Posts tagged Value Pickr

Supriya Lifescience Ltd – pure play API (15-09-2024)

I have been tracking it since IPO. Invested very low levels. In my view, the 1000 Crore target will be achieved earlier than guided. The China plus advantage may be a positive surprise.

SmallCap Hunter : Trying to find the dark horses with triggers (15-09-2024)

Does anyone has more insight on Shardul Securities. It Q.o.Q numbers are tremendous and reserves has been rising. Book value is still comparable with the current price and P/E is less than 4.

Although the stock has been cycle of upper circuit and lower circuit. Is it operator play? Would really appreciate if anyone can share their expertise. Thanks !

IZMO- bet on new technologies in Auto retail & defence (15-09-2024)

izmo Ltd. Launches izmo Micro: India’s Leading System-in-Package (SiP)

Manufacturing Facility, Now OperaƟonal in Bangalore.

Entering into Semiconductor space

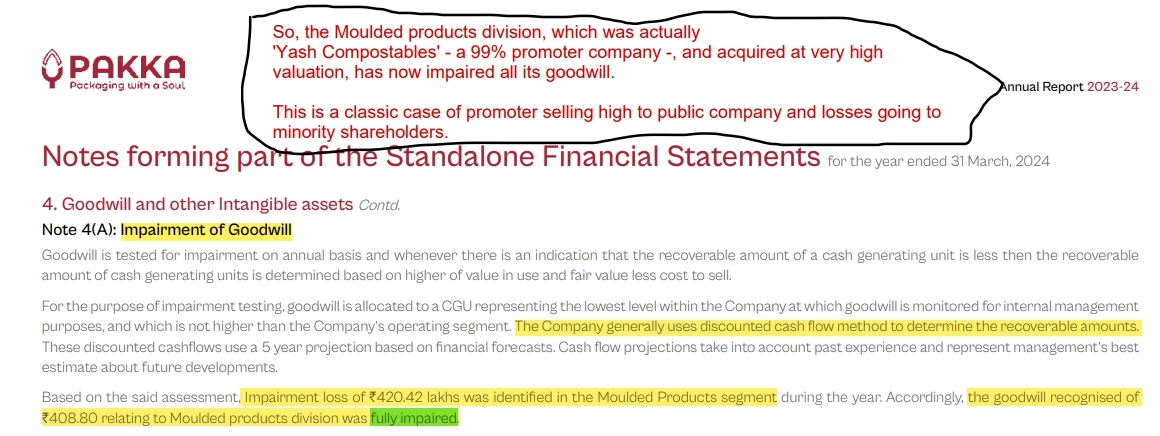

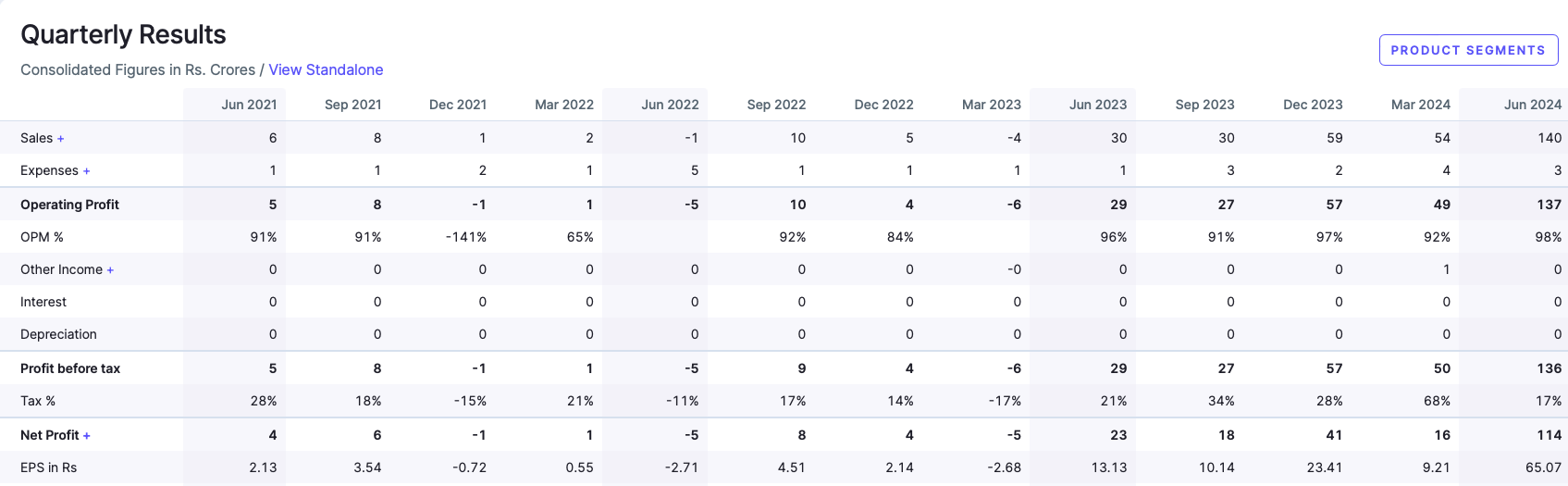

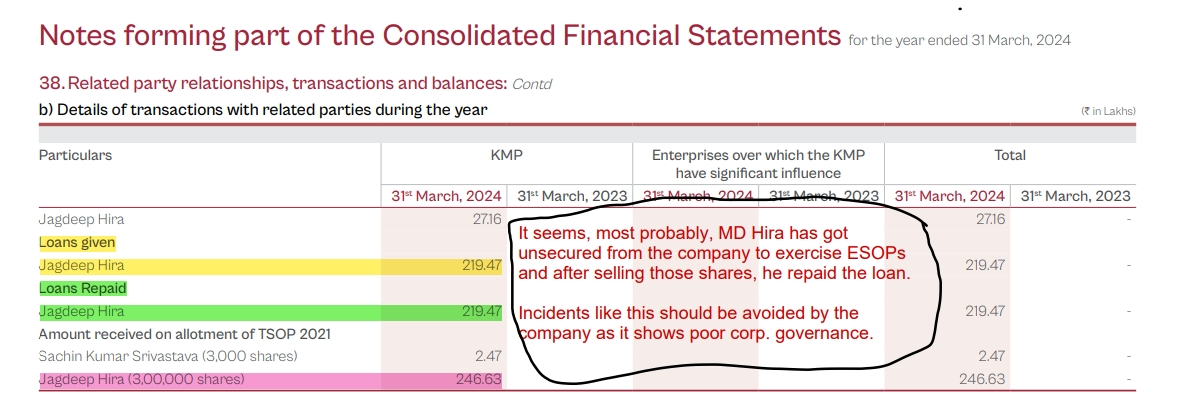

Yash Pakka – (Previously Yash Paper) – Rising from ash (15-09-2024)

After reading the AR 2023-24, i found some aspects worth discussing, which i will be sharing in subsequent posts.

Indiabulls Housing – A compounder from here? (15-09-2024)

Still how they will reach the PAT of INR 4000 by FY’27 is not clear. The Path is a bit unclear.

Even if we take NIMs of 4 percent on book assets of 40k cr – INR 1,600

plus 1 percent on total AUM of 1 lacs cr – INR 1000

plus 0.5 percent processing fee on incremental disbursal – say 150-200 crs. (On disbursement of 30k crs)

Revenue sum barely reaches 3000 crs and on top of that you have Opex and credit costs.

In all scenarios it ends up in range of 1800-2200 crs.

Is there any other fee or income that comes in case of colending?

Do they get some additional revenue share if they are originating, maintaining and collecting from the customers? Logically, they should be getting some additional share for ops purpose.

Also, in my knowledge, when you give FLDG to the colender then you tend to get higher share in the arrangement (at tandem your credit risks shoots up).

Can someone help to solve this piece of puzzle.

@Ballaji_Vijayan @Mihir_iitr @Vineet_Bhatia and others.

Disc: tracking position taken

Policybazaar – Insurance Online (15-09-2024)

@joinjp2003 @amit151190 and others what’s your take on Star Health. They have highest market share in Retail health insurance space and have been churning good PAT with guidance of 3x PAT in next 4 years with doubling of Premium.

How shall we compare the PB fintech with a traditional insurance company like Star Health from the valuation perspective?

Health Insurance sector shall explode in India in coming time (the process has already begun). This is the accumulation stage of the long term story thats still panning out.

Thanks!

Disc: Invested in Star Health and PB fintech

Sandur Manganese (15-09-2024)

Recently, SMIORE has expanded its operations to include ferroalloy production, coke manufacturing, and power generation. They’ve also integrated downstream, aiming to become a more vertically integrated player in the steel and energy sectors. This diversification helps mitigate some of the cyclicality associated with raw material markets like manganese and iron ore.

Let’s break down the significance of each operation:

1. Ferroalloy Production

- What it is: Ferroalloys are alloys of iron with a high proportion of one or more other elements, such as manganese, silicon, or chromium. SMIORE primarily produces silicomanganese and ferromanganese.

- Where it’s used: These ferroalloys are critical in steelmaking. Silicomanganese and ferromanganese are used as deoxidizers and to add specific properties to steel, such as improving its hardness, strength, and resistance to wear and corrosion.

- Benefit to SMIORE: Ferroalloy production adds vertical integration to the company’s mining operations. Instead of only selling raw manganese ore, the company processes the ore into higher-value products. This enhances profit margins, reduces reliance on volatile raw material prices, and positions it closer to end-users in the steel industry.

- Market relevance: With the global push for infrastructure development and manufacturing, demand for steel continues to grow, which directly increases the demand for ferroalloys.

2. Coke Manufacturing

- What it is: Coke is a high-carbon fuel made by heating coal in the absence of air. It’s primarily used in steel production as a reducing agent in blast furnaces, helping to melt and purify iron ore to produce pig iron.

- Where it’s used: Coke is integral to the traditional steelmaking process. It helps achieve the high temperatures needed in blast furnaces to convert iron ore into molten iron, which is then processed into steel.

- Benefit to SMIORE: By producing coke, it reduces the need to buy this essential material from third parties, cutting costs and improving the efficiency of its iron and steel production chain. Additionally, as the global steel industry faces supply chain challenges, having its own coke production gives the company an advantage in maintaining production continuity.

- Environmental aspect: Coke manufacturing is typically a carbon-intensive process. However, investments in clean energy, such as its thermal and future renewable energy plans, suggest a forward-looking approach to reducing the environmental impact of this operation.

3. Power Generation

- What it is: SMIORE captures and utilize the heat produced during their operations to generate electricity. It operates a 32 MW thermal power plant, which primarily supplies electricity to its own mining and manufacturing operations. In addition, the company has ambitions to expand into clean energy.

- Where it’s used: The power generated is largely used for its mining and ferroalloy production operations, ensuring they have a stable, reliable, and cost-effective energy supply.

- Benefit to SMIORE: Power generation offers energy security and cost efficiency. Rather than being exposed to fluctuating energy prices, the company can control its energy input costs. This also reduces the company’s operational risks, as any power outages or supply issues can have severe impacts on continuous operations like smelting and ore processing.

- Future potential: The company’s future move towards cleaner energy production aligns with global trends towards sustainability. By generating clean energy, it not only reduces its carbon footprint but may also tap into government incentives for green energy projects, improving its public and market standing.

The synergy

- By incorporating ferroalloy production, coke manufacturing, and power generation into its operations, SMIORE is creating a closed-loop system where raw materials (manganese and iron ore) are transformed into higher-value products (ferroalloys), fueled by in-house energy (coke and power generation).

- This level of vertical integration offers the company better control over its supply chain, reduced operational costs, and the ability to weather fluctuations in commodity prices more effectively.

Microcap momentum portfolio (15-09-2024)

Hi @araman,

How to refresh the database with the latest data?

IRB INVIT TRUST- new game in the town! (15-09-2024)

@KS16 Thanks for all the informative post you bring for the forum.

What you all think about IRB Invit and Bharat Highway against NAV to traded price. IRB Invit is loaded with BOT asset and Bharat is loaded with all HAM asset. IRB Invit no visibility when next asset will be loaded . Bharat is awaiting for approval from NHAI on take over of GR Aligarh Kanpur Highway . Bharat also has a ROFO agreement with GRIL , nothing as such for IRB Invit though stable asset generally comes to IRB Invit from its sponsor. But IRB also has another private Invit but mostly focused on construction of asset.

As on March-2024 IRB Invit has NAV of INR 98.32 and market price at steep discount of 62.

As on March-2024 Bharat Highway NAV INR 114.12 . Market price tracking NAV almost.

Generally there remains a discount to NAV for traded price. Any thoughts.