kindly post some more updates to select mutual funds?

Posts tagged Value Pickr

Zaggle_A platform to address pain points for enterprises (13-09-2024)

Even most IT companies have a 60-days payable, they raise invoice at end of month & expect to get paid in 60 days. Most IT companies irrespective of profitability have good OCF/profit ratio.

One would expect Zaggle as SaaS to have huge OCF, but their OCF is consistently negative.

Even if H1 of an FY is a slow period, it might approximate to H2 of prev FY but OCF is still negative consistently for H1s too.

Macpower CNC Machines: Manufacturing a Strong Growth? (13-09-2024)

Capex announced for capacity expansion plus backward integration as per plan. For FY 26 the sitting capacity would be 2500 machines which means that capacity would be expanded by almost 1000 machines within this and previous FY. It’s fair to sense that the management is now getting geared up for the next phase of growth.

With defence orders also kicking in and a lot of institutional meetings as well lined up, it’s highly probable that some fund might be waiting on the sidelines to jump in. The stock is low float with high class management.

It wouldn’t be as straightforward to go ahead and do a lot of calculations wrt valuations since a lot of unknowns such as a JV etc might make the proposition even sweeter.

Disc-Is the biggest holding in the portfolio and can be biased

Dreamfolks services limited( DFS) (13-09-2024)

highway business is again not capital intensive so should not be a problem trying it out. but i do not see it scaling up with good profits.

the mainstay airport business has to perform better.

MTAR Technologies – A wager on innovation meeting economies of scale (13-09-2024)

See you’re points are valid. We underestimate how much financial knowledge may be acquired by merely running a business. One has to take effort to know it. Just experience may not teach everything. I suggest we wait and watch for eps.

From my personal experience I’ll say. Unless you’re from one of the traditional trade communities you do not understand working capital and compound interest in India no matter how much you are educated.

Va Tech Wabag (13-09-2024)

Company Profile: The company is a technology focused water solution provider having core expertise in EP, with civil activities being outsourced, following an asset light model. The company offers world-class technology at competitive prices promoting circular economy, resource recovery, and manufactured water. The company has presence across 25 countries.

a) Q1 FY25 results: The following are the highlights of the company’s Q1 FY25 results:

-

The company’s Q1 FY25 revenue from operations stood at Rs 626.5 crores, up 13.3% YoY. EBITDA stood at Rs 81.3 crores, up 23.4% YoY, whereas EBITDA margins stood at 13% versus 11.9% YoY. The company’s PAT stood at Rs 55 crores, up 9.9% YoY. PAT margins stood at 8.8% versus 9% YoY.

-

The company earned 60% of Q1 FY25 revenues from RoW and 40% from India. 81% of the revenues were from EPC and 19% from O&M. 57% of the revenues were from the municipal segment whereas 43% were from the industrial segment.

-

On a consolidated basis, the India business revenues declined 22% YoY, and the export revenues doubled. This was because of the general elections in India and two international projects in the supply phase. On the domestic side, the revenues will start flowing in from Q4 FY25 majorly from the 400 MLD desalinization plant.

-

The higher gross margins in the current quarter can be attributed to a higher international revenue mix.

-

The company completed the 100% divestment in Wabag Romania in Q1 FY25.

B) Order book and order intake: The following are the details about order book and order intake:

-

The company’s order book as of Q1 FY25 stood at Rs 10,676 crores versus Rs 11,400 crores as of Q4 FY24. Of the current order book, 69% is from India and 31% is from RoW. 55% is EPC and 45% is O&M. 91% is municipal and 9% is industrial.

-

The company’s order intake for Q1 FY25 stood at Rs 67.2 crores. Out of this, 68% is India and 32% is RoW. 82% is municipal and 18% is industrial.

-

The company is a preferred bidder in projects of over Rs 6,000 crores in the MEA and India region, which will take anywhere between 1-5 months to flow through.

-

On 6th Sept’24, the company won an EPCC order worth Rs 2,700 crores from the Saudi Water Authority towards a 300 MLD Mega Sea Water desalinization plant. The project is slated to be completed within a 30-month period. With this order, the company’s total order book stands at Rs 13,376 crores.

C) Project highlights: The following are the highlights for the company’s ongoing projects:

-

The company’s 400 MLPD desalinization project in Chennai, funded by JICA, is moving at a brisk pace and engineering activities are at its peak.

-

The company’s 200 MLP sewage treatment plant project in Bangladesh and CIDCO water treatment plant in Maharashtra are progressing well.

-

A large part of revenues from the Senegal and SIBUR projects will be earned by Q2 FY25 as they are EP projects.

D) Future outlook: The following is the future outlook provided by the management:

-

O&M has been the company’s focus as it helps bring in stability, better profit margins and cashflow visibility. The company has a long-term visibility on O&M with a robust order backlog and it will continue to develop its O&M business.

-

The recent budget announcements also put emphasis on promoting water supply, sewage treatment, and solid waste management projects and services for 100 large cities which will augment demand for freshwater and other water infrastructure.

-

The company will have some semi-conductor, CBG, and green hydrogen projects in its pipeline in the next 2-3 years as it has already started working in these segments. It will be setting up 100 CBG projects in partnership with peak ventures over the next few years. Order inflows in the semi-conductor space could start as early as FY26. Hydrogen is still in a development phase.

-

By FY25, the company is targeting an order book of Rs 16,000 crores.

-

The company aims to double its revenues and increase the margins over the next 4-5 years. It has given a medium-term outlook of 13-15% EBITDA margins. Also, H2 is always far better than H1 in terms of execution. FY25 revenue growth guidance is 15-20%.

-

One of the company’s stated goals is to derive 50% of the revenues from international business. The Middle East market gives better flavor with respect to the O&M business. Also, internationally, there is a scope of have more EP projects. The company will strive to keep at least 1/3rd of revenues from EP and will aim to improve this percentage over the long run.

-

The company’s closest international peers are Veolia (French company) and the Beijing Water Company.

-

The company also sees growing opportunities in the One City One Operator Model both India and internationally. It is currently handling water treatment activities for the city of Agra and Ghaziabad.

-

The company has also pre-qualified for a 1000 MLD desalination plant in Egypt. As per ICICI securities, Egypt and Middle East have a strong pipeline of desalination projects.

D) Key monitorables: The following are the key monitorables for the company:

-

As of FY24, receivables formed almost 70% of revenues and 45% of the total assets. Although the company has said that it takes 3-4 months to collect the receivables for the execution done in Q4, hence the receivables will normalize.

-

Since the company has a presence across various geographies, it is prone to geographical risks arising out of war, politics, climate, etc.

The stock trades at a TTM PE of 34x.

Zaggle_A platform to address pain points for enterprises (13-09-2024)

With re: receivables, I have an explanation to this.

Now H2 is where most of the spends (incentives, vendor payment, benefits etc.) happen in companies – per the Q1FY25 transcript, H2 is 60-65% of spends. Hence it would be reasonable to assume Q4 at 35% of spends & hence, February+March is about two-third i.e. 23% of spends.

The company operates on a 30-60 day cycle which means the money (revenue) Zaggle is expected to receive in Feb+Mar – is received in April and May. Since the receivables information you’re seeing is as-on 31st March of any year, it’s likely you’ll see a reporting of 20-25% receivables-to-revenue ratio every year

Dreamfolks services limited( DFS) (13-09-2024)

Indians hate waiting for charging/refuelling while travelling hence I feel hybrid is the way to go for India rather than full EV car. Hence betting on EV charging and hence lounges on the highway seems like a far fetched idea …bit of a desperate move to chase growth…

Only time will tell if it is a diversification or “di-worsification” as mentioned by Peter Lynch…

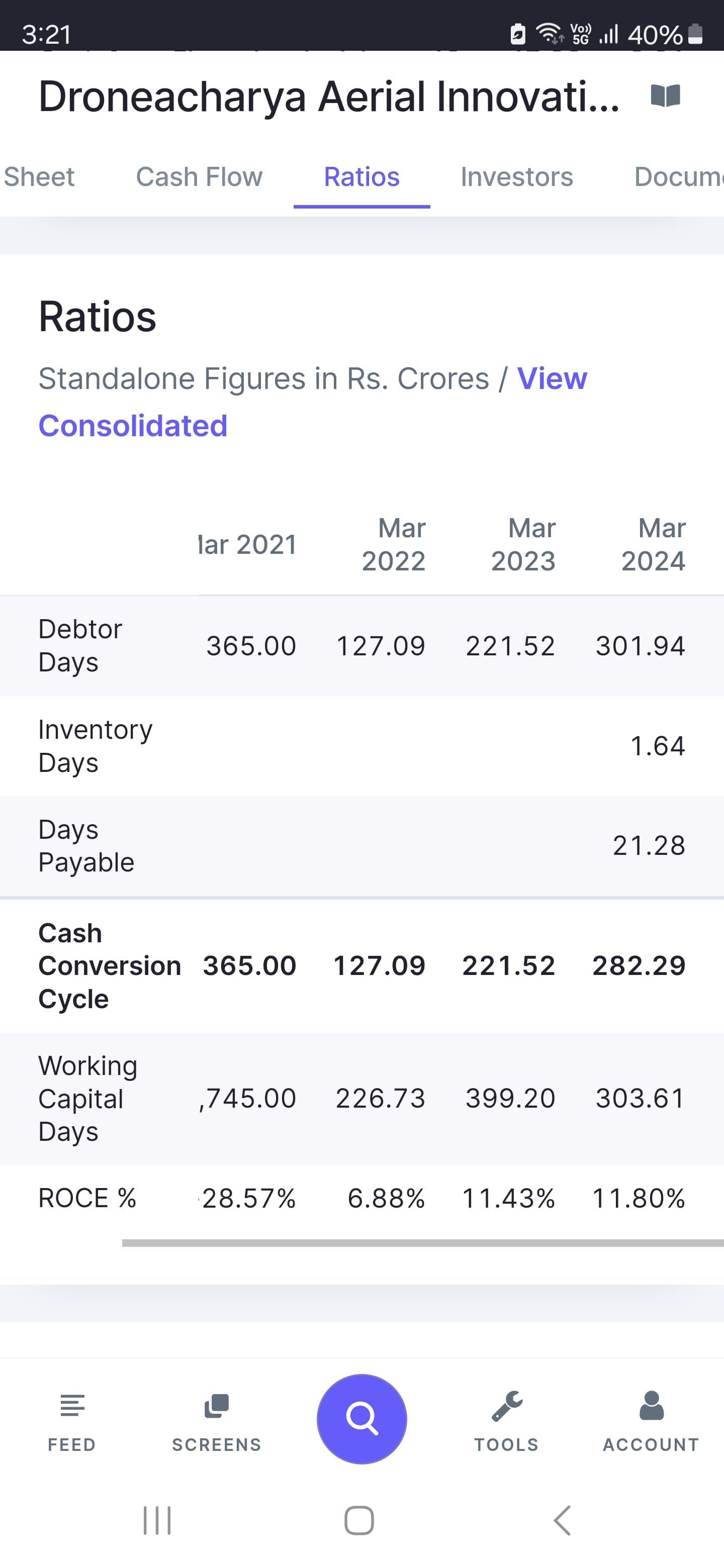

DroneAcharya Aerial Innovations – a new age business (13-09-2024)

Can someone please explain such an unusual figure of 300+ Debtor Days?

How is this normal? To wait for a year to receive payment for the sale one makes today?

Please comment.