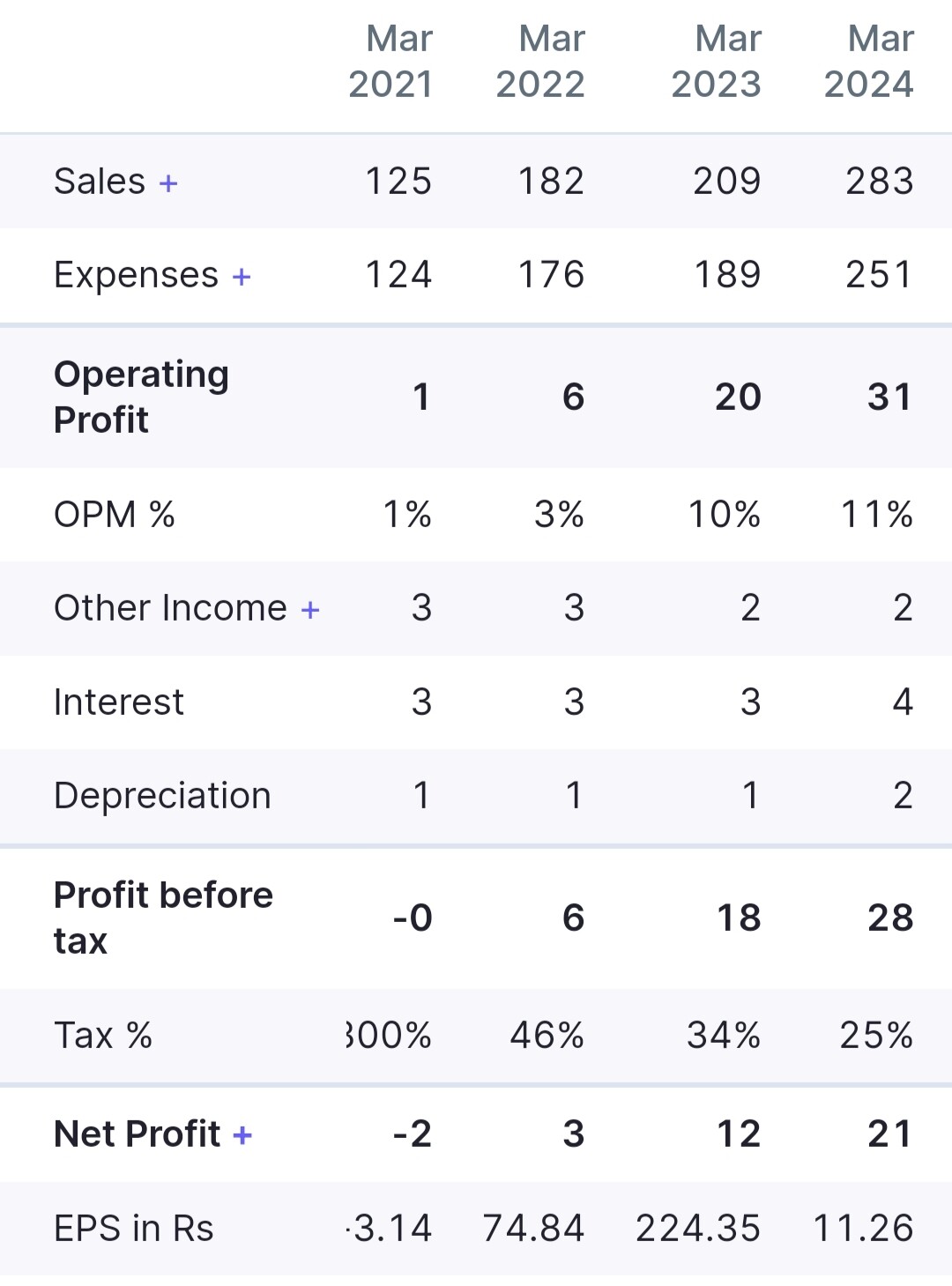

Financial statements:

P&l

Balance sheet

Cash flow statement

Peers:

EMS

V.L.Infraprojects

Vishnu Prakash R Punglia

RPP Infra Projects

Valuation:

Market cap to sales ratio: ~2

Pe ratio: 27

Market cap to order book ratio: ~0.84

Management:

Praveen Tyagi (Chairman), is the Promoter and Director of our Company and founder of VVIP Group. He has completed Diploma in Civil Engineering by DN Polytechnic, Meerut and engaged in the business of civil construction and infrastructure development for more than three decades. He is a first generation entrepreneur and started his career as a civil contractor in the year 1991. Initially he started business in Proprietorship firm. Later, he formed incorporated a Private Company in the year 2001. Vaibhav and Vibhor Tyagi are his two sons.

Vaibhav Tyagi, (MD) Managing Director and Promoter of our company. He has completed Bachelor of Business Administration and joined the Infrastructure Business of the group around eight years back in the year 2015. He is entrusted with the responsibility of managing the overall affairs of the Infra Company of the group. He is instrumental in entering into Jal Jeewan Mission work of the company. He is fully involved in getting the work executed at sites, liasioning with departments and working on new tenders.

Vibhor Tyagi,(Whole time Director) Whole Time Director and Promoter of our Company. He holds a Bachelor of Business Administration (Marketing) from Eastern Institute for Integrated Learning in Management University, Sikkim. He joined the company ten years ago and is actively involved in real estate business of the group.

Management interviews:

Inside VVIP Infratech Limited: A Comprehensive Exploration

VVIP Infratech Limited: Redefining Infrastructure With Passionate Progress.

Biz Talk With Don – VVIP Infratech Limited

Investment thesis / key triggers/ positives

- Total order book of ~665cr which is to be executed within 18-24 months. Recent order:

16a2d441-cdde-4460-ac04-a70e3bfb4960 (1).pdf (602.8 KB)

2.strong revenue growth of 30% +cagr (3 years) and strong bottomline growth. Management giving guidance that on a conservative side they will do 30-35% cagr growth in the coming 3-4 years.

-

Huge tailwinds for sewage and water treatment sector. Pm modi announces mission Amrit. Strong budget allocation towards water, infrastructure and towards electrification.

-

The management seems clean, wasn’t able to dig up any red flags on them.

-

Healthy operating cash flows is an extremely green flag especially in this sector as it is a b2g sector and compared to its peers its cash flows are phenomenal.

-

Capex requirements are lower because the management’s strategy is to lease a part of equipments required as it is more convenient physically and economically both. This may lead to an asset light model which may give benefits to the company in the future.

-

Deleveraging is also at play here, the company has been reducing long term borrowings.

-

Most of the projects are funded by central government, chances of bad debts is extremely low.

Risks

-

The major risk here is the execution risk, whether the company will be able to deliver its projects on time.

-

B2G and receivables risk.

-

as it’s a sme company there are volatility, liquidity, regulatory (exchange risks) . One may loose 100% of their capital investing in sme / microcaps due to their small size and in general volatile nature.

-

Raw material risk is there but the company has escalation clauses for it (got this information from the credit report).

Disclosure: not registered with sebi,

Not a buy/ sell recommendation

Invested.

Zomato – Should you order? (02-10-2024)

Can anyone tell me what on the earth stops Flipkart, Amazon, bigbasket, swiggy, zepto becoming another blinkit. What is the moat here.

Angel One: Metamorphosis into a Fintech? (Previously Angel Broking) (02-10-2024)

Key points in SEBI mandate

—> No Daily expiries (One expiry per week/exchange)

—> Contract size to triple

—> Calendar spread margin

First two points would negatively impact the F&O participation from where the major revenue comes from.

This will prove to be a double whammy from brokers stocks. First due to lower EPS, second due to P/E contraction.

Assuming no P/E contraction, since Angel One’s PE is already low, I am a expecting 20-30% correction from here.

References:

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (02-10-2024)

My understanding is that SP group wanted to invest in the SW data center business (not related to SWRE) through the current stake sale.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (02-10-2024)

How to speak without giving any information. One should really watch the interview.

Very very primitive answers given about debt reduction, low revenue and low ebitda margins. “Log responsible ho gye h, election me”. Also not sure if banquet halls are newly added or he is just saying that there is trend to do marriages in hotels now. (Which I would say is not a new trend).

Also mentioned that they are opening their pure veg restaurant in every hotel. Again unsure if this is new or the restaurants already exist. Also mentioned that their restaurants are famous. And also made a weird point about people want to eat in clean restaurants after covid.

If the stock wasn’t at a good support zone technically, I would have made a full exit in loss.

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (02-10-2024)

the long term debt of SW solar was of the order of 240 cr only till march.

What is the 750 crore debt which was supposed to be paid of?

I saw there were some unexplained huge current liabilities in the balance sheet.

(b) Other current liabilities 28 946.31

Is this the one for Data center?