Brent crude falls below $70 for the first time in 3 years…Direct beneficiary is PCBL

Disc:Invested

Brent crude falls below $70 for the first time in 3 years…Direct beneficiary is PCBL

Disc:Invested

When will TCNS shareholders get the ABFRL shares, anyone has idea?

The best way to analysis is just get through last Investor Presentation , couple of concalls and last 6 month management interview (Mr.Irfan Razak & teams) you will easily understand the sector and Prestige estate future prospect, Real estate cycle in midway it will easily last another couple of year say 3-4 year , just compare the presales date and future launches ,existing land bank etc. Do your own analysis before investing.

Disc: Invested

Hello Sauhard, I think it bit differently , there are very few companies which can generate ROE equal to or more than 100, in my mind Nestle is one such company. With a growth of 15% Nestle gets a PE of 75, while the switching cost in case of Nestle is easier for customers. So PB Fintech which is supposed to have ROE around 100% and growth say around 30% can have a high multiple. I tried explaining the same in my video , its pinned in my x account you can watch it.

X-@amitsinghpal

Once you do it, you might yourself reduce the no. By over 50-70%.

Post you write your thesis we’d be able to critique you better.

At this price distilleries are not going to improve margins. I am not sure if distilleries would be even interested in purchasing at this price. If the auction cannot go down the reserve price then I believe no takers for the broken rice at this price. My two cents.

As mentioned earlier, assuming, even if FCI rice was a viable option, BCL management had no plans of using FCI rice. The only benefit BCL would have had with the availability of FCI rice is easing of pressure on Maize availability and its price as some players would have moved from maize to FCI rice. BUT even though the Govt has removed the embargo on FCI rice for Ethanol on paper, but practically speaking it is as good as not being available IMHO. Landed cost of FCI rice will be 30+/kg and Ethanol price produced from FCI rice is lower than that produced from maize, so I find it difficult to see who will opt for FCI rice, maybe only those which cannot process Maize at all.

There was no way Govt would have gone back to making FCI rice available for Ethanol at around Rs. 22 when States like Karnataka are procuring rice from FCI at around Rs. 28-30. That would have generated lot of heat for Central Govt.

Regarding Q2 results, I agree it doesn’t look pretty. I don’t know how much lower cost (~Rs 23) inventory they had available to be processed in this quarter. BCL is one of the most efficient players, so its results maybe among the least bad. Every Tom Dick Harry knows about the raw material prices plaguing Ethanol industry, I will be surprised if the ‘Market’ isn’t discounting the Q2 results.

I guess the more important aspect is the next years Ethanol price which will be published soon by Govt. If there is any negative surprise, that will move the stock price more substantially than 1-2 subdued quarters.

Disc: Invested. Frustrated. Possibly Biased.

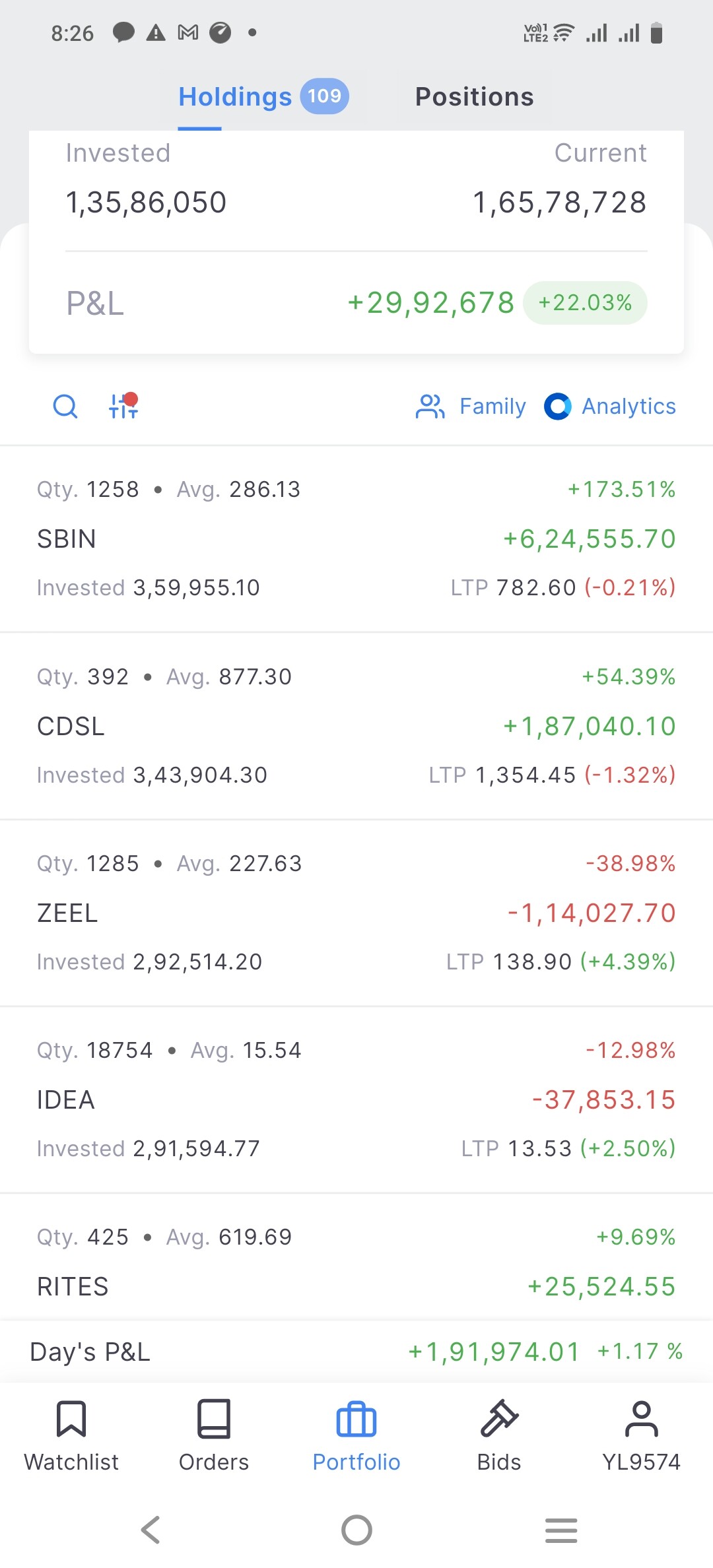

Dear Investor friends, this is my first post on the forum. I would really appreciate a critique of my portfolio. I currently hold 109 stocks in my portfolio and I am looking to reduce it to a maximum of 20. I want to take my investing journey seriously looking forward to your support and hopefully I would like to share my experiences in the future to enrich discussions on the superb platform.

Is this the reason, why IRB invit has been falling?

This news came today…I would like to understand the implications of this to the toll collector like IRB New toll rules: Pay only for distance covered, no charges for first 20 km – India Today

No toll tax for private vehicles up to 20 km, govt amends ‘National Highways Fee Rules’ – India TV

Lol clear cut is debatable. Coz may be we are clearly biased coz of our position or may be we read and interpreted verbatim and you might be biased in some other way coz never thought that the management is telling the truth.

Also, not sure why we are ignoring the numbers – may be that is the fact we need to look at

PS: more than 5000 stocks – not married to anything. Suggest u the same respectfully