(post deleted by author)

Posts tagged Value Pickr

Equitas Small Finance Bank: A Profitable lender to small businesses (18-09-2024)

EQUITAS SFB experienced a rise in its GNPA ratio to 2.7% in 1QFY25, driven by increased slippages in the MFI segment (INR850m) and vehicle finance (INR1.5b), pushing the overall slippage ratio to 4.5%, which exceeds the management’s comfort level of 4%.

The stress in the MFI business is widespread across multiple regions, primarily due to over-leveraging issues within the industry. This ongoing stress has impacted profitability and will keep near-term performance in check.

However, with the bank successively reducing the MFI mix to ~17% (from 19% in FY22) and an anticipated recovery in vehicle finance, one can expect the slippage run-rate to ease from 2HFY25 onwards.

The Bank’s ability to swiftly recover from previous credit cycles (e.g., COVID-19, demonetization) with controlled credit costs supports optimism for an improvement in asset quality in the second half of FY25.

Borrower-level indebtedness in the industry has increased swiftly over the past couple of years after the change in guidelines by the RBI. The general level of borrower discipline (as observed in aspects such as center meeting attendance) has steadily declined. However, the industry associations for microfinance are working together to resolve the issue through coordinated efforts and some tightening of credit filters.

Accordingly, Equitas SFB has already implemented the MFIN guardrails as part of its business rule engine in microfinance. Rejection rates are likely to inch up, as all lenders implement these guardrails.

A large share of Equitas’ microfinance business is in Tamil Nadu, Karnataka and Maharashtra. There have been some collection-related challenges in select pockets of Tamil Nadu and Maharashtra. The bank does not have a sizeable microfinance business in the northern part of the country, with some limited presence in Rajasthan. The bank does not have any microfinance business in Bihar.

Management indicated that it does not see any major challenges to its income at the borrower

level. Hence, the company remains hopeful about the microfinance industry stabilizing over the next two quarters.

Credit cost for 1QFY25 was elevated (~3.5% of average gross advances) due to the creation of ~Rs1.8 bn of floating provisions. Excluding this floating provision, credit costs for the quarter stood at ~1.4% of average gross advances.

The creation of the floating provision also helped to reduce net NPA below 1%, which is one of the eligibility criteria for an SFB to transition into a universal bank.

Currently, microfinance is the only unsecured asset product offered by the bank. Over the next year or so, the bank might introduce a few new retail products such as personal loans and credit cards, with the objective of acquiring and retaining more liability customers.

The credit card product is expected to focus primarily on existing-to-bank customers. Even after the addition of personal loans and credit cards, management expects the overall share of unsecured loans to remain at or <20%.

The bank saw a sharp decline in the CASA ratio during the current rate cycle as it declined from a peak of ~52% in March 2022 to ~31% in June 2024.

Management indicated that the bank saw a steady shift in customer deposits from savings account to term deposits during the rate cycle, as the differential in interest rate on incremental term deposit and incremental SA deposit widened sharply.

Some of this shift was also encouraged by bank customer relationship officers to prevent the loss of business to competition. Management is now confident about maintaining the CASA ratio in the range of 30-35% (~31% as of June 2024).

In management’s view, cost of funds remains the biggest risk to the achievement of 1.8-2.0% RoA over the medium term.

Sources: Recent reports from Motilal Oswal and Kotak

Gravita India success story (18-09-2024)

The company is on an investor meet spree for last 2 months.

I’ll look forward to see some new names of institutional investors in shareholding pattern of Sept Quarter.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (18-09-2024)

Yesterday’s interview – https://www.youtube.com/watch?v=IzXC-_aIUzM , CEO mentions Q2 has been “quite good” .

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (18-09-2024)

Will suggest going through their website.

Ola Electric – Full Stack EV play? (18-09-2024)

If numbers are true the monthly issue rate is more than 10% (680,000 units lifetime sales, 80,000 pm complaints), seems pretty high. Is this normal, anyway to benchmark against competitors global or local.

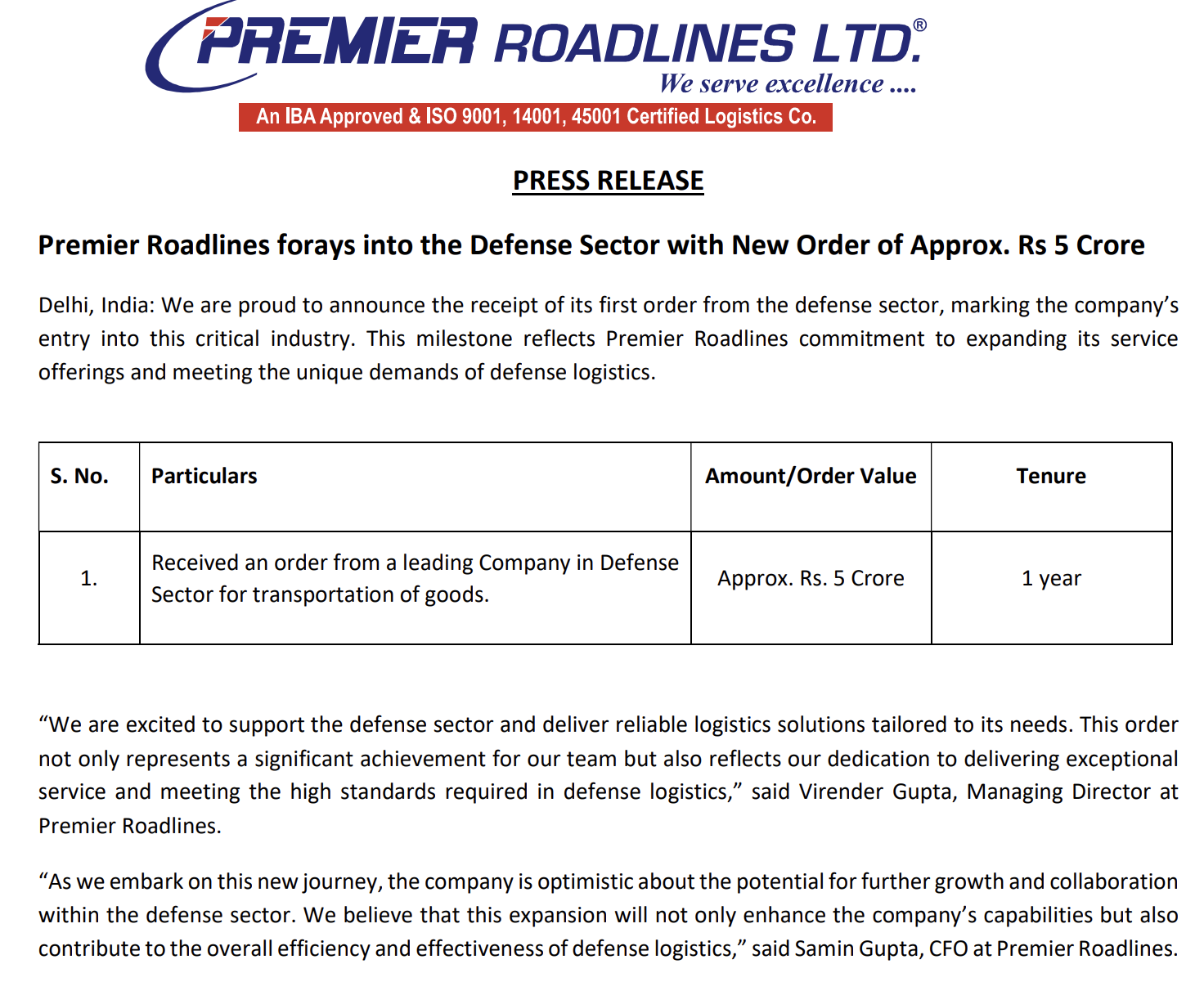

Premier Roadlines Ltd (18-09-2024)

Premier Roadlines forays into the Defense Sector with New Order of Approx. Rs 5 Crore

02/09/2024

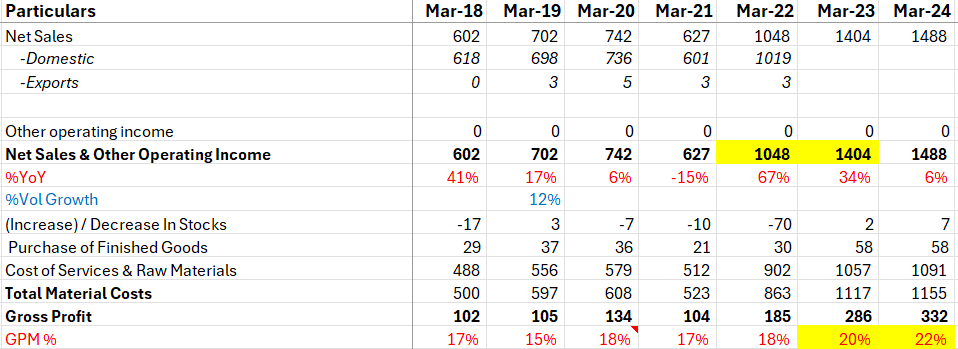

Kingfa Science & Technology (India) Ltd-Could it be a dark horse for Make In India Theme? (18-09-2024)

Was looking at this company, can someone explain how has the Gross margins been stable from FY’20 to FY’22 inspite of high volatility in RM (crude prices) during that time.

Is it because they source major RM from parent co. or they just pass on all the price increase?

And then later what caused the GM to increase in FY’23,24

A super simple way to find good companies (18-09-2024)

Thanks, went through the resources, was really helpful.

Ola Electric – Full Stack EV play? (18-09-2024)

And then only the company reacted…