stock hasn’t corrected despite poor fundamentals. But technicals suggest the stock is about to breakout.

stock hasn’t corrected despite poor fundamentals. But technicals suggest the stock is about to breakout.

FY20-24,

earnings up 20%, stock up 3x … ![]()

Curious if export realisations in general in this space are higher? Indri is being retailed at GBP45 for 700ml bottles, which is far higher compared to Indian retail prices.

Are you still following Precision Wires?

Few points add before jump on Export part:

2.The mills will start at MH and Kar in somewhere ~ Oct end / Nov first half and UP ~ Nov / Dec 2024

3.The mills want to increase MSP 4000 to support farmers (watch this number carefully)

current situation of coffee crop and scope of expansion

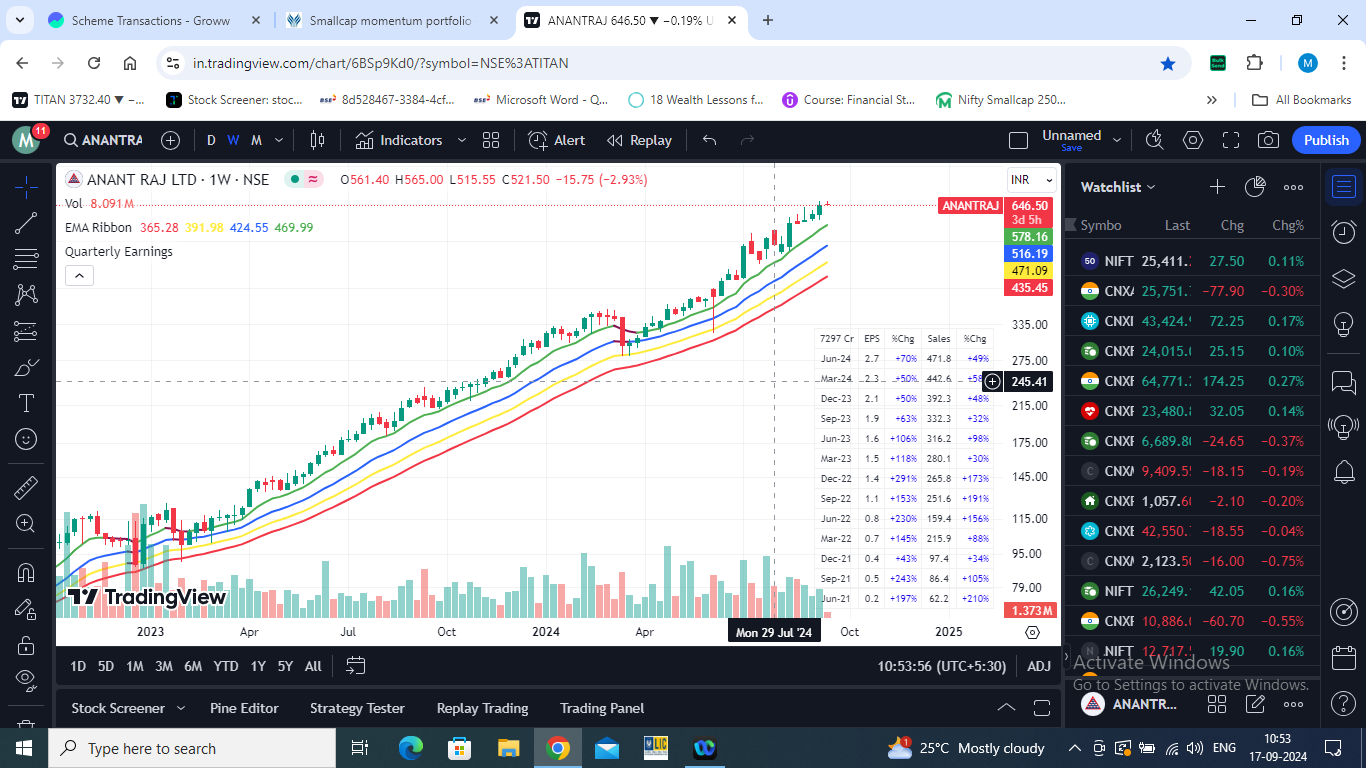

@ChaitanyaC If you give a detailed attention towards this rank-based momentum portfolio, you would realise that since Sharpe returns are used, we are trying to avoid high volatility stocks, which can bounce up on some news and come in the list one week and go out of the list the very next week. Volatility is taken care of. Then there is a very high possibility that stocks like Anantraj might come in the list which are in a very secular uptrend and not volatile.

So what do you thin? When will such stocks go out of the rank? Mostly they will not have abrupt exit. They will slowly lose momentum over 6 months to 1 year and then go out of worst held rank.

Imagine , it came into your ranking list in July 2023 and till today it has given you upmove of 288% and now its downward spiral has started and suppose it goes out of ranking list in lets say march 2025, by giving out all the gains or substantial gains back…That would be very unfortunate, after seeing such high gains. And this will be the story for all the Sharpe-curated secular stocks. They will behave like good boys while going up as well as going down.

So to avoid giving out all the gains and to protect these profits, its more sensible to have a trailing stop-loss. This strategy is not written in Bible Or Gita or Kuran that we cant change it to protect our profits. We need not be at the mercy of stock price behaviour if we could protect the gains by just implementing a risk minimising feature. Also if you see it in that way, Worst held rank , meaning we are selecting top 20 stocks but not selling till it crosses 25th rank, is also a risk minimization feature only to avoid whipsaw…

Obviously when we sell the stocks , then can again re-bound and come into top list, but thats not a cause of concern. What I should be happy with is, I tried to protect my gains and I am able to do it.

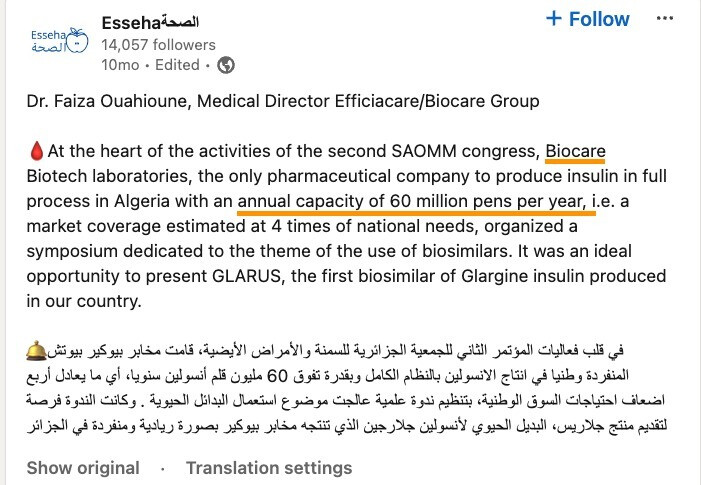

There’s a gradual scale-up to Biocare Biotech seen in exports data last couple of months – almost to the tune of 200k pens. It appears more or less likely that this is the source for the 10million own IP insulin pen order.

BioCare seems to have started production fairly recently and has capacity for 60 million insulin pens

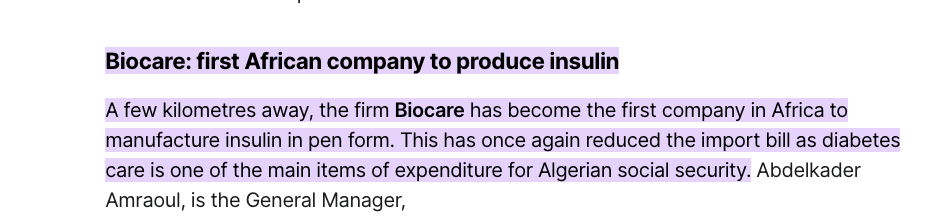

As per this news, Biocare is the first African insulin plant and was setup to reduce import bill.

It looks like Sanofi, Algeria was importing insulin and probably doing fill and finish there and had a capacity of 100 million pens (was also exporting to rest of Africa).

Somne regulation seem to have changed (either duty on imports or withdrawl of subsidies, its unclear) which has made things difficult for Sanofi once the import substituion plant of Biocare started production.

So two things are clear, there could be more to the 10 million pen order, considering the total capacity of 60 million pens at Biocare. The increase in volume from contract-manufacturing to own-IP is structural since regulation across the world have made things difficult for players like Sanofi (Lantus having price restriction in US as well at $35). Shaily volumes and margins have a potential to go up. To put it in perspective, at Rs.60 per pen, the 10 million pen order is worth 60 Cr. The whole of healthcare revenue for Shaily in FY24 was just 108 Cr in FY24 with 80 Cr coming from manufacturing. That puts this 60 Cr in context and any further volume scale as well in better context.

Disc: Invested.

![]()

Makes an interesting read

Frankly , its not a small thing. We may end up giving all the gains that we have got on the position. The core strategy will remain as rank-based momentum, but this tweaking can be seen as a risk management measure to lock-in the gains.