Notes from 22 Sep 2024 Tiger Conclave investor meet [more clarity to what is already well covered by Dhruv above]:

- Out of 1 lac crores per year opportunity, they qualify for 90k crore due to their pre qualification i.e. PQ (past experience etc):

- River to reservoir (bulk): 45% of opportunity- This is where SPML Infra operates

- Reservoir to tap (distribution): 35%

- Tap to river (sewage): balance

- Out of this opportunity, targeting only 5-7k crore order book:

- Highly profitable ones (EBIDTA: 12-15%)

- Funded by world-bank, JICA, jal jeevan [so that no possibility of these earmarked funds being diverted to vote bank as done earlier]

- Almost no working capital with vendors- No advance / LC required

[reminds me of Shakti Pumps when they rejected to work with states having weak funding; likewise SPML is learning from it’s mistakes and instead of being too aggressive with Govt biz by targeting complete 45k crore opportunity, they want to target only highly profitable, less competitive orders, funded projects]

- Right to win:

- Only 4 players have PQ for bigger contracts: Regulatory sorts of barrier

- Per management, would take 5 years for anyone new to gain PQ

[thesis can be relooked post 3 years, or whenever competitive intensity increases. While it may be a mere EPC co, any other EPC co even with stronger balance sheet can’t enter like it recently happened with solar, construction EPC et al]

- They would partner with credible EPC companies for project execution and charge 2.5% of order value which would flow directly to PAT

[would it make their partner EPC co, which are currently ineligible to bid due to insufficient PQ, gain PQ and bid on their own in future? It is inevitable: due to size of opportunity, execution is required by many players. If SPML doesn’t partner with them, someone else would] - No capex for 3-4 years (until arbitration money is received)

- Promoter stake, which was reduced (due to sale of stake to lender, NACL), to increase from current 36% to 40% with preferential allotment.

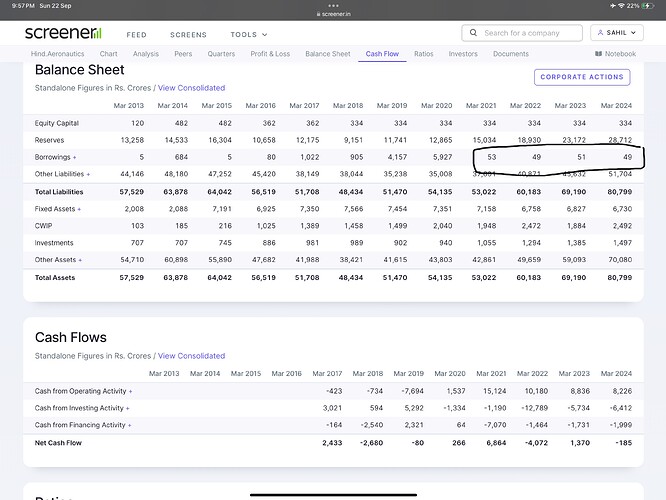

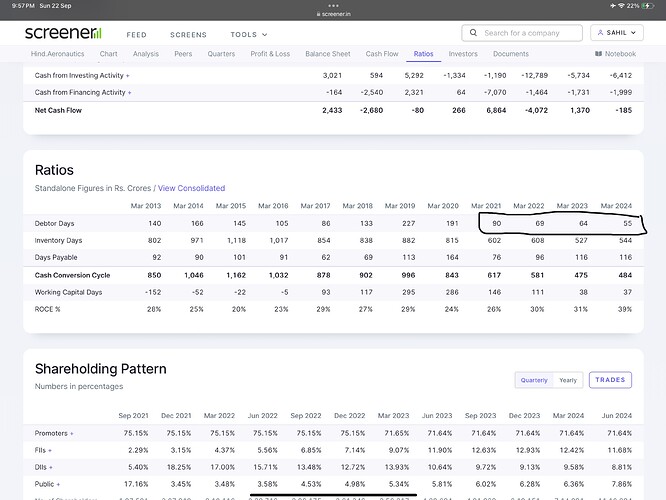

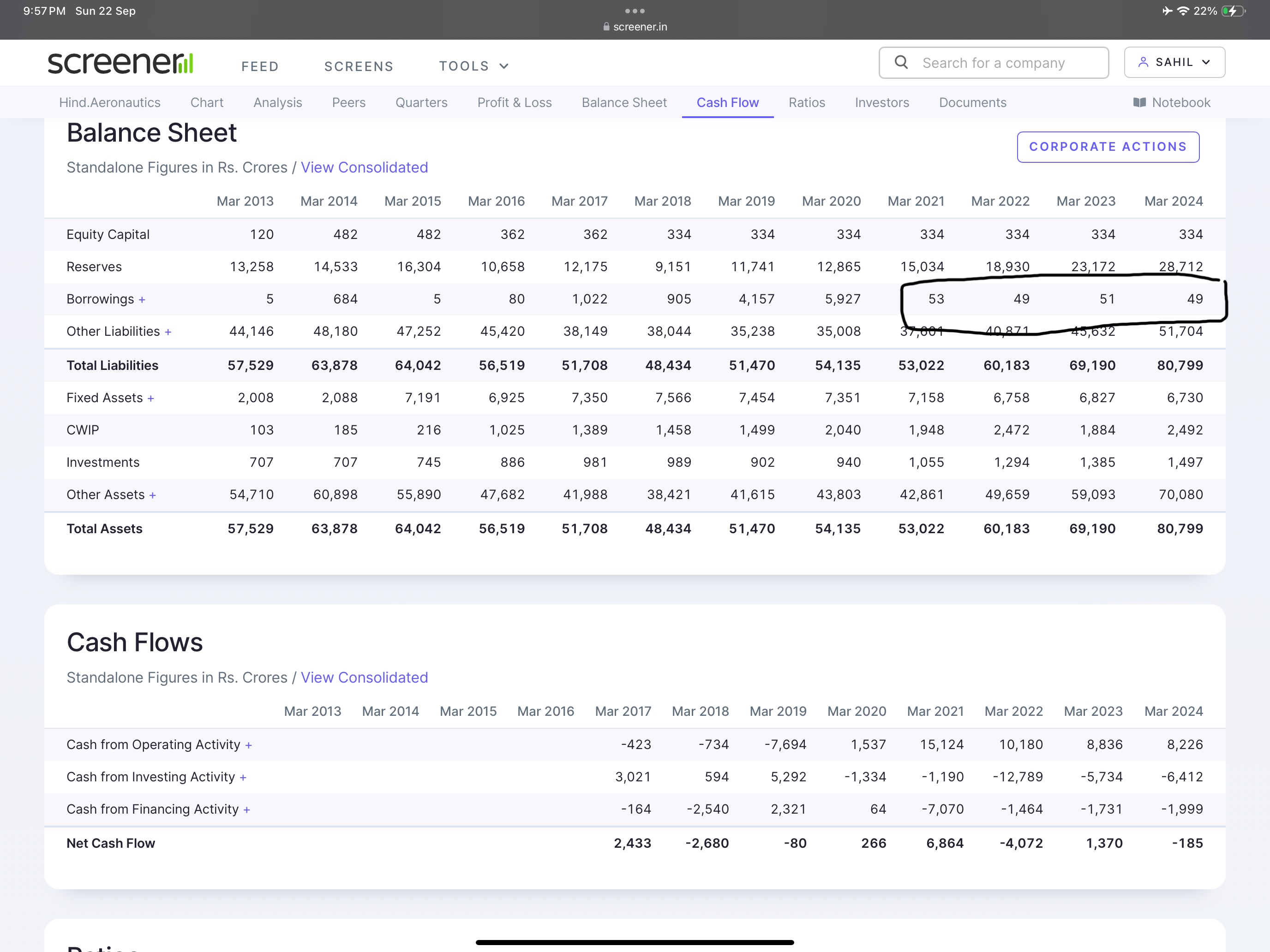

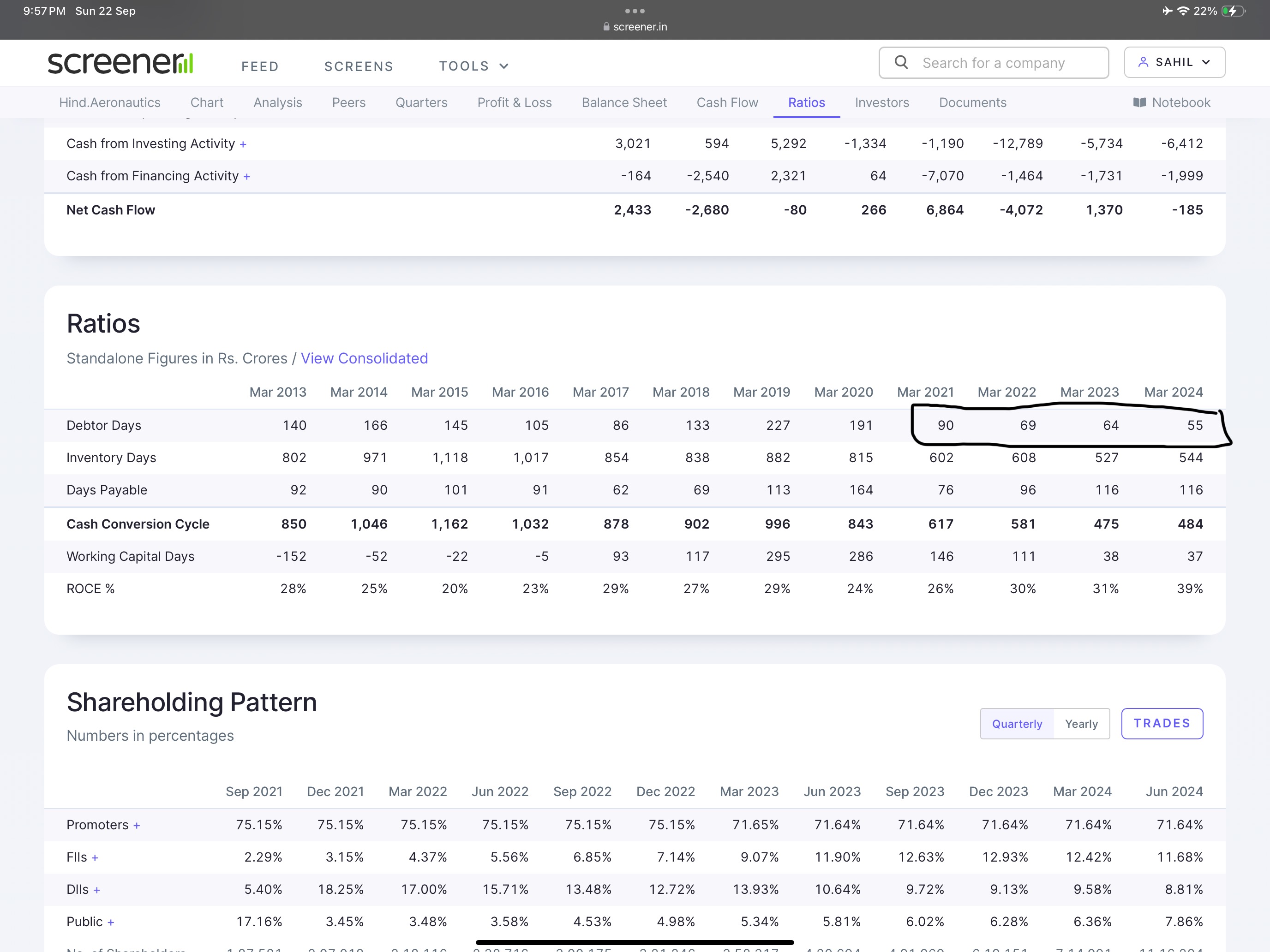

- Looking at SPML, reminds me of Hindustan Aeronautics which became a multi baggier when catalysts entered: debtors which were funded by borrowing started paying off and reduced substantially with Govt focus on defence sector

To monitor:

- PQ isn’t removed as bidding criteria

- Competitive intensity for bigger contracts [players beyond 4]

- Receivables

- Order flow intake

- Transaction with their related party JV partner [JWIL]