The X post does not make any sense. The attached auditor comments does not prove the poster’s surprising claim. The claim if true would be concerning but there is no proof.

Disclosure: Invested from lower levels.

The X post does not make any sense. The attached auditor comments does not prove the poster’s surprising claim. The claim if true would be concerning but there is no proof.

Disclosure: Invested from lower levels.

The 3 other comparable listed companies : Updater Services, Quess Corp and SIS Ltd all trade at around 35 P/E (33.1, 35.3, 36.8 respectively)…is there a reason why Krystal trades below at 20.4 P/E?

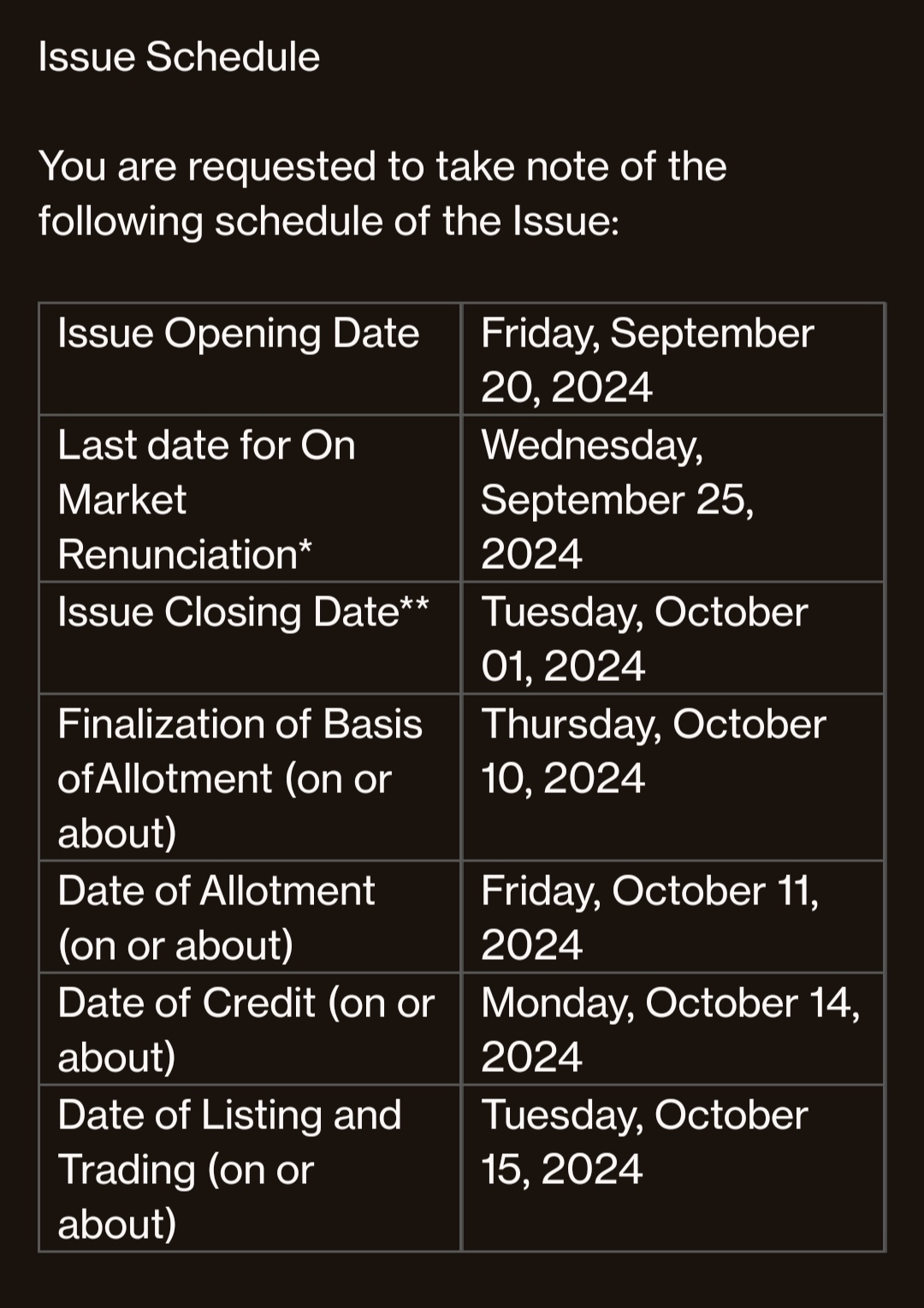

RE Schedule

The company that raised 1200 odd cr and trading at 2400cr Mcap is really not fair. As the interest rate cycle takes a U-turn the company should perform way better. This is classic example of a value investing for me. Best in class company with pristine governance and trading at peanut valuation.

Market has a few reservations from my understanding, namely:

One thing is really no-brainer for me, the TAM of MSME lending is incredibly huge and unlike affordable housing market, the competition is not proportional. Companies like SBFC finance and UGRO that have built the physical and digital infrastructure will take the lead, it’s just the matter of time.

One caveat is; the opportunity cost of remain investing in Ugro has been huge, when the whole market is exploding. IMHO it’s a choice, Ugro has all the ingredients to be a 10 bagger from here with low or no risk, even then the Mcap would be just 30k cr.

PS: Mcap would be around 3400cr if you include all the CCDs and warrants that will get converted into shares in the next 18months.

Disc: invested

@sandeep17 Thank you for your reply.

I was also wondering why mutual funds keep the rebalancing period of 6 months. In this momentum strategy keeping such a long rebalance period is not good as it will start facing momentum decay. To corroborate the evidence, i simply checked the current portfolio of UTI nifty 200 momentum 30 fund and Tata Midcap150 momentum 50 fund.

I checked charts of all these 80 companies, and what I found is, almost 80% companies are either consolidating or they are even in downward slope. Inspite of this, these funds have given more than 60% and 50% returns in last 1 year. So my contention is that, if we apply smaller rebalancing period, we can definitely outsmart these guys.

Also these mutual funds are following that particular indexes, so they have to do 6 monthly rebalancing as the underlying index does that. And being a larger size funds, it is difficult for them to entwr and exit the stocks without impact costs, like we do. May be thats the reason. But certainly its along period for the strategy. Also now Motilal has come out with NFO for Nifty 500 momentum fund, even in that they are having same 6 month rebalancing. And in 6 months, entire momentum world chnages a lot.

Anyone tracking TRIL? It has formed lower low pattern on chart and went below 21 week MA first time since April 23? Signs of weaking in transformer space and this stock?

Yes, different company by the name of Nibe Ordnance & Maritime Ltd, but there are no sellers in the stock.![]()

Nibe is going to manufacture aircraft parts and also helping with the launching of satellites, while being 2 years old and basically making iron frames/parts all this while ![]() let’s see how it makes us some money at all.

let’s see how it makes us some money at all.

Does it have a shipping parts business also?

Disc: invested

Well, being a Momentum proponent myself and having manually backtested a strategy from 2018 (until I went live with it this Jan), I can tell you that there’s nothing right or wrong about either of the two approaches. Over a long period of time, you will see that you will have a decent share of such regret scenarios either ways. One might regret exiting at 15% trailing loss or one might regret not having exited. Doesn’t matter over the long term in my opinion. One should choose as per one’s psychological framework. The trailing loss approach will ofcourse result in higher churn which may not appeal to everyone.

This is also proven by the fact that the momentum indices published by NSE Indices have comfortably outperformed the broad based indexes and a lot of active funds as well ( in the respective category) by a decent margin even with a rebalance period of 6 months.

So the visibility of revenue of 800 crores plus revenue seems to be more realistic now with new order of 42 crores to be executed by May’25.