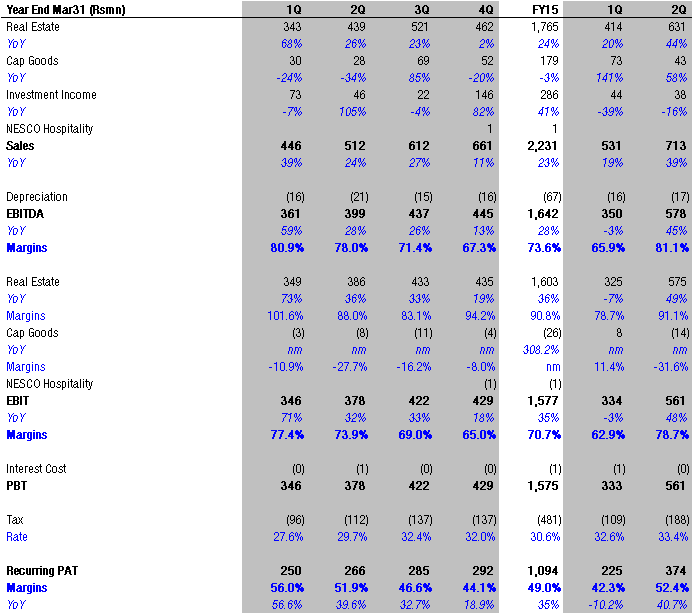

Strong 2Q. Sales +39% YoY, PAT + 41% YoY. This is on account of 100% occupancy level for IT Building 3 & rent free period expiry.

Disclosure: Invested

Skipper is showing improvement and results are quiet impressive from last year onwards...

The self sustainable growth is very visible.

for SSGR see Dr Vijay Malik's explaination: http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

Today facebook showed me this adv. about a dealer selling Royal Enfield close to Taipei (I live in Taipei)

Makes me think, that the brand is travelling to places where company hasn't even started selling officially. This is very promising development. Helps to seed the idea/culture and fan club around it.

It's selling for almost 4x of India price, but Taiwan is known to have atrocious tax rates for bike imports so that could be contributing to it.

Taiwan has a huge leisure bike riders market. Mostly dominated by BMW's, Harley,Triumph's of the world.

This is really setting the stage for something very interesting.

Make me very happy !!

vardha ji

increase in authorized share capital is the first sign of raising funds to fund working capital ? (eg : through debt) or any other plan they have for rise in auth capital.

even eros has ballooning receivables, as we knew recently news on eros.

Rohit, Hitesh,

One of the reason for higher valuation to DB Corp is their ability to enter any given market and start as No.1 or 2 newspaper from day 1 of circulation, which no newspapers in the world are able to achieve. This reduces their gestation period.

Director Ravi kumar is taking pay of only 30Lakh Rs which is very modest for 20Year experience and he owns 8 lakh shares.

Ashok Atuluri took 1.4Cr salary in 2012 when they were in profits. 2013, 2014 he took only 30Lakh

Management looks to be honest and incentives are tightly coupled with performance.

Aviation sector in for good times thanks to low fuel prices,huge opp size n new NCAP ie new civil aviation policy.

Starting a new thread on a defence based micro cap Zen technologies

They basically prepare simulators in the defence sector primarily landbased as of now. Here are a set of links all should go

through:

http://www.defproac.com/?p=820

Here are some viewpoints to kickstart the discussion.

"In a parallel development, it made an allotment of 1.38 million equity shares on preferential basis to Parikh, who had founded Kanpur-based Resinova Chemie in 1995, at a share price of Rs 425.93 apiece, aggregating Rs 59 crore (approximately $9 million)"

Read more at:

http://www.vccircle.com/news/technology/2015/11/03/astral-poly-completes-acquisition-resinova-chemie

I think no one's looking at the ballooning receivables - the company now has Rs. 35 Cr. of receivables outstanding - up from Rs. 25 Cr. last yoy.No wonder the company authorized an increase in authorized share capital

Look at operating cash flows - all of the profits go back into inventory of FG that they maintain at customer's end. I am not sure if this is healthy in the long run. This is reflecting in the increasing WC debt too whch is up 25 % or so.