Posts tagged Value Pickr

Jash Engineering – Is it a multibagger (19-09-2024)

Let’s talk about some risks:

According to “Simply Wall Street”, it has 1 major and 2 minor risks as follows;

Major Risk: No financial data reported. We can see in Tijori also, no financial information is being updated about the company

Minor risks: 1) Unstable dividend paying track record with dividend experiencing an annual drop of over 20% in the past.

- Shareholders have been diluted in the past year (2.9% increase in shares outstanding). 3) I have seen decrease in promotor holding, is it related to point number 2 ?

Appreciate if any experts can give their views

Disclaimer: Invested and biased

Atma Nirbhar Bharat – Stock opportunities (19-09-2024)

Garden Reach Shipbuilders bags $54-million German order for four more cargo vessels. Govt upgrades Garden reach from B to A category

Now ,There is going to be fire in belly of PSU’s to perform or perish. Recently, there is a policy change with respect to PSU functioning and performance monitoring. The finance ministry would monitor each and every PSU for accountability for its performance and upgrade or down grade a PSU. The grading is in to 4 buckets- A,B,C,D- A is highest and D is lowest. The salary of the board members would depend upon some qualitative and quantitative parameters such as Revenue / execution of orders, profit before tax, Share price in the market , capacity addition and winning competitive orders.

The classification of PSU Maharatna , Nava ratna , Mini Ratna would still continue which would give them financial power to invest , add capacity and decision making ability. This means that even a Maharatna or Navratns company can be downgraded.

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (18-09-2024)

Did anyone visit their plant for EV and/or any idea when their EV will be launched? Gensol has changed launch date multiple times and now it seems a hope story. I am also doubtful on their reverse trike if it will be adopted well. Personally I dont think many people will like this.

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (18-09-2024)

Did anyone visit their plant for EV and/or any idea when their EV will be launched? Gensol has changed launch date multiple times and now it seems a hope story. I am also doubtful on their reverse trike if it will be adopted well. Personally I dont think many people will like this.

Macpower CNC Machines: Manufacturing a Strong Growth? (18-09-2024)

Very important point. But requires a more second and third and fourth order thinking before concluding.

Most critical components ( Machine control unit and control panel or even the spindle in some cases etc ) will always be imported as they are manufactured by 3-4 players top in the world, as well known from the con calls. The rest of the critical parts are being backward integrated slowly but surely ( likes of the telescopic rod, the BED itself, its channels etc which they create using their own machines – thats first hand information of my site visit ). The next major step to backward integration is metal forging that will only be announced in the 35 acre new facility as it requires space and is a specialised unit for a specialised job.

I would not look at the demand supply mismatch as much. Instead i would pay more attention to supply side dominance. Jyoti is not the only player. ACE ( in the unlisted space – IPO coming soon and doing very well with sales over 1250 crores in a year ) is another player doing as much sales as Jyoti and then there are other players who currently don’t seem to be that deeply invested in CNC machines with the likes of Laxmi, Lokesh, but Bharat fridges Warner ( BFWindia.com that no one talks about and doing very well but quietly ) and others but doing a fairly decent job. All Companies will have to continue to do R&D and be quick to pivot to better technologies and materials in this fast paced precision engineering sector to stay relevant 3 to 5 years from now.

I will soon share a report by IMTMA which will show how import in india has increased recently in the last 2 years. See, my scuttle bud activity tells me that the tech for the really high end machines is not up to the mark in india ( at-least thats what the word that is going around in the private players space ) causing private business in really critical applications ( eg. TATA iPhone, all big automobile manufactures etc ) to use imported machines for E.M.S. Or critical parts of the engine respectively. We will have to keep and eye on how import substitution plays out in the next few years ( not quarters ). Having said that we also see public companies with critical applications ( HAL ) issuing new tenders from india players and giving them preference to imported machines. Clearly the government is pushing the indian tool industry for a brighter future of manufacturing in india ( Gujarat vibrant scheme ). While the indian companies are also trying hard to develop better tech with precision with use of better materials ( opening new R&D facilities and tech centres ), Hence a work in progress. Not many reports available for the indian CNC machine industry today, but this is my humble personal assessment.

I have learnt that a small number of players in a supply side dominant industry with big TAM, growing order books and great support from the government don’t usually have a cut throat completion between each other. ( read the book Capital returns by Edward chancellor ). “ The challenge for everyone here is to improve on tech, materials, precision and be relavent in the future to be part of the massive import substitution opportunity in a growing precision manufacturing sector of india.” Its serious business by any means of imagination.

A wise man and my teacher ( Mr. Ishmohit Arora ) once taught us that in long term investing respect your time horizon and in trading respect your stop loss.

Since i am investing here, I am zooming out even further to say With a 2500 capacity at 80% utilisation, 22 lakh average utilisation, and 22% EBITA margins, when i look 2 year forward P.E. I am in Mid teen 2 year forward P.E. Multiple.

It tells me if i am ready to wait it out for two years i should not loose money in the longer run. Thats my risk analysis.

Good luck to everyone on their investments in MACpower cnc.

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (18-09-2024)

Everything is going good except their EV production plans which have got delayed any times. Plus there is market apprehension on the designs. Overall still invested and hopeful

Nazara Technologies (18-09-2024)

Making a hit game is no use if you cannot generate revenue from it. By the way they have 2 hit games that tens of millions of Indians have played. World Cricket Championship 2 and 3. But guess what, it’s useless as it’s a freemium game and the generate close to nil EBITDA from there. It’s E-sports (You definitely have heard of Sportskeeda), Animal Jam is quite famous, Kiddopia is one of the top 3 games in US for children. So all in all they are popular but their revenues need to rise

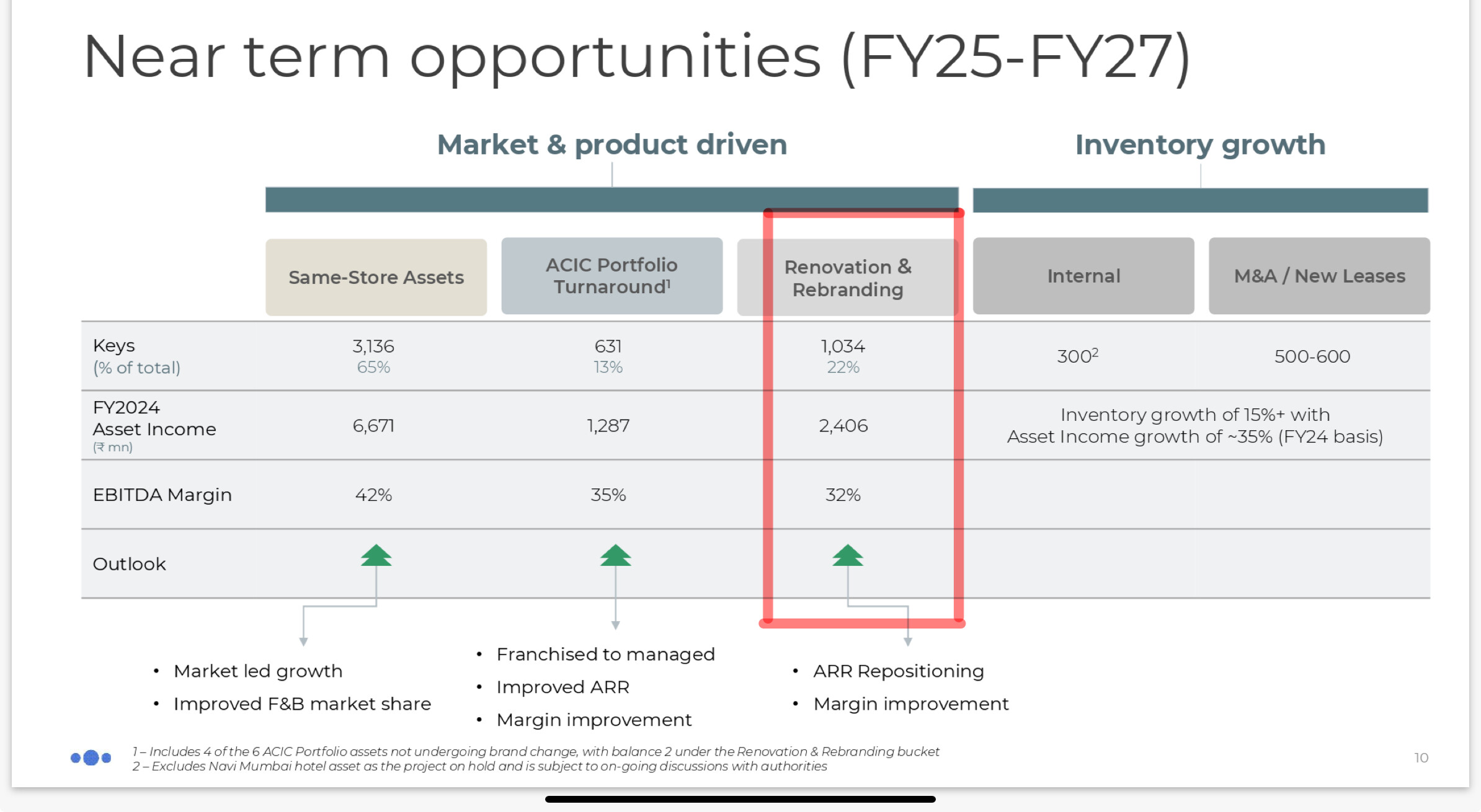

Samhi Hotels – Turnaround with Tailwinds (18-09-2024)

Samhi generates 240 crore from its renovation and rebranding portfolio. However, I am concerned that these activities might disrupt ongoing operations. Could these disruptions result in a significant decrease in revenue of this portfolio until the renovations and rebranding are complete? I am interested in understanding if the rebranding and renovation efforts could temporarily impact this revenue stream.